The $545K Retirement Reality Check Keeping 40-Somethings Awake

For U.S. workers in their 40s, retirement planning looks stronger on paper than it feels in reality. Empower reports an average savings of $545,424 for this age group, but the Federal Reserve shows the median is just $213,645, meaning half have less. Financial stress is widespread due to mortgages, student debt, childcare, and supporting aging parents, leaving many households stretched despite “above-average” balances. With healthcare and inflation risks rising, midlife savers must look beyond averages and plan for their actual needs.

- Averages vs. reality: The $545k average is skewed by high savers; the median $213k is a more accurate benchmark.

- Guidelines: Fidelity suggests 2-3× annual salary by age 40; many households barely meet this.

- Stress factors: Debt, housing, childcare, and aging parent costs weigh heavily on 40-somethings.

- Risks ahead: 80% of older households face financial strain in retirement.

- Action steps: Boost contributions, tackle debt early, and budget realistically for healthcare and inflation.

For many Americans in their 40s, retirement planning is a paradox: the numbers on paper can look strong, yet the lived reality often tells a very different story. According to fresh data from Empower, the average retirement savings for people in this age group is $545,424. On the surface, that figure suggests security and progress toward financial independence. However, averages can be deceiving, and when paired with broader financial stress indicators, the picture becomes much more complicated.

Source: Empower

The Average vs. the Median

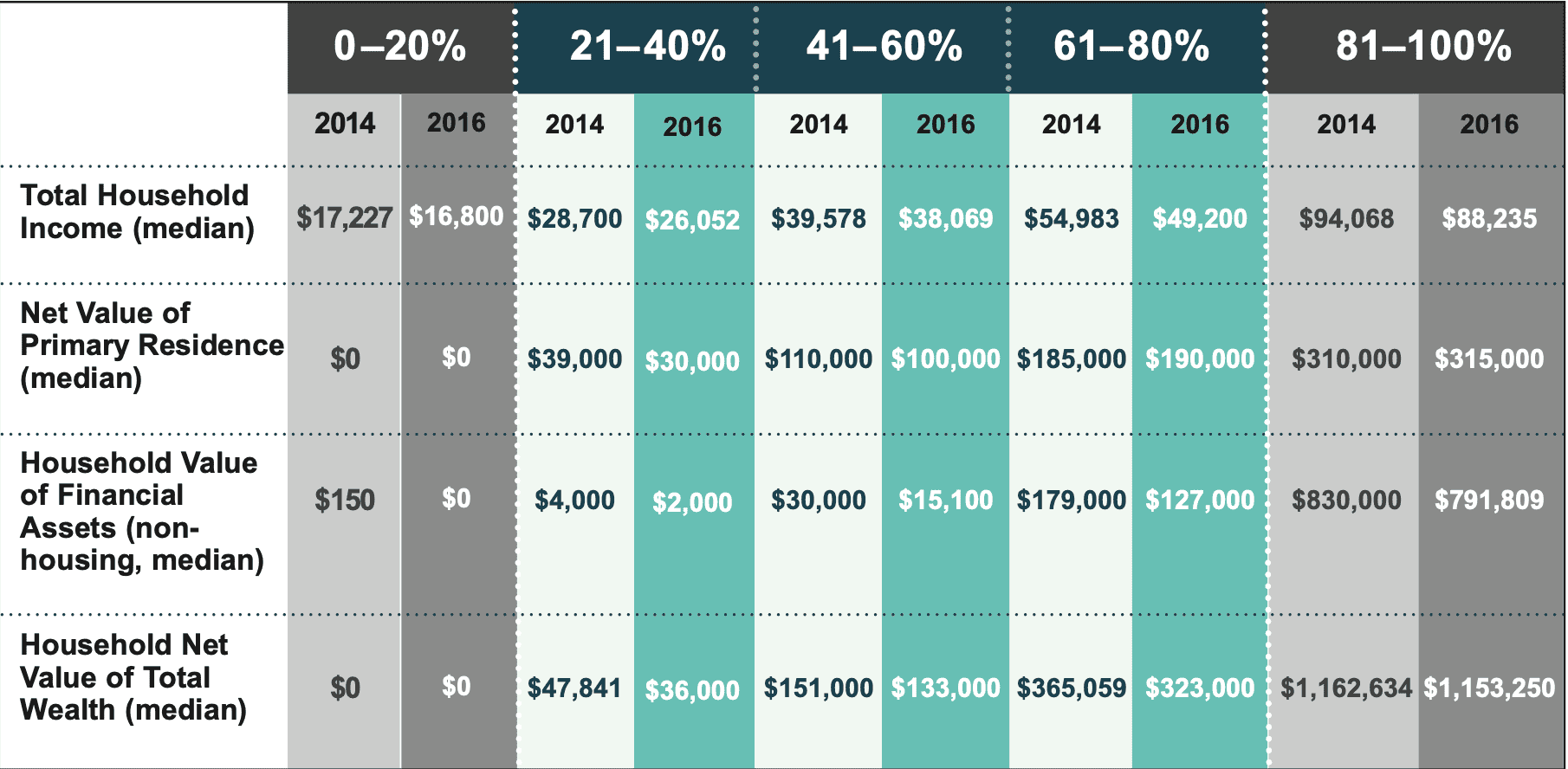

One of the first issues with the $545,000 figure is that it represents an average, not a median. Averages are easily skewed by a small number of households with extremely high savings, those with balances well over $1 million. The Federal Reserve’s distribution data makes it clear that the reality for most Americans in their 40s looks very different. The median retirement savings balance is just $213,645, less than half the average. This means that while a handful of savers are doing very well, the majority fall far short of what traditional financial guidelines recommend.

Guidelines from investment firms such as Fidelity suggest that by age 40, individuals should have saved about two to three times their annual salary. For a household earning $80,000 a year, that benchmark would mean $160,000-$240,000 in retirement accounts. While the median balance of $213,645 appears to fit within that range, it does not leave much margin for unexpected setbacks such as job loss, medical expenses, or periods of economic downturn.

Why Stress Runs High

Even with savings figures that appear substantial, nearly half of people in their 40s report experiencing major financial stress, according to the Federal Reserve. Meanwhile, Gallup polling finds that two-thirds of Americans worry about not having enough for retirement. This decade is often referred to as the “sandwich generation” stage, where individuals must balance competing financial priorities.

Mortgages, student loan repayments, and childcare or college costs for children all place pressure on household budgets. At the same time, many in this age group are beginning to assist aging parents, shouldering medical bills or long-term care costs. These overlapping responsibilities explain why financial anxiety is not limited to those with low balances. Even households with above-average savings often feel stretched thin, particularly in an era of high housing prices, persistent inflation, and uncertainty about the future of Social Security.

The Bigger Retirement Picture

The strain felt in midlife does not always ease with age. Research from the National Council on Aging shows that 80% of older adult households face financial strain or risk of economic insecurity in retirement. Rising healthcare costs, longer life expectancies, and the decline of traditional pensions contribute to this widespread vulnerability. Even well-prepared savers may discover that medical bills, unexpected home repairs, or prolonged market downturns can erode their financial security faster than anticipated.

Source: NCOG

This long-term picture underscores why Americans in their 40s feel uneasy even when retirement accounts look solid on paper. The headline number may suggest progress, but without careful planning, the risk of falling short remains high.

What 40-Somethings Can Do

While the challenges are real, financial experts recommend several strategies to strengthen retirement readiness:

-

Increase contributions gradually. Raising retirement contributions by even 1–2 percentage points can compound into significant growth over the next two decades. For example, on a $100,000 income, moving from a 10% contribution to 12% could mean an additional $200,000–$300,000 by retirement, depending on market performance.

-

Track personal benchmarks, not averages. Comparing yourself to the average saver can be misleading. Instead, track progress against your income and lifestyle expectations, using personalized goals rather than broad statistics.

-

Plan for healthcare and inflation. Retirement calculators often underestimate the cost of healthcare and long-term care. Factoring these in, along with steady inflation, creates a more realistic picture of future needs.

-

Address debt early. Paying down high-interest debt, including credit cards and lingering student loans, reduces stress and frees up cash flow for future savings. Mortgage acceleration strategies, such as making one extra payment per year, can also shorten loan terms and cut interest costs.

Bottom Line

The $545,424 average retirement savings number for Americans in their 40s is attention-grabbing, but it hides more than it reveals. The median balance of $213,645, the high levels of reported stress, and the broader pressures of midlife show that many households are far from feeling financially secure. For this generation, the lesson is that numbers alone don’t guarantee peace of mind. Success will depend on balancing short-term financial demands with long-term savings strategies, tackling debt, and preparing for the realities of healthcare and inflation.

In short, being “average” on paper does not equal security. For many 40-somethings, retirement planning is less about celebrating a milestone figure and more about closing the gap between savings and genuine financial confidence.