Why Your Brain Is Wired to Lose Money (And How to Fix It)

Most people don’t overspend or under-save because of poor discipline, it’s because the human brain is wired for survival, not long-term wealth. Behavioral biases like loss aversion, overconfidence, present bias, and herd mentality cause repeated money mistakes that erode savings, reduce investment returns, and delay retirement security. The solution isn’t willpower, it’s setting up systems that counteract these biases and make smart financial choices automatic.

- Loss aversion: Fear of losses leads to panic-selling and missed compounding returns.

- Overconfidence: Frequent trading reduces returns; DALBAR finds average investors underperform the S&P 500 by 3–4% annually.

- Present bias: Immediate gratification fuels undersaving; the Federal Reserve reports nearly 40% of adults feel behind on retirement.

- Herd mentality: Following hype drives buying high and selling low, seen in bubbles from dot-com stocks to crypto.

- Fixes: Automate contributions, add friction to spending, use pre-commitment tools, and track progress to stay motivated.

Do you ever open your bank account and wonder, “Why do I keep making the same money mistakes?” It’s not simply a lack of discipline, it’s rooted in how the human brain is wired. Our ancestors evolved in an environment where surviving the next day mattered far more than saving for the next decade.

That survival-driven wiring still influences how we handle modern money, often pushing us to overspend, under-save, and make emotional investment decisions. The encouraging part is that once you understand these psychological biases, you can set up practical systems that protect your financial future.

The Psychology Behind Money Mistakes

Loss Aversion

Behavioral economics research has consistently shown that losing money feels about twice as painful as gaining the same amount feels rewarding. For example, if you lose $100, the emotional sting is far stronger than the joy of finding $100. This fear leads many people to sell investments at the first sign of a downturn, even if those assets have strong long-term growth potential. Over time, this results in missing out on compounding returns.

Overconfidence Bias

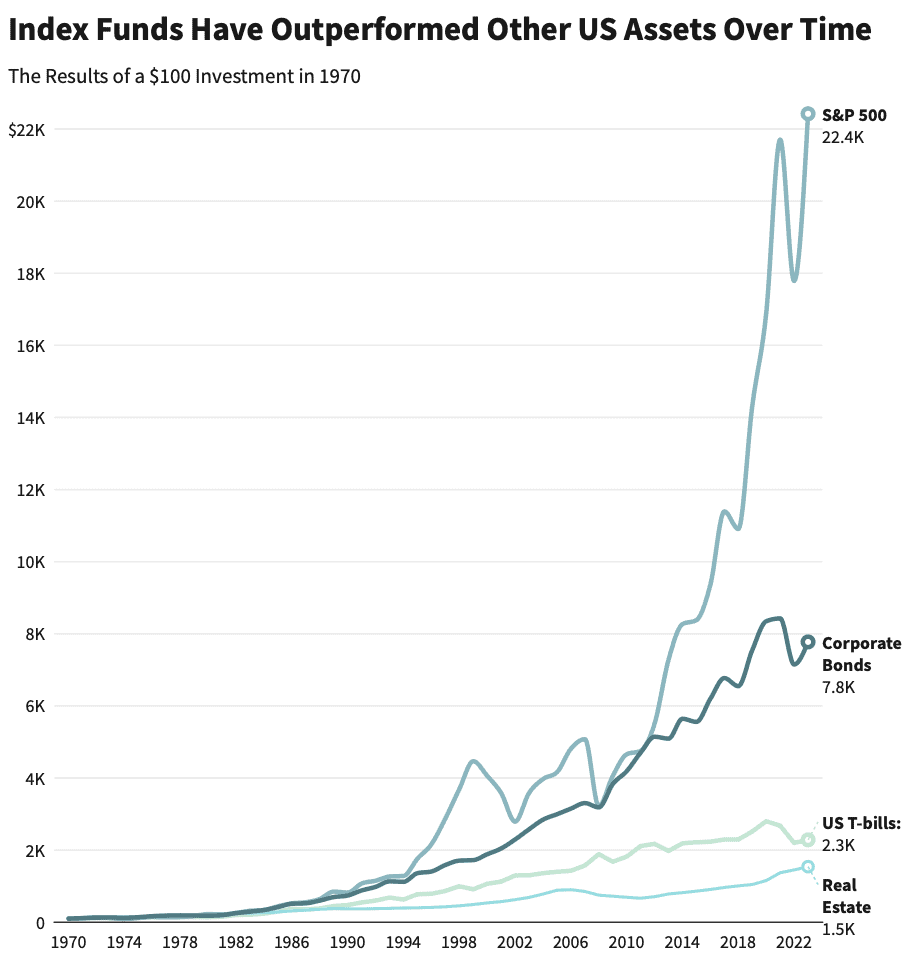

Most of us like to believe we’re smarter or luckier than the average investor. This mindset fuels excessive trading, frequent stock-picking, and speculative bets. Yet, study after study demonstrates that frequent traders often earn significantly less than those who simply invest in broad index funds. In fact, DALBAR’s annual Quantitative Analysis of Investor Behavior has shown for decades that the average equity fund investor underperforms the S&P 500 by several percentage points due to poor timing decisions driven by overconfidence.

Source: Investopedia

Present Bias

Our brains crave instant gratification. Spending $50 on dinner today feels more rewarding than adding $50 to a retirement account we won’t touch for 30 years. This preference for the present is a major driver behind America’s retirement savings gap. It explains why many people struggle to build emergency funds or stay consistent with long-term goals, even when they know saving is rational.

Herd Mentality

Humans are social by nature, and when it comes to money, we copy what others are doing. If friends or media hype a certain stock, cryptocurrency, or trend, we feel pressure to join in. This often means buying assets at their peak because “everyone else is doing it,” only to panic-sell when the trend reverses. History is full of examples, from the dot-com bubble to meme stocks, where herd behavior left ordinary investors holding the bag.

How Biases Cost You Money

These mental shortcuts don’t just cause quirky behavior, they create real financial damage:

-

Retirement Savings Gap: According to the Federal Reserve, nearly 40% of adults feel they are behind on retirement planning. Present bias, prioritizing immediate spending over long-term saving, is a key contributor.

-

Poor Investment Timing: DALBAR’s research highlights that the average investor consistently underperforms the market by 3–4% annually because of emotional trading decisions. Over a 20-year period, this gap can mean hundreds of thousands of dollars in lost wealth.

-

Everyday Overspending: Subtle behaviors like chasing sales you don’t need, keeping unused subscriptions, or upgrading to match peers stem from loss aversion and herd mentality. Over years, these “small” leaks add up to tens of thousands of wasted dollars.

Even minor money mistakes, repeated over decades, can compound into financial stress, delayed retirement, or reliance on debt.

Practical Fixes for Money Biases

The goal isn’t to “outsmart” your brain but to design systems that anticipate your tendencies and reduce opportunities for error.

Automate Savings and Investing

Automation removes temptation. Setting up recurring transfers into a savings account, IRA, or 401(k) ensures your future self is prioritized. Research shows people save significantly more when contributions are automatic rather than optional.

Add Friction to Spending

Impulse spending thrives on ease. Introduce small hurdles, like deleting saved credit cards from shopping sites, using the 24-hour rule before making online purchases, or shifting discretionary spending to cash envelopes. These minor inconveniences force you to pause and reconsider.

Use Pre-Commitment Tools

Leverage your commitment to future goals. Some employers offer “save more tomorrow” programs that automatically increase your retirement contributions with each raise. Budgeting apps can also enforce limits by locking categories once you’ve hit your spending cap, preventing emotional overspending.

Track Progress to Stay Motivated

Your brain loves feedback. Whether it’s a simple spreadsheet, a mobile app, or a debt payoff tracker, seeing progress visually keeps you engaged. Watching your savings grow or your debt shrink provides a steady stream of motivation that fights present bias.

The Bottom Line

Your brain wasn’t designed to navigate modern financial systems filled with credit cards, volatile stock markets, and decades-long retirement planning. But that doesn’t mean financial success is out of reach. By recognizing how loss aversion, overconfidence, present bias, and herd mentality influence your behavior, and putting protective systems in place, you can make smarter decisions that align with your long-term goals. The key isn’t having superhuman discipline, but building structures that make the right choice the easy choice.