Killing the Auto-Renew: The Simplest Financial Win Most People Ignore

Most Americans waste over $1,400 a year on unused subscriptions, often without realizing it. A weekend audit can reveal hundreds in hidden recurring charges from apps, streaming services, and trials that quietly renew. With the FTC reporting record complaints about “subscription traps,” and the average person underestimating monthly costs by more than 100%, regular audits are one of the most effective ways to reclaim cash and control in 2025.

- Average loss: Consumers spend about \$1,416 per year on subscriptions, with half admitting to paying for services they no longer use.

- Psychology at play: Behavioral biases like sunk cost fallacy and loss aversion keep users subscribed long after value fades.

- Legal changes: The FTC’s Click-to-Cancel Rule, initially set for 2025, aims to make unsubscribing as easy as signing up, despite court delays.

- Practical fix: Conduct a six-month statement review, use tools like Rocket Money or Trim, and adopt a quarterly “subscription audit.”

- Bottom line: Canceling unused services can free up \$2,000+ annually, money better invested, saved, or spent intentionally.

Last weekend, I finally tackled something I’d been putting off for months, reviewing my bank statements line by line. What I discovered was shocking: more than $3,000 a year, that’s $250 every month, was vanishing into unused and forgotten subscription services.

A meditation app I’d opened twice. A meal kit delivery I kept forgetting to cancel. A second premium music service I didn’t even need. And several mystery charges I had to Google just to identify.

After two hours of cutting through the clutter, I reduced my recurring costs to under $500 a year, putting $2,500 back in my pocket. That’s real money that can go toward savings, travel, or even investments for the future.

If this scenario sounds familiar, you’re not alone. The subscription trap is one of the biggest hidden drains on personal finances today. With Americans averaging 8.2 active subscriptions and spending over $1,400 annually, tracking recurring charges has never been more essential for smart money management and financial freedom.

The Subscription Economy’s Dirty Secret

Americans now maintain an average of 8.2 active subscriptions, spending roughly $1,416 per year, according to 11:FS’s 2025 subscription economy report. Nearly one-third of consumers (32%) manage ten or more recurring charges, from streaming services and apps to meal kits and software plans.

But here’s the catch: more than half of Americans (54.9%) admit they’re still paying for at least one subscription they no longer use, based on findings from a Self Financial survey. On average, people waste between $10.57 and over $30 each month on forgotten or unused subscriptions, depending on the study year.

Source: Self Financial survey

That may not sound like much, but it adds up, more than $125 per person annually simply vanishing into digital limbo. With U.S. adults spending billions every year on services they rarely touch, these hidden costs represent one of the most underestimated leaks in personal budgets.

While some online reports estimate the total loss from forgotten subscriptions estimated at $21.8 billion annually, this figure varies widely and isn’t backed by a single definitive study. What is clear, however, is that regular subscription audits can put hundreds, or even thousands, back in your pocket each year.

How Did We Get Here?

The subscription economy didn’t explode by accident, it was engineered for maximum profitability. Companies perfected a formula built on psychology: make signing up effortless, automate the billing, and make canceling just inconvenient enough that most people never bother.

According to the Federal Trade Commission (FTC), consumer complaints about “negative-option” billing and subscription traps have surged. In 2021, the FTC averaged 42 complaints per day; by 2024, that number had jumped to nearly 70 per day, a 67% increase in just three years.

The biggest culprit? The so-called “free trial.” Surveys reveal that around half of Americans forget to cancel trial subscriptions before they convert to paid plans. A 2024 survey by Self Financial found nearly 65% of people had been charged for a service they meant to cancel.

Industry experts note that “free trials” often act as a gateway to recurring charges, especially when cancellation options are buried behind multiple clicks or vague settings. The FTC’s proposed Click-to-Cancel Rule aims to change that by forcing companies to make unsubscribing as simple as signing up.

In short, the subscription boom isn’t just convenience, ggit’s a masterclass in behavioral design that keeps consumers paying long after the value fades.

The Psychology of Auto-Renew

Why do so many of us keep paying for subscriptions we rarely use? It’s not about laziness, it’s about psychology. Modern subscription models are designed to exploit deep-rooted cognitive biases that shape our decision-making.

Loss aversion: Once we’ve paid for something, we irrationally fear “losing” access, even if we never use it.

Sunk cost fallacy: “I’ve already paid for six months, I should keep it to get my money’s worth.”

Default bias and decision fatigue: Canceling takes effort; keeping a subscription takes none. Faced with endless daily choices, our tired brains take the path of least resistance, doing nothing.

The “someday” illusion: “I’ll use it more next month.” But in reality, most subscribers never do, letting unused services quietly drain their budgets.

According to CivicScience research, 62% of streaming users feel overwhelmed by the number of options, showing clear signs of subscription fatigue. Yet the average number of paid services per person has climbed from 2.4 to 3, a 25% increase, fueled by password-sharing crackdowns and market shifts highlighted in Netflix’s 2024 growth report.

Source: Civic Science

The result? Millions continue paying for digital services out of habit rather than value, a powerful example of how behavioral economics keeps the subscription economy thriving.

The Real Cost: Beyond the Dollars

That $3,000 you’re losing every year to unused subscriptions isn’t just money, it’s opportunity cost.

If you invested that amount instead, the difference over time would be staggering. Investing $3,000 annually at an average 8% return could grow to more than $340,000 in 30 years, according to compound interest calculations. That’s a retirement fund, a dream vacation, or the down payment on a home, all slipping away in the background of your monthly auto-payments.

And it’s not only about wealth. It’s about freedom. Freedom to build an emergency fund, pursue a passion project, or take a lower-stress job without financial pressure.

When I finally realized I’d been paying $29.99 a month for a productivity app I opened maybe twice a year, it hit me: I wasn’t just wasting money, I was trading nearly 40 hours of my working life every year for nothing in return. Cutting out forgotten subscriptions doesn’t just save cash, it buys you back your time, your options, and your peace of mind.

The Subscription Audit: Your Action Plan

Here’s how to take back control of your finances, and stop paying for subscriptions you don’t use.

Step 1: Find Everything

Don’t rely on memory. Go forensic:

-

Review at least 6 months of statements: Check every bank and credit card account. Subscriptions can bill monthly, quarterly, or annually, a one-month snapshot won’t catch everything.

-

Search your email: Use keywords like “subscription,” “membership,” “auto-renew,” “trial ending,” and “payment confirmation.”

-

Check your devices: iOS users can go to Settings > [Your Name] > Subscriptions, while Android users can open Google Play > Payments & Subscriptions > Subscriptions (note: direct website subscriptions won’t appear there).

-

Use a subscription tracker: Apps like Rocket Money (formerly Truebill), Bobby, or Trim can automatically identify recurring charges.

Recent Canadian surveys show the average person thinks they have only 4 subscriptions, but actually pays for closer to 8, with 66% discovering charges they’d completely forgotten about.

Step 2: The Brutal Evaluation

For each subscription, ask yourself three questions:

-

Have I used this in the last 30 days? If no, it’s gone.

-

Does this serve a current goal or need? Not a hypothetical future one, a real one.

-

Would I pay for this if I had to choose it today? If the honest answer is “nothing,” cancel it.

These simple filters cut emotional attachment and expose what’s really worth keeping.

Step 3: The Cancellation Gauntlet

This is where many companies make it difficult. Common complaints include repeated sales pitches, being passed from agent to agent, and charges that continue even after confirmation.

Here’s how to push through:

-

Start with the source: Log in to the service’s website or app and look for Account Settings > Billing > Subscription > Cancel.

-

Know your rights: The FTC’s proposed “Click-to-Cancel” rule, finalized in October 2024, aimed to make cancellation as easy as signup. Enforcement was later delayed to July 2025 and ultimately vacated by a U.S. court, but many states are still pursuing similar consumer-protection laws.

-

Document everything: Take screenshots, save confirmation emails, and note call dates/times. If charges continue, you’ll need a paper trail.

-

Use clear language: Tell support, “I want to cancel my subscription effective immediately. I do not wish to hear retention offers.”

-

Escalate if necessary:

-

Ask for a supervisor

-

Reference the FTC’s rule or your state’s automatic-renewal law

-

File a complaint at ReportFraud.ftc.gov

-

Post publicly on social media, companies often respond faster there

-

-

Last resort: Call your credit-card company to dispute continued charges or block the merchant. Use cautiously, as it may violate the service’s terms.

Step 4: Prevent Future Leaks

Once you’ve cleaned house:

-

Set reminders: Add a calendar alert three days before each free trial ends and schedule a quarterly “subscription audit.”

-

Use virtual cards: Services like Privacy.com let you generate single-use or trial-only card numbers that automatically decline renewals.

-

Choose annual plans only when certain: Annual billing usually costs less, but only if you’ll use the service all year.

-

Adopt a “one-in, one-out” rule: Every new subscription should replace an old one.

A few hours of auditing can save you hundreds, even thousands, every year. With forgotten subscriptions costing consumers billions annually, treating this as a recurring financial check-up can be one of the smartest money habits you build.

The Hidden Subscriptions You’re Probably Missing

Based on my audit and recent consumer reports, here are the sneakiest culprits quietly draining your wallet:

-

Free trials that weren’t: Most “no credit card needed” trials still require one and auto-renew into paid plans if you forget to cancel. The Federal Trade Commission warns that these offers rely on inertia to keep you paying.

-

Amazon Subscribe & Save: Auto-ship items from Amazon’s Subscribe & Save can pile up fast, leaving you with products you no longer use or need. Many shoppers forget to pause deliveries, turning convenience into waste.

-

In-app subscriptions: Hidden in your phone, these keep billing through Apple or Google Play even after you delete the app. Because charges appear under generic names, they’re easy to miss on bank statements.

-

Premium upgrades you didn’t request: Services frequently roll users into new pricing tiers automatically. The FTC’s proposed rule aims to curb these “negative-option” renewals that charge more unless you actively opt out.

-

Gym memberships: A timeless trap. The Better Business Bureau still receives thousands of annual complaints about cancellation barriers and hidden renewal terms, keeping members stuck long after they’ve stopped going.

-

Bundled subscriptions: That “free” Prime Video with your Amazon Prime shipping isn’t free if you rarely shop online. Bundles work by keeping you subscribed for one feature while quietly billing for the rest.

When Canceling Gets Ugly

Some companies turn cancellations into an obstacle course. The FTC calls these dark patterns, design tricks that bury cancel buttons under menus or disguise them as “pause” options to keep you subscribed longer. In 2022, the FTC fined Vonage $100 million for making customers call multiple agents, pushing repeated offers, and charging even after cancellations.

Some companies add surprise “final billing cycles” or early-termination fees, extending payments weeks beyond cancellation. Under the FTC’s updated rules, firms can now face fines up to $53,088 per violation. If canceling feels intentionally difficult, document everything and report it through the FTC complaint portal.

The Subscription-Pause Alternative

Here’s an emerging trend that actually makes sense: subscription pausing. Data shows that the median percentage of subscribers rejoining a service they previously canceled rose to 34.2% in 2024, up from 29.8% in 2022, evidence of what experts now call “subscription cycling.”

Rather than fully canceling services you might only want seasonally, consider whether they offer a pause option. Many streaming platforms now recognize fluctuating viewing habits and allow users to preserve watch history and preferences without paying during inactive months.

However, while consumer demand for flexible billing is growing, only a minority of companies currently provide true pause features, even though over half of consumers say they would prefer to pause instead of cancel if given the choice.

My Results: The $2,500 Freedom

After my weekend audit, here’s what I kept:

- Netflix: $15.99/month (family uses it constantly)

- Spotify: $10.99/month (use it daily)

- New York Times: $4/week (regularly read)

- Cloud storage: $9.99/month (essential for work)

Total: $499.08 annually

Here’s what I canceled:

- Four streaming services I watched maybe once a month

- Three fitness apps I’d opened a combined five times

- Two meal kit subscriptions I kept forgetting to pause

- A meditation app from a long-abandoned New Year’s resolution

- Several “productivity” tools that did the opposite

- A coffee subscription box I no longer use

- The entire process took about 90 minutes.

Annual savings: $2,519

But the real win wasn’t just financial, it was clarity. No more surprise charges. No more guilt about unused apps. No more mental clutter from accounts I’d forgotten existed.

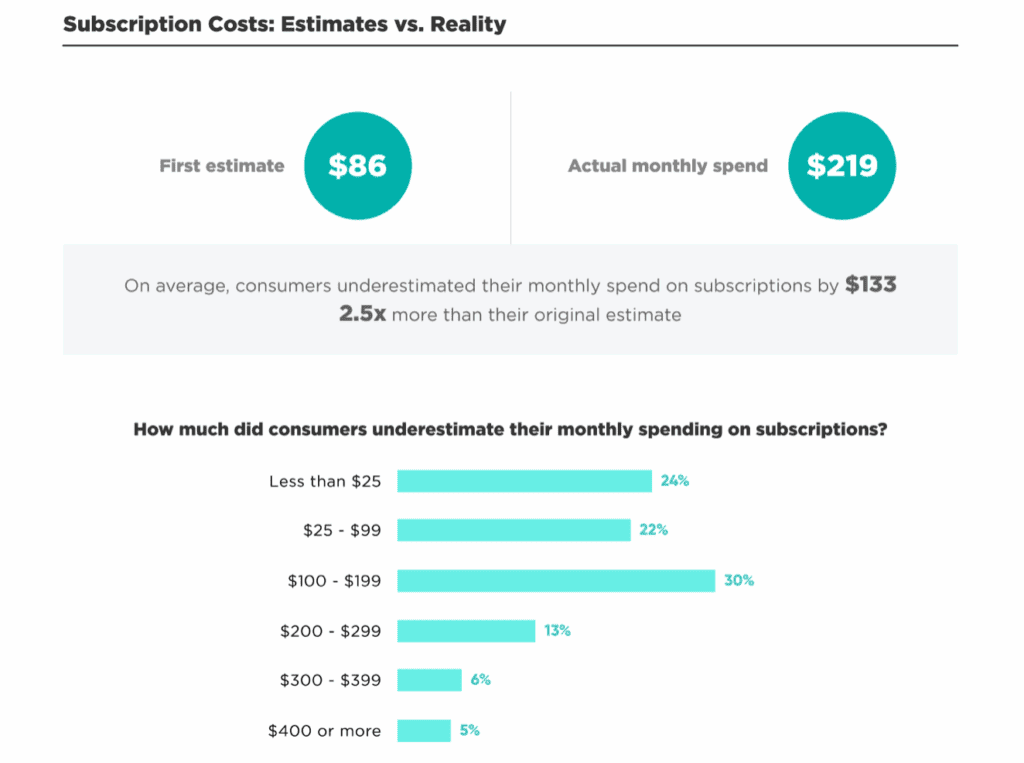

Recent research supports this outcome: the average consumer underestimates their subscription spending by over 100%, often believing they pay about $86 a month when the real total is closer to $219, according to C+R Research. Cutting back doesn’t just save money, it restores control over your finances and peace of mind.

Source: C+R Research

The Bigger Picture

The subscription economy isn’t inherently bad, when done right, it offers real value: you pay only for what you use, when you use it, without heavy upfront costs. The real issue arises when companies exploit consumer inertia and lack of transparency to collect payments for services that no longer deliver value.

Globally, the subscription economy is projected to surpass $1.5 trillion by 2025, underscoring that this model isn’t disappearing anytime soon. That’s why it’s crucial to treat every subscription like any other financial commitment, with intention, oversight, and regular reviews.

Recent data from FT Strategies and Mastercard shows 73% of subscribers want a single platform to manage all their subscriptions, yet only 2% currently use one. Meanwhile, a U.S. Bank survey found that 72% of consumers wish they could manage every subscription directly through their banking app, highlighting a major opportunity for financial institutions to simplify the subscription experience.