The Continuous Compound Interest Formula That Doubles Your Money Faster Than Anything

Continuous compounding represents the theoretical maximum speed at which money can grow, interest added at every instant instead of monthly or daily. While no bank uses it in practice, the formula A = Pe^(rt) sets an upper limit for growth and helps investors, students, and financial planners model exponential returns. Understanding it shows why even small changes in rates or compounding frequency can meaningfully affect long-term outcomes.

- Formula:

A = Pe^(rt), where e (≈2.718) represents the limit of infinite compounding periods. - Doubling Time: At 5% interest, continuous compounding doubles money in ~13.86 years, slightly faster than ~14.2 years with annual compounding.

- Applications: Used in bond pricing, option valuation, and investment growth models, even though banks stick with daily compounding.

- Limitations: No bank compounds continuously; inflation, taxes, and fees reduce real returns; gains beyond daily compounding are negligible.

- Bottom Line: The math is elegant, but the real financial edge comes from starting early, reinvesting consistently, and letting time amplify compounding.

If you’ve ever wondered how quickly your money can grow, you’ve likely run into the concept of compound interest. It’s the force that makes savings accounts, bonds, and investments increase in value over time. But there’s an even more powerful version of this principle, continuous compounding.

Unlike regular compounding, which applies interest at fixed intervals (monthly, daily, annually), continuous compounding represents growth at every possible instant. While no bank compounds continuously in practice, the formula gives a theoretical ceiling on how fast money can grow.

Students encounter it in calculus courses, and investors use it to model scenarios. Understanding this concept not only improves your grasp of exponential growth but also highlights why even small differences in interest rates or compounding frequency can make a significant impact over the long run.

What Is Continuous Compound Interest?

To understand continuous compounding, it helps to first revisit how standard compound interest works. In a typical savings account, you don’t just earn interest on the original deposit. Instead, every period, whether that’s annually, quarterly, monthly, or daily, the interest earned gets added back to the balance. Future interest then builds on this slightly larger amount. Over time, this snowball effect accelerates growth.

Continuous compound interest takes this process to the extreme. Instead of waiting for a month or a day to pass, the balance grows at every possible instant. This constant growth may not be something banks use in practice, but it is mathematically elegant and gives us a precise formula for the upper limit of compounding.

The Formula: A = Pe^(rt)

The formula for continuous compounding is:

A = Pe^(rt)

Where:

-

A = final amount after time t

-

P = initial principal (starting amount)

-

r = annual interest rate (in decimal form, e.g., 0.05 for 5%)

-

t = time in years

-

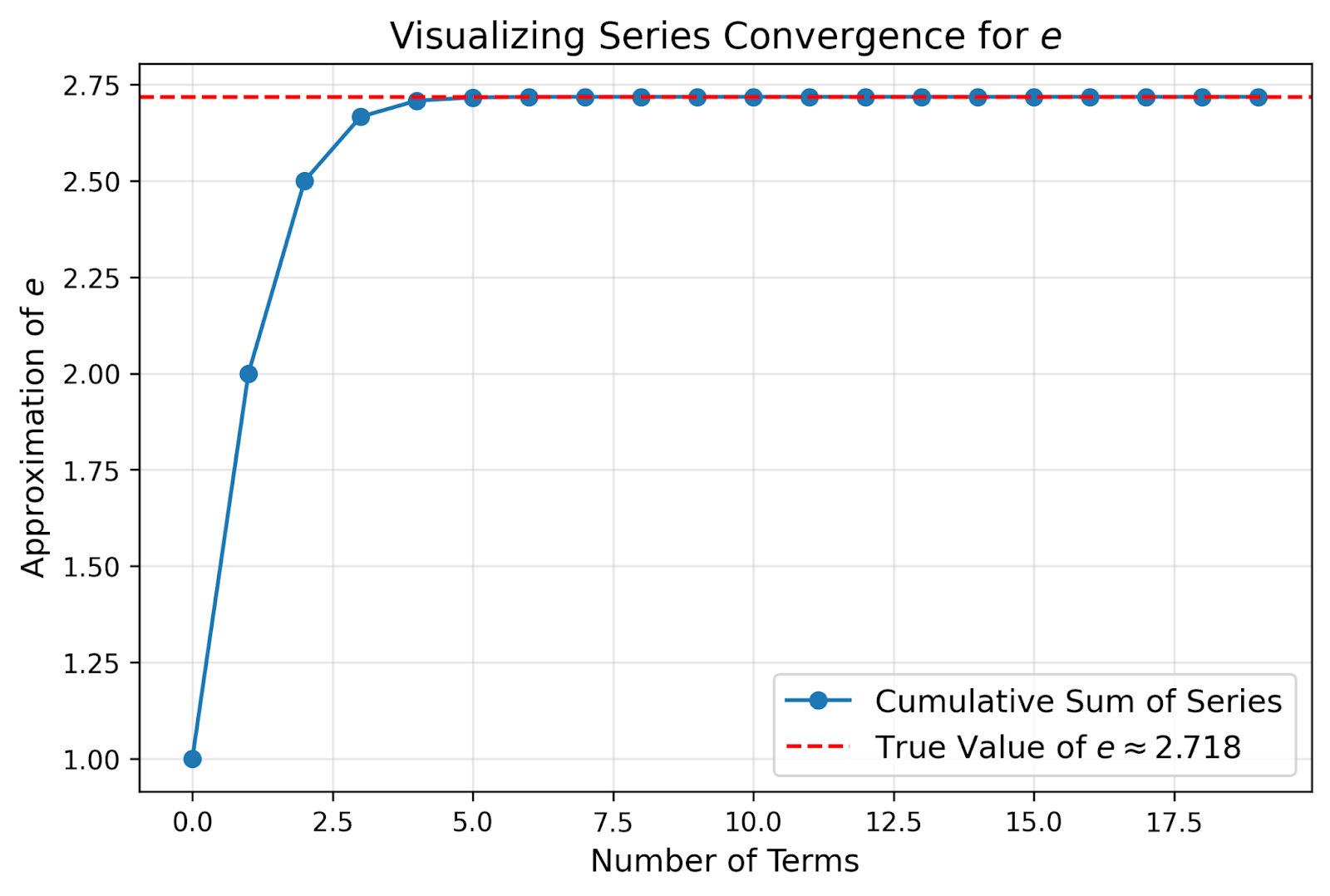

e = Euler’s number (≈ 2.718), a constant that naturally arises in exponential growth

This formula allows us to calculate the exact growth of money when compounding occurs infinitely often.

Why Euler’s Number e Appears

Euler’s number e is central to many areas of mathematics, including statistics, physics, and finance. In the context of compounding, e represents the limit reached when the number of compounding periods per year approaches infinity. Without e, continuous growth modeling wouldn’t be possible.

Source: DataCamp

Continuous vs. Regular Compounding

Source: Study Finance

Notice that the difference between daily and continuous compounding is only a few cents. That’s why most U.S. banks use daily compounding for savings accounts, it’s close enough to the theoretical maximum.

Doubling Your Money with Continuous Compounding

A frequent question is how long it takes to double an investment. With continuous compounding, the formula makes it straightforward.

Starting with: A = Pe^(rt)

If you want to double your money, set A = 2P. The equation becomes 2 = e^(rt). Taking natural logs of both sides gives ln(2) = rt, and solving for time yields t = ln(2)/r.

At an annual rate of 5% (r = 0.05), the doubling time is about 13.86 years. This is slightly faster than under annual compounding, which takes around 14.2 years. While the difference may seem small, the calculation reveals the precision continuous compounding offers for theoretical growth modeling.

Source: Federal Reserve Bank of ST.LOUIS

Real-World Applications

Even though banks don’t apply continuous compounding directly, the formula has important applications:

-

Investment Growth Models – Financial planners use it as an upper limit when projecting returns.

-

Bond Pricing – Continuous discounting helps calculate the present value of fixed-income instruments.

-

Options and Derivatives – Many pricing models in corporate finance assume continuous compounding.

-

Education – Teachers use it to illustrate exponential growth in calculus and finance courses.

For example, a financial advisor comparing savings strategies may use both daily and continuous compounding. The numbers will be nearly identical, but the exercise highlights how compounding frequency affects outcomes.

Misconceptions and Limitations

The elegance of the formula sometimes creates misconceptions. Here are the key limitations:

-

No bank compounds continuously, most use daily compounding.

-

Interest rates change, the formula assumes a fixed rate.

-

Taxes, fees, and inflation reduce actual returns.

-

Beyond daily compounding, gains are negligible.

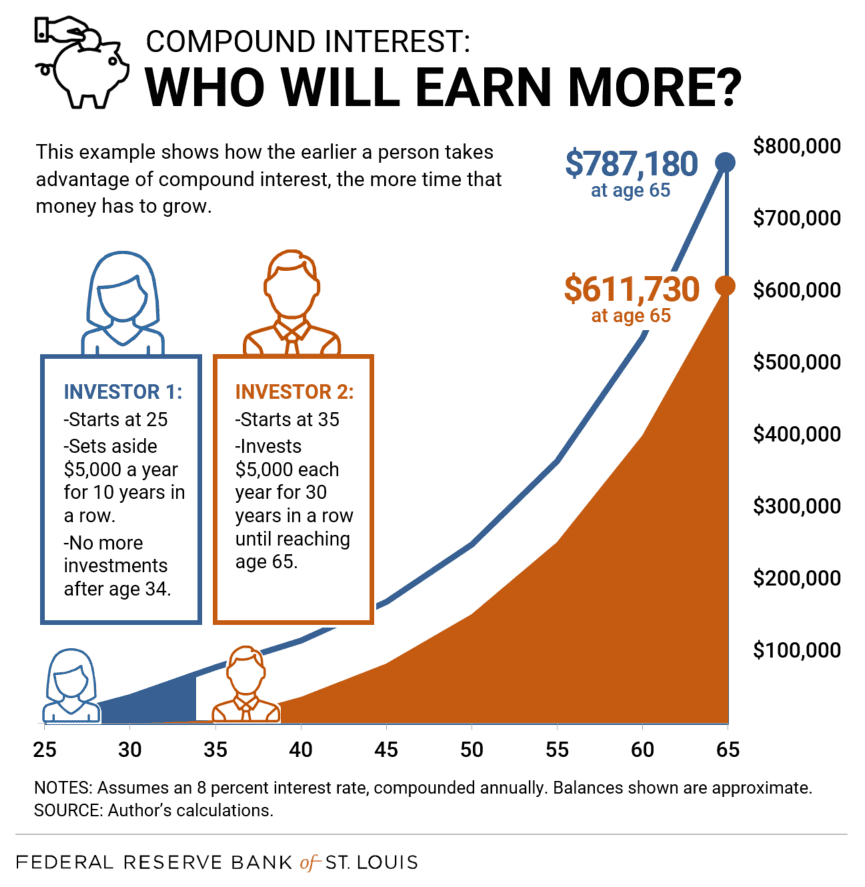

The real power of compounding lies not in continuous formulas but in starting early, investing consistently, and reinvesting returns.

Key Takeaways

The continuous compound interest formula, A = Pe^(rt), is one of the most elegant and powerful equations in finance and mathematics. It represents the theoretical limit of compounding, offers valuable insights for modeling and projections, and demonstrates the incredible effect of exponential growth.

In practice, the difference between daily and continuous compounding is only a matter of cents over many years. Still, the formula remains a cornerstone in education and finance because it teaches a timeless lesson: compounding is most effective when paired with consistency and patience.

For investors and students alike, continuous compounding provides both a mathematical ideal and a financial reminder. While no one can achieve growth at every instant, the principle behind it emphasizes why even small actions today can lead to significant financial outcomes tomorrow.