Unlocking the Power of Crypto Loans: A Borrower’s Guide

In the ever-evolving landscape of finance, the crypto sector is boldly challenging traditional banking norms by entering the lending arena. Curious about the world of crypto loans?

Here we demystify the concept, explore the benefits, and examine how you can tap the full potential of a crypto loan.

Crypto Loans: A Path to Financial Flexibility

Imagine a world where you can embrace the potential windfall of your crypto assets without parting ways with them. The allure of exponential value growth in cryptocurrencies like Bitcoin is undeniable. Consider this: between March 2020 and March 2021, Bitcoin’s price skyrocketed by a staggering 900%, soaring from around $6,000 to over $60,000. This meteoric rise underscores the potential loss for those who liquidated their Bitcoin holdings prematurely.

The story extends beyond Bitcoin, with various cryptocurrencies witnessing substantial value appreciation during the 2021 crypto bull run. Although the market saw a retracement in May 2021, many alternative coins maintained significant gains compared to their January 2021 levels. More recently, Bitcoin’s price dipped to around $16,000, but for astute investors, this presented a tantalizing opportunity to seize assets in anticipation of another surge to new highs.

Empowering Holders with Crypto Loans

Picture this scenario: the value of your crypto assets is on the rise, yet you’re short on immediate cash. Selling your crypto isn’t appealing, given its potential future worth. Enter crypto loans – the bridge between holding onto your digital goldmine and leveraging its value for other investments.

Companies entering the crypto loans space are proliferating, offering varying interest rates. Stay informed with the latest crypto loan interest rates here.

Unveiling the Essence of Crypto Loans

So, what exactly are crypto loans? It’s a straightforward concept. You deposit your cryptocurrency, cash, or even NFTs with a lender such as Nexo or YouHodler. In return, these lenders provide you with cash or a different cryptocurrency that you can allocate elsewhere in the investment universe.

If you’re a Bitcoin holder looking to expand your portfolio while keeping your BTC intact, this avenue is a win-win. Notably, Nexo blazed a trail by adding NFTs to their list of acceptable collateral for loans, catering to the burgeoning NFT ecosystem.

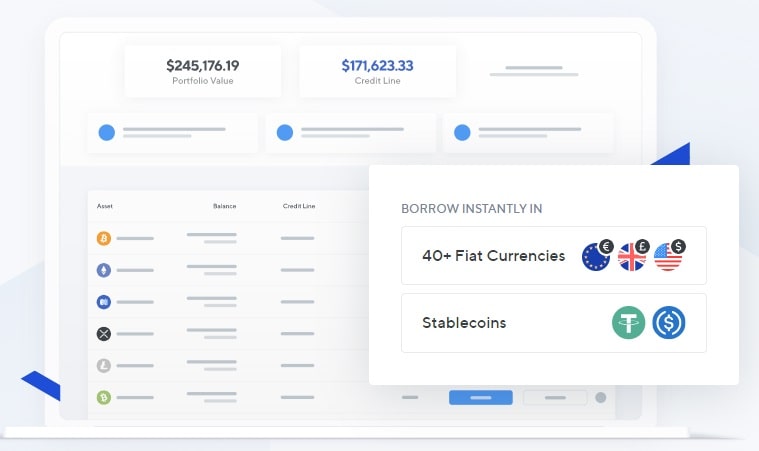

Deposit crypto and borrow national currencies or stablecoins. Source: NEXO

If all goes well, as you repay the loan along with interest, your collateralized crypto or assets are promptly returned to you. This process empowers holders to seize fresh opportunities without liquidating their crypto nest egg.

Enhancing Financial Strategy: When to Consider a Crypto Loan

For long-term crypto holders who aren’t active traders, the wait for value appreciation can feel interminable. While the potential gains are substantial, the unpredictable nature of market surges is a constant companion.

The 2021 Bitcoin price surge is the most recent bull run, but it is also reminiscent of the Q4 2017 crypto bull run. Here, Bitcoin’s value surged from around $4,500 in September 2017 to nearly $19,500 by Christmas. However, the subsequent decline and years of sideways movement highlighted the scarcity of such opportunities.

Crypto loans effectively address these issues by:

- Unlocking Capital: By tapping into your crypto’s latent potential, you free up resources for potentially more lucrative investments.

- Eliminating Market Timing Pressure: Crypto loans eliminate the need to perfectly time the market to capture surges. Your assets remain poised for future gains while you explore other investment avenues.

Crypto Loans: A Gateway Without Credit Checks

An enticing facet of crypto loans is the freedom from credit checks. Even if your credit rating is less than stellar, crypto lenders typically bypass this conventional step. This presents a lifeline for those grappling with high credit card utilization and the urge to consolidate debt under a single loan.

Crypto loans typically don’t require a credit check

It’s worth noting that some lenders may not even require KYC or AML checks. While this leniency is a boon, evolving regulatory landscapes might impact the longevity of this approach, particularly due to money laundering concerns.

The Mechanics of Crypto Loans: How They Operate

While specifics vary across platforms, the core mechanics and associated risks are consistent. Understanding the borrowing process and potential pitfalls is crucial.

Borrowing Limits and Over-Collateralization

An essential element of crypto borrowing lies in comprehending borrowing limits. Simply put, the collateralized cryptocurrency’s value must substantially surpass the borrowed amount. This results in over-collateralization, a cornerstone of crypto loans.

For instance, if you choose Bitcoin as collateral, you might need to deposit twice the borrowed sum. Commonly expressed as the Loan to Value (LTV) ratio, most crypto lenders give loans with an LTV requirement of 50%. This means that to secure a $10,000 loan, you’d deposit $20,000 worth of Bitcoin.

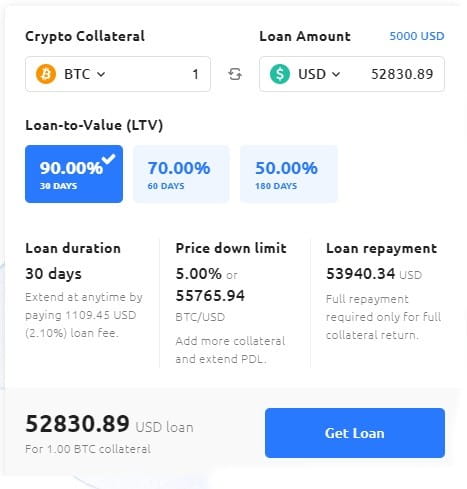

Lenders differ in their policies, and due to the inherent volatility of cryptocurrencies, most institutions mandate borrowing amounts lower than the collateral. Some, like YouHodler, extend an LTV of 90%, while most cap it at 70-75%. Naturally, higher LTV offerings come with heightened risk and accompanying elevated interest rates.

A higher LTV ratio will mean higher interest rates. Source: YouHodler

Crypto Loan Risk Factors

As with any financial endeavor, crypto loans carry inherent risks. It’s crucial to understand these before delving into the world of borrowing against your crypto holdings.

Platform Vulnerability

The foremost risk is tied to the lending platform’s stability. Recent times have seen once reputable platforms such as Celsius and BlockFi face bankruptcy, leading to long-term collateral freezes for borrowers. For example, if you borrowed $10,000 from Celsius using $20,000 of Bitcoin collateral, your Bitcoin assets are now inaccessible until the company’s current bankruptcy proceedings conclude – a process that could span years with no guaranteed return.

Loan Liquidation: Navigating Volatility

Given the volatile nature of Bitcoin and other cryptocurrencies, lenders ensure conservative borrowing by permitting only a fraction of your collateral’s value. A significant drop in Bitcoin’s value might trigger partial loan repayment or a requirement for additional collateral infusion to maintain the loan-to-value ratio. Instances of this nature occurred during Bitcoin’s sharp declines in early 2020 and May 2021, resulting in loan liquidations.

Security Breaches and Hacking

Both decentralized and centralized lending platforms remain susceptible to hacking and manipulation. Unlike traditional banks, crypto wallets lack the safety net of Federal Deposit Insurance. Instances of crypto theft and business collapses due to security breaches are not uncommon.

Prioritizing platforms with robust custodial systems, like Nexo with BitGo, or YouHodler with Ledger Enterprise, offers a layer of protection. Also enquire about insurance policies that safeguard against hacking incidents.

Governmental Intrusion and Regulation

Government sentiments towards cryptocurrencies vary globally. Regulatory shifts can impact crypto access. Instances like China’s ban on crypto mining or India’s potential cryptocurrency possession prohibition underscore the importance of choosing platforms operating within stable regulatory jurisdictions.

Conclusion: Crypto Loans on the Horizon

As the crypto lending sector matures, 2022’s turbulence is yielding to renewed capital inflows in 2023. The breadth of products and services available in this realm is set to rival traditional banks and credit providers, and even some crypto exchanges are now offering lending.

For now, crypto loans provide a pathway for crypto holders to harness the latent potential of their assets. This financial avenue empowers holders to preserve their crypto holdings while capitalizing on diversified investment opportunities – ensuring they’re poised to ride the wave when and if their tokens ascend to a greater height.