Direct Express Card Switching to Fifth Third Bank: A Complete Guide for Social Security Beneficiaries

Millions of Social Security and Supplemental Security Income recipients who rely on the Direct Express prepaid debit card are about to see a change behind the scenes as the Treasury Department is moving the program’s banking partner from Comerica Bank to Fifth Third Bank.

In addition, the rollout is happening at the same time the Social Security Administration is closing out its broader shift away from paper checks entirely. For beneficiaries who depend on this card every month, understanding what is changing, what is staying the same, and how to protect themselves during the switch is essential.

What Is Actually Changing

The Direct Express program itself is not going away, and the benefits paid through it are not changing in amount, schedule, or eligibility. What is changing is the financial institution that issues and manages the card behind the scenes. Comerica Bank has served as the Treasury’s financial agent for Direct Express since the program launched in 2008. Under a new five-year agreement, Fifth Third Bank has taken over that role, with Money Network Financial continuing as program manager and Mastercard remaining the payment network.

New enrollees who sign up for Direct Express are already receiving Fifth Third Bank cards as of May 2026. The larger and more complex part of the transition involves the roughly 3.6 million existing cardholders who currently carry Comerica-issued cards. Those cardholders will be migrated in phases beginning later this year and continuing into early next year, according to the Social Security Administration’s May 18, 2026 notice to advocates.

Why the Switch Is Happening Now

Two separate but overlapping federal initiatives are converging on Direct Express cardholders this year. The first is the bank transition itself, which followed a competitive selection process by the Treasury’s Bureau of the Fiscal Service. Fifth Third has said the new arrangement will allow it to introduce features such as virtual cards, cardless ATM access, bill payment services, and expanded digital wallet integration for federal benefit recipients, most of whom do not have a traditional bank account.

The second initiative is the government-wide elimination of paper checks under Executive Order 14247, titled “Modernizing Payments To and From America’s Bank Account.” That order, signed in March 2025, required nearly all federal benefit payments to be made electronically as of September 30, 2025. The Social Security Administration has said it intends to complete that transition for every remaining beneficiary by the end of 2026. As of mid-2026, fewer than one percent of beneficiaries, somewhere between 280,000 and 400,000 people, were still receiving paper checks. The Direct Express card is one of the two electronic options the agency offers to that remaining group, alongside traditional direct deposit.

Timeline of the Direct Express Transition

- New Direct Express enrollments have been issued Fifth Third Bank cards since May 2026.

- Existing Comerica cardholders will begin receiving replacement Fifth Third cards starting in the summer of 2026, with the process expected to continue into early 2027.

- Each cardholder will receive advance written notice before their account moves to the new bank.

- Current Comerica-issued cards remain fully functional and continue to receive deposits on the regular payment schedule until a replacement card arrives.

- Once the new card arrives, the cardholder must activate it before using it, following the instructions included with the card.

What Beneficiaries Should Do Before the New Card Arrives

Confirm Your Mailing Address Is Current

Because the new card will arrive by mail, an outdated address is the single biggest risk to a smooth transition. Beneficiaries who have moved recently should update their contact information with the Social Security Administration as soon as possible. An undeliverable card can delay access to benefits and may require additional steps to resolve.

Keep Using the Current Card

There is no need to take any action with the existing Comerica card before the replacement arrives. It will continue to work normally, including for purchases, ATM withdrawals, and cash back at retailers, until the new Fifth Third card is activated.

Watch for the Official Notice

The Social Security Administration and Direct Express have both said they will send advance notice before a new card ships. Beneficiaries should expect this communication through the mail, since unsolicited calls, texts, or emails asking for personal information should be treated with suspicion, regardless of how official they appear.

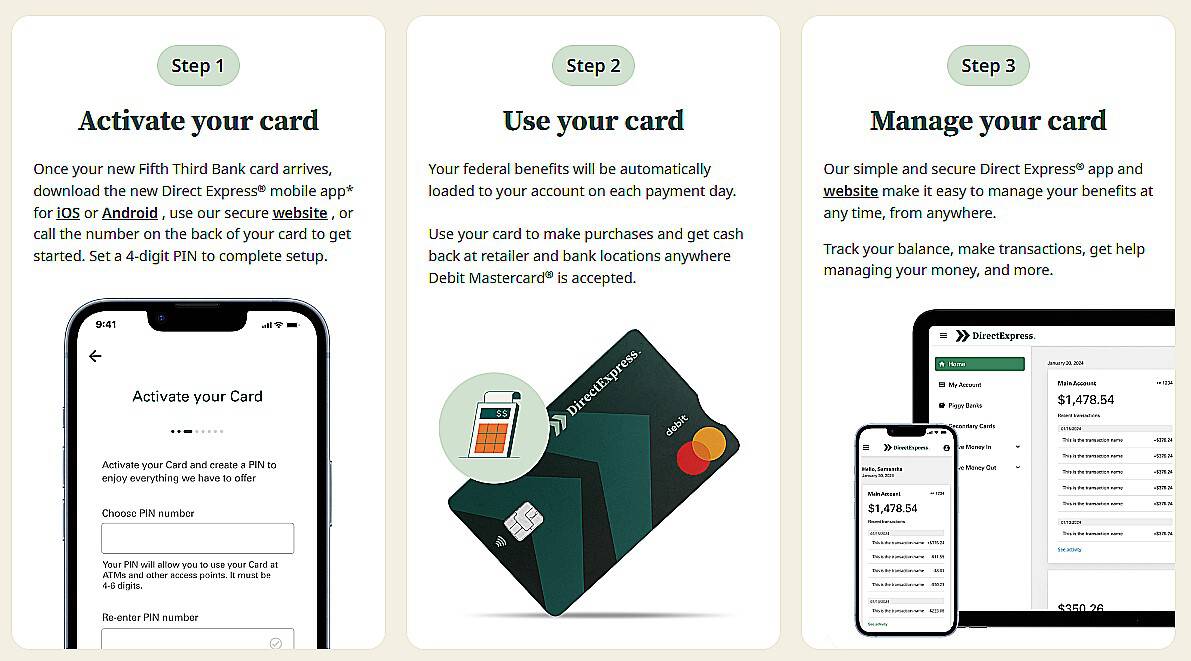

Steps to card activation. Source Direct Express.com

How the Fifth Third Card Will Work

Functionally, the new card is designed to mirror the experience cardholders already have. Benefits will still be deposited automatically on the regular payment date, and the card will still work anywhere Debit Mastercard is accepted, including for purchases, bill payments, and cash back at checkout. Once the new card arrives, cardholders will set it up by downloading the updated Direct Express mobile app, visiting the secure website, or calling the number printed on the back of the card, then creating a new four-digit PIN to complete activation.

Fifth Third has indicated it plans to expand on the current feature set over time, including cardless ATM access and improved digital tools, though the core mechanics of receiving and spending federal benefits are not expected to change for most users.

Fees Cardholders Should Understand

Direct Express has consistently been one of the lower-fee prepaid card options available to federal benefit recipients, and that fee structure is expected to carry over under Fifth Third. Most everyday activity remains free of charge.

- No fee to sign up, no monthly maintenance fee, and no overdraft fee, since the card cannot be overdrawn.

- No fee for purchases anywhere Debit Mastercard is accepted, and no fee for cash back at the register.

- One free ATM cash withdrawal in the United States for each federal benefit deposit, valid through the end of the following month.

- Free cash withdrawals at any bank or credit union teller window displaying the Mastercard acceptance mark.

- A small fee, typically under one dollar, applies to additional ATM withdrawals beyond the one free withdrawal per deposit.

- One free replacement card per year, with a roughly four dollar fee for additional replacements in the same year.

- An optional fee, under one dollar, for a mailed paper statement each month, which can be avoided by using the app or website.

Cardholders who want to minimize costs should rely on purchases and cash back at checkout for everyday spending, save the one free ATM withdrawal for when a larger amount of cash is needed, and use bank teller windows for any additional withdrawals rather than out-of-network ATMs, which may carry a surcharge from the ATM owner on top of any Direct Express fee.

How This Fits Into the End of Paper Checks

The Direct Express bank switch is a smaller piece of a much larger change already underway. President Trump’s Executive Order 14247 set September 30, 2025 as the date by which nearly all federal payments, including Social Security, Supplemental Security Income, tax refunds, and veterans benefits, had to move to electronic delivery. The Treasury has cited cost and security as the primary motivations. According to federal estimates, printing and mailing a paper check costs roughly $3.07, about twenty times more than an electronic payment, and paper checks are sixteen times more likely than electronic payments to be lost, stolen, altered, or returned undeliverable.

The Social Security Administration has said it intends to complete this transition for all remaining beneficiaries by the end of 2026. Beneficiaries who are still receiving paper checks have two electronic options going forward: traditional direct deposit to a bank or credit union account, or a Direct Express prepaid card for those without a conventional bank account. Limited waivers remain available through the Treasury for individuals who can document a genuine obstacle to making the switch, such as a documented disability-related barrier or residence in a remote area without reasonable access to a financial institution.

What to Do If You Have Questions or Run Into a Problem

Most cardholders will not need to take any action beyond keeping their contact information current and watching for the official notice. For anyone who does run into trouble, such as a card that never arrives, a delayed payment, or a suspicious contact, there are clear channels to use.

- Call the customer service number printed on the back of your current Direct Express card for account-specific issues, lost or stolen cards, or disputed transactions.

- Contact the Social Security Administration directly for questions about benefit payments themselves, since the agency continues to handle payment amounts and eligibility independent of which bank manages the card.

- Visit usdirectexpress.com for activation instructions, the ATM locator, and general program information once a new Fifth Third card has arrived.

- Request a waiver through the Treasury at 1-877-874-6347 if a genuine barrier prevents a switch to electronic payment of any kind.

The Bottom Line

For the vast majority of the 3.6 million affected cardholders, this transition should be uneventful. The benefit amount, payment date, and basic way the card works are not changing. The main responsibilities for cardholders are to keep their address current with the Social Security Administration, watch for the official mailed notice, and activate the new card promptly once it arrives