The 8 Money Habits to Adopt in the New Year

As 2025 ends with higher living costs, rising borrowing expenses, and subscription creep, the most effective way to strengthen your finances in 2026 is by adopting habits, not resolutions, that run automatically in the background. The eight habits below reflect guidance from sources like the Consumer Financial Protection Bureau, Fidelity, Vanguard, Investopedia, and the FTC, and are designed for households seeking practical, sustainable systems rather than rigid budgeting.

- Start with a realistic monthly plan by reviewing your last 60–90 days of transactions, a method supported by behavioural finance research showing consumers routinely underestimate real expenses.

- Automate savings, investing, bill pay, and debt payments, a strategy backed by Richard Thaler’s “Save More Tomorrow” findings that automation beats motivation every time.

- Run a quarterly subscription audit to catch hidden and forgotten charges; C+R Research found households spend $219/month on average despite believing it’s closer to $86. Tools highlighted by Investopedia, including Quicken Simplifi and Rocket Money, can help surface recurring costs.

- Track your net worth quarterly, a metric consistently emphasized by Fidelity as the clearest indicator of long-term financial direction.

- Build a one-month financial buffer first, aligning with Consumer.gov recommendations for starter emergency funds that reduce stress and the need for high-interest borrowing.

As 2025 ends, many households are experiencing something familiar: the sense that their financial life moved faster than they could manage. Higher living costs, rising borrowing expenses, subscription creep, and market volatility have made this a challenging year for even the most disciplined people. That’s why 2026 offers a meaningful opportunity, not for grand resolutions, but for smarter habits.

Financial habits are different from goals. Goals depend on motivation; habits depend on systems. Goals can be abandoned when life gets busy; habits continue quietly in the background, shaping outcomes even when you’re not paying attention. If you’re seeking real financial improvement in 2026, habits will do the heavy lifting.

Below are eight essential habits that can meaningfully strengthen your financial life next year, supported by behavioural science, consumer finance data, and guidance from credible sources like the Consumer Financial Protection Bureau, Fidelity, Vanguard, Investopedia, and others.

1. Start Each Month With a Realistic Plan — Not a Fantasy Budget

Most budgets fail because they’re built on wishful thinking instead of real financial behaviour. People often enter numbers they want to work rather than the numbers that truly reflect how they spend. That’s why one of the most effective habits for 2026 is shifting from rigid, idealized budgets to a monthly financial review grounded in actual data.

A practical way to start is by reviewing the past 60–90 days of bank and card transactions. Build your monthly plan based on what you really spent, not what you assume or hope your spending looks like. Behavioural finance research consistently shows that people underestimate their costs across multiple categories, especially discretionary ones.

A realistic monthly plan only needs to answer three core questions:

• What expenses are guaranteed?

Fixed obligations such as rent, utilities, subscriptions, and debt payments must be accounted for first.

• What goals or commitments must be funded this month?

This includes savings targets, medical needs, school fees, or any financial priorities coming due.

• What flexible spending is left once real numbers are acknowledged?

This determines how much room you have for lifestyle choices, discretionary purchases, or variable costs.

By grounding your financial plan in truth instead of optimism, you build a budgeting habit that steadily strengthens your financial stability. Even the most beautifully designed template can’t match the accuracy of a system rooted in your real behaviour, and that’s why this small monthly habit consistently outperforms traditional budgeting.

2. Automate Before You Motivate

The people who manage money most reliably aren’t necessarily more disciplined, they simply automate more of their financial decisions. Automation removes emotion, eliminates forgetfulness, and creates consistency without requiring daily motivation.

Behavioural economists, including Nobel laureate Richard Thaler, have shown that automation is one of the strongest predictors of long-term financial success. His well-known “Save More Tomorrow” research demonstrates that automatic savings and automatic investing outperform willpower-based strategies every time.

What Automation Looks Like in Practice

-

Automatic transfers to savings, even small weekly or monthly amounts

-

Automatic retirement contributions such as 401(k), IRA, pension, or KiwiSaver

-

Automatic debt payments to prevent missed dues and reduce interest costs

-

Automatic bill pay for fixed monthly commitments

When money moves automatically, consistency becomes effortless. Even small automated transfers early in 2026 can accumulate into meaningful savings by December, far more than most people achieve through manual effort or motivation alone.

Automation is the habit that protects you on your busiest days, not just your best ones.

3. Run a Quarterly Subscription & Recurring Expense Audit

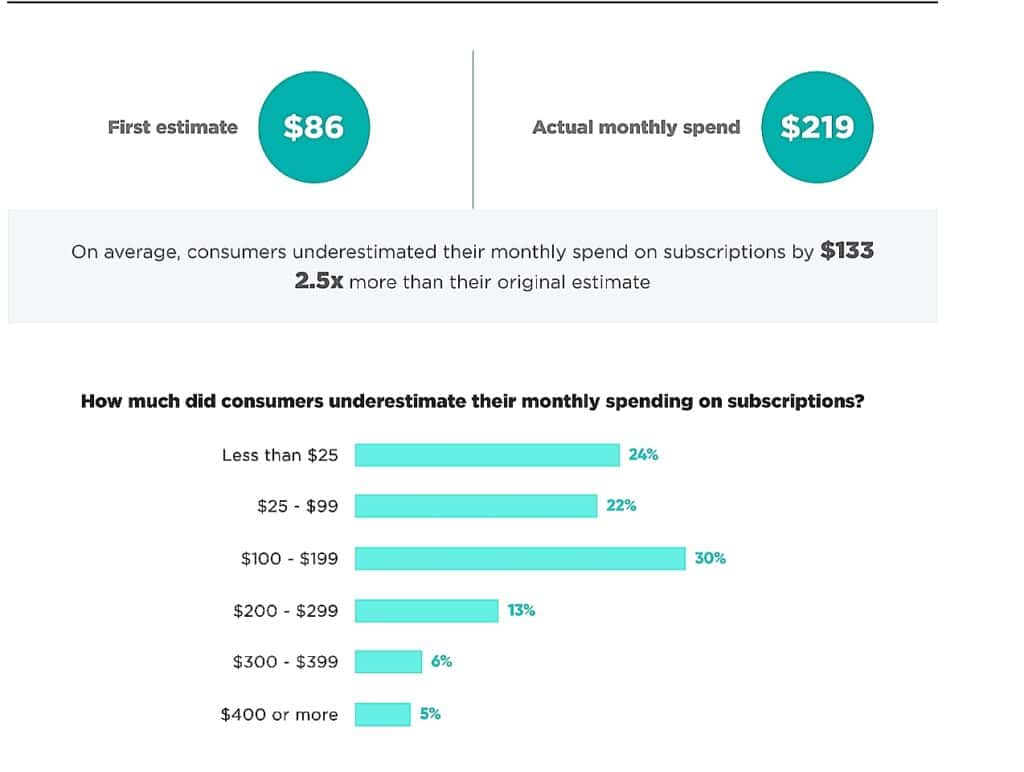

The subscription economy has quietly become one of the biggest drains on household budgets. Research from C+R Research shows a striking gap between perception and reality: consumers believed they spent about $86 per month on subscriptions, but the actual average was $219 per month.

Source: C+R Research

This makes a quarterly subscription and recurring-expense audit one of the most impactful financial habits for 2026. It forces you to revisit every charge that automatically hits your account, including:

-

App-store subscriptions

-

Cloud storage plans

-

Streaming platforms

-

Digital memberships and SaaS tools

-

Device protection and warranty add-ons

-

Free trials that quietly renewed

-

Telecom and internet add-ons you no longer use

While budgeting apps can assist with detection, a manual review is still the most accurate method. Tools like Quicken Simplifi and Rocket Money, both highlighted by Investopedia as leading budgeting apps, can help surface hidden or forgotten charges.

This habit is powerful because it disrupts the “set-and-forget” pattern companies depend on. Even cancelling two or three unnecessary subscriptions every quarter can save hundreds of dollars per year, with no lifestyle sacrifice whatsoever.

4. Separate Fun Spending From Everyday Money

Most people don’t overspend on big bills, they overspend through small, frequent, frictionless purchases. Mint/Intuit analysis found that “invisible spending” on items like coffee, snacks, subscriptions, conveniences, and entertainment can quietly consume up to 30% of a person’s discretionary income without them realizing it.

A proven habit to control this is the fun-money account, a strategy widely recommended by financial coaches. The idea is simple:

Create a separate account for discretionary spending and load it once per week or once per month. Use only this account for non-essential purchases.

Why This Habit Works

-

Guilt-free spending: The amount is pre-decided, so every purchase feels intentional rather than impulsive.

-

Automatic control: The moment the fun-money account runs low, discretionary spending naturally slows, without daily decision fatigue or strict rules.

This habit replaces emotional budgeting with a clean, predictable structure. Instead of guessing or constantly self-correcting, you create an environment where overspending becomes much harder, and financial clarity becomes much easier.

5. Track Your Net Worth Quarterly — Your Most Important Indicator

Most people focus heavily on budgeting but overlook the single most important measure of financial progress: net worth, the total of what you own minus what you owe. While budgets show short-term behaviour, net worth reveals your true long-term financial direction.

Major financial institutions like Fidelity consistently highlight net worth as the clearest indicator of overall financial health. Fidelity provides straightforward guidance on calculating and tracking net worth here:

Why Quarterly Tracking Works Best

Checking your net worth every quarter strikes the perfect balance:

-

Monthly updates fluctuate too much due to market volatility

-

Annual updates hide important trends and make course-correction slower

Quarterly tracking clearly shows:

-

Whether your savings are increasing or simply holding steady

-

Whether your debt is shrinking or quietly growing

-

Whether your investments are growing beyond your contributions

-

Whether your emergency fund is improving or stagnating

This habit transforms your mindset. Instead of seeing yourself as someone who “tries to budget,” you become someone who actively builds wealth, measures progress, and adjusts with intention.

6. Build a One-Month Buffer Before Any Other Savings Goal

Many people hesitate to start an emergency fund because traditional advice feels impossible: “Save 3–6 months of living expenses.” With rising costs, that goal can feel intimidating long before it feels achievable.

A far more realistic and powerful habit for 2026 is to start with a one-month financial buffer, a manageable amount that prevents minor emergencies from snowballing into major financial setbacks.

The U.S. Federal Trade Commission’s Consumer.gov guidance supports this approach, recommending smaller starter emergency funds because they significantly reduce financial stress and lower the risk of borrowing during a crisis:

Why a One-Month Buffer Works

A one-month safety cushion delivers immediate, meaningful benefits:

-

Financial breathing room

-

Protection against small, unexpected expenses

-

A shift out of day-to-day survival mode

Once this buffer is in place, saving becomes dramatically easier. You’re no longer making decisions from a place of stress or urgency, which means you can build additional savings, including larger emergency funds, with more confidence and stability.

7. Treat Your Debt Like a Project — Not a Life Sentence

Debt feels overwhelming when it’s unclear and unstructured, but it becomes far easier to manage when you treat it like a specific, time-bound project instead of an endless burden.

A powerful financial habit for 2026 is to create a clear debt repayment roadmap using one of two proven strategies:

-

Avalanche Method: Focus on paying off the highest-interest debt first to reduce total interest costs.

-

Snowball Method: Pay off the smallest balances first to build quick momentum and stronger motivation.

Research in consumer behavior shows that people are more likely to stay committed to repayment when they experience early wins, which is why the Snowball Method often boosts long-term follow-through.

To make this habit even more effective, turn your plan into something visual. Create a simple progress sheet, tracker, or dashboard that shows every balance and your monthly reductions. When you can see your debt shrinking in real time, the emotional weight decreases, and the project becomes a winnable challenge instead of a lifelong struggle.

8. Align Your Spending With What Actually Makes Your Life Better

One of the most transformative financial habits for 2026 is learning to spend with intention, not impulse. Instead of focusing only on cutting costs, the real goal is to direct your money toward the purchases that genuinely make your life better.

A highly effective approach is to conduct a quarterly “joy audit”, a simple reflection on where your money went and how those purchases made you feel. Research on financial well-being shows that intentional spending, especially on experiences, relationships, skills, and health, leads to more lasting happiness than impulse buys or forgettable purchases.

Questions to Guide Your Quarterly Review

Ask yourself every quarter:

-

What spending truly added value to my life?

These are purchases that improved your well-being, reduced stress, strengthened relationships, or supported your personal growth. -

What spending felt empty, automatic, or unnecessary?

Think about charges you barely remember, habitual purchases, convenience buys, or subscriptions you no longer use. -

What did I wish I had invested more in?

This could include rest, learning, travel, health, hobbies, or experiences that enrich your daily life.

When you routinely reflect on these answers, your spending becomes aligned instead of accidental. You create a financial life where your money supports your goals, your values, and the lifestyle you genuinely want, not one driven by impulse or routine.

The Real Promise of 2026: A Year of Quiet, Compounding Wins

Real financial success rarely comes from one dramatic choice. People don’t suddenly become debt-free, build wealth, or feel in control of their money overnight. Lasting progress comes from consistent systems, smart behaviours, and daily habits that compound quietly over time.

In 2026, adopting even a handful of simple practices, automated savings, quarterly money audits, intentional spending, a separate fun-money budget, and regular net-worth tracking, can dramatically shift your financial stability and confidence.

The goal isn’t to be perfect. It’s to build momentum. When small habits repeat for 12 straight months, they compound into meaningful, long-term financial growth. These quiet, steady wins are what truly transform your money life in 2026.