In a pivotal discussion during the Securities and Exchange Commission’s recent roundtable on crypto custody, regulators and industry leaders tackled a question with sweeping implications for investor protection: Should the Securities Investor Protection Corporation (SIPC) cover crypto assets in broker-dealer insolvencies?

The conversation, held as part of the SEC’s “Spring Sprint” initiative toward regulatory clarity in digital assets, highlighted mounting concerns over the lack of federal safeguards in the event of crypto-related brokerage failures. Insurance in the crypto custody space is notoriously hard to come by, and when it is available, policies are usually vague about what risks are covered and to what extent.

A Core Issue: Are Crypto Customers Protected?

Currently, SIPC protection—which acts as a backstop for customers if a traditional brokerage fails—does not extend to crypto assets that are not classified as securities. This legal boundary has become a flashpoint for policymakers as digital assets increasingly move into quasi-traditional financial services.

What Is The SIPC?

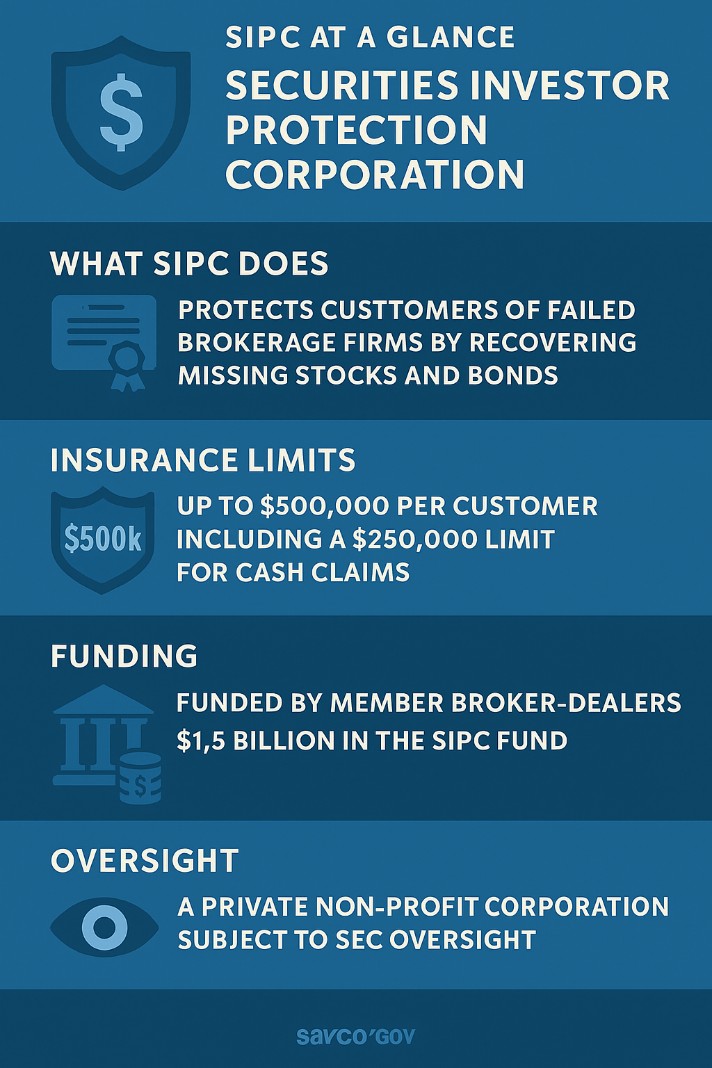

The Securities Investor Protection Corporation (SIPC) is a non-profit membership organization established by Congress in 1970 to protect customers of failed brokerage firms. SIPC’s primary role is to restore missing stocks and cash to investors when a SIPC-member brokerage firm goes bankrupt or experiences financial difficulty. Unlike the FDIC, which protects bank deposits, SIPC does not insure against market losses or guarantee the value of any investment; instead, it covers up to $500,000 per customer, including a maximum of $250,000 for cash claims.

SIPC is not a government agency—it is funded through assessments on its member broker-dealers, not taxpayer money. Nearly all U.S. broker-dealers registered with the SEC are required to be SIPC members, ensuring that the costs of investor protection are borne by the financial industry itself rather than the public.

Commissioner Caroline Crenshaw asked if Congress should amend SIPA to address the treatment of crypto assets that are not securities as defined in SIPA.

She further pressed the panel to consider how customers would be protected if a broker-dealer holding crypto assets were to fail, absent existing SIPC remedies.

Calls for Legislative Action

Etana Custody CEO Brandon Russell was among the panelists advocating for action beyond SEC purview: “If you want orderly markets and the confidence of regulated money to come into the space in a meaningful way, you need to expand SIPC’s mandate on that. I know this takes an act of Congress, but that’s probably the conversation that needs to take place.”

Others echoed this concern, pointing to the cooling effect regulatory uncertainty continues to have on institutional participation in the crypto markets.

Mark Greenberg of Kraken urged caution, suggesting that SIPC protection must be thoughtfully extended without overwhelming innovation. However, he supported consistent investor protections across asset classes: “We don’t want to make every single trade an on-chain transaction… but we also can’t have different standards for different types of assets that confuse or endanger investors.”

A Regulatory Gap Widens

The debate spotlighted a growing regulatory gap between crypto assets that fall within the SEC’s definition of a security—and those that don’t.

Rachel Anderika of Anchorage Digital, a federally chartered crypto bank, emphasized that digital asset custody inherently involves security-like functions. Still, she acknowledged that crypto’s unique risks—like smart contract failures or custody via omnibus wallets—require tailored protections beyond the traditional SIPC framework.

“In traditional securities custody, we have CIPC and clear rules. For crypto, we’re still figuring out the equivalent safeguards. And investors are noticing that gap,” she said.

SIPC, But for Crypto?

Some panelists floated the idea of a new crypto-specific resolution mechanism. One suggested modifying SIPC’s structure or enabling a “parallel entity” focused solely on digital assets, though this received mixed reactions.

Jason Alante of Fireblocks stressed that while innovative solutions are necessary, regulation must preserve trust in capital markets: “We have the most robust capital markets in the world not because they’re easy but because they’re difficult to access. We need to bring that same rigor to crypto asset custody.”

What’s Next? Congress May Hold the Key

While the SEC has initiated discussions and offered interim guidance through special-purpose broker-dealer (SPBD) frameworks, several speakers concluded that legislative clarity from Congress may ultimately be required.

Commissioner Hester Peirce framed the stakes plainly: “We must ensure that custody requirements further, rather than impair, investor protection and choice… Otherwise, we risk pushing customers into less safe platforms.”