High Deductible Health Plans: Who They’re For, What They Cost, and How They Affect Your Care

High Deductible Health Plans (HDHPs) continue to expand across U.S. employers as a lower-premium alternative to traditional coverage. For 2025, the IRS defines HDHPs as those with at least a $1,650 individual deductible or $3,300 for families, and out-of-pocket maximums of $8,300 and $16,600, respectively. These plans pair with Health Savings Accounts (HSAs), offering major tax advantages but higher upfront medical costs. Understanding how HDHPs balance risk, cost, and tax benefits is essential before open enrollment.

- Tax Benefit: HDHPs qualify for HSAs, which provide triple tax advantages, pre-tax contributions, tax-free growth, and tax-exempt withdrawals for qualified medical expenses.

- Best for: Healthy, higher-income individuals with emergency savings and minimal healthcare needs; ideal for long-term HSA investors.

- Risk Factors: Not recommended for those with chronic conditions, regular prescriptions, or limited savings, delayed care and higher costs are common.

- Research Insight: Studies show HDHPs reduce both necessary and unnecessary care; lower-income enrollees face worse health outcomes.

- Decision Tip: Compare premiums, expected medical use, and your ability to fund an HSA before choosing an HDHP during open enrollment 2025.

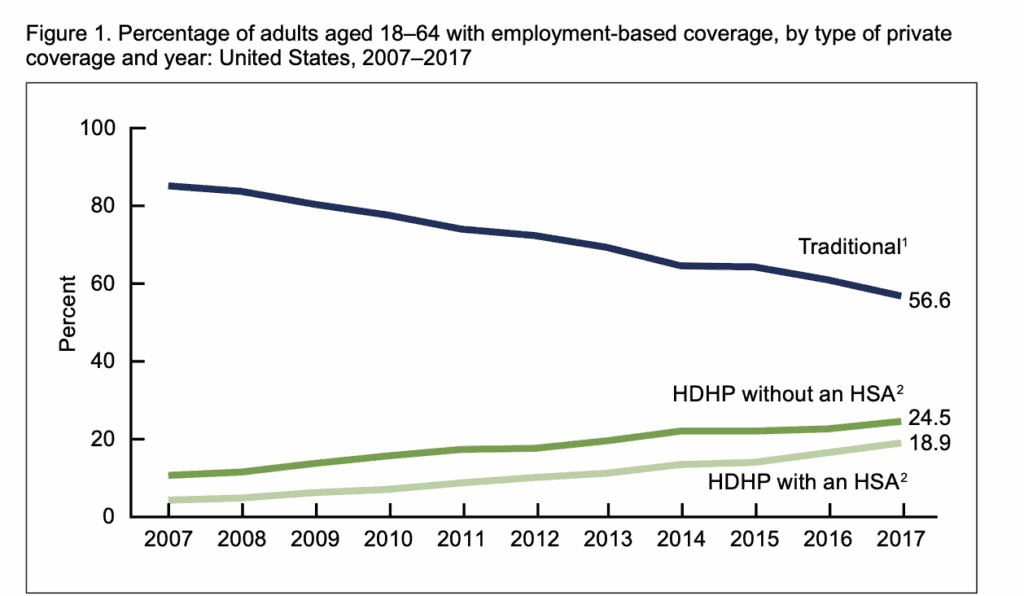

High deductible health plans (HDHPs) have become increasingly common in U.S. health insurance. According to data from the Centers for Disease Control and Prevention (CDC), enrollment among adults under 65 rose from roughly 4% in 2007 to nearly 19% by 2017, and that share has continued climbing as employers push for lower premiums. Understanding how these plans work, who benefits most, and what risks they pose is crucial during open enrollment.

What Is a High Deductible Health Plan?

An HDHP is a type of health insurance that features higher deductibles and lower monthly premiums compared to traditional plans. The deductible is the amount you must pay out of pocket for covered medical services before your insurance begins sharing costs.

For 2025, the Internal Revenue Service (IRS) defines HDHPs as plans with minimum deductibles of $1,650 for individual coverage or $3,300 for family coverage. The maximum out-of-pocket limit is $8,300 for individuals and $16,600 for families. For 2026, those thresholds rise to $1,700 and $3,400 for deductibles, with out-of-pocket caps of $8,500 and $17,000, respectively.

Unlike traditional plans, HDHPs don’t cover most non-preventive services until you’ve met the deductible. This means patients cover the full cost of doctor visits, tests, and prescriptions upfront. After reaching the deductible, co-insurance (a percentage of ongoing costs) applies until you hit the out-of-pocket maximum, at which point the plan covers 100% of remaining eligible expenses for the year.

However, most HDHPs still cover preventive services, such as annual checkups, immunizations, and certain screenings, at no cost before the deductible, as required under the Affordable Care Act (ACA).

Who Provides HDHPs?

All major health insurance companies offer high deductible plans, including Aetna, UnitedHealthcare, Cigna, Anthem, and Blue Cross Blue Shield affiliates. HDHPs are available as HMO, PPO, POS, or EPO plans depending on the insurer and specific product.

These plans are offered through employers, the Health Insurance Marketplace, and directly from insurance companies for individual purchase. Many employers now offer HDHPs as their only option or as an alternative to traditional plans during open enrollment.

The Tax Advantage: HSA Eligibility

One of the biggest benefits of HDHPs is their eligibility for a Health Savings Account (HSA), a powerful, tax-advantaged tool that allows participants to save pre-tax dollars for qualified medical expenses.

Under IRS rules, only individuals enrolled in qualified HDHPs can open and contribute to HSAs. The accounts offer a triple tax benefit:

-

Contributions are tax-deductible.

-

Earnings grow tax-free.

-

Withdrawals for qualified medical expenses are tax-exempt.

For 2025, contribution limits are $4,300 for individuals and $8,550 for families. Those age 55 or older may add a $1,000 catch-up contribution. Funds roll over indefinitely, remain yours regardless of job changes, and can even serve as a retirement asset, after age 65, non-medical withdrawals are taxed as regular income but face no penalties.

Who Benefits Most from HDHPs

High deductible plans work best for specific populations. Healthy individuals who rarely need medical care beyond preventive services benefit from significantly lower monthly premiums. If you visit the doctor once annually for a checkup and have no chronic conditions requiring ongoing treatment or medication, an HDHP can generate substantial savings.

Higher earners with emergency funds to cover the deductible if needed gain the most. The combination of lower premiums and HSA tax benefits provides significant financial advantages. The ability to max out HSA contributions and invest those funds for long-term growth creates another tax-advantaged retirement savings vehicle.

Young, healthy workers without families often find HDHPs advantageous. They pay minimal premiums while building HSA balances that can grow over decades.

Who Should Avoid HDHPs

High deductible plans create financial and health challenges for certain populations. Individuals with chronic conditions requiring regular care, frequent doctor visits, or ongoing medication face substantial out-of-pocket costs before reaching their deductible. Research shows these patients often delay or forgo necessary care due to cost concerns.

Families with young children who need frequent sick visits and potential emergency room visits may spend more under HDHPs than traditional plans despite lower premiums.

Lower income individuals struggle most with HDHPs. Studies consistently demonstrate that cost-sharing through high deductibles disproportionately affects lower-income populations, leading to delayed care, medication non-adherence, and worse health outcomes. Anyone without emergency savings to cover the deductible faces risk. A serious medical emergency could require paying several thousand dollars before insurance coverage begins, creating financial hardship.

The Healthcare Outcomes Research

Extensive research examines how HDHPs affect healthcare utilization and outcomes, revealing concerning patterns. A systematic review of diabetes care published in the Journal of Managed Care & Specialty Pharmacy found that HDHPs lower spending at the expense of reduced high-value diabetes monitoring, routine care, and medication adherence, potentially contributing to increases in acute healthcare utilization.

Studies show patient out-of-pocket costs for recommended diabetes screenings doubled under HDHPs, while total healthcare expenditures increased 49.4% for HDHP enrollees compared to traditional plan enrollees. Reductions in disease monitoring and routine care were greatest among lower-income patients.

Research on cardiovascular medication adherence published in Circulation found that HDHP enrollment affects medication-taking behavior, with studies documenting disparate impacts across different populations.

Source: AHAIASA Journals

A comprehensive Health Affairs review concluded that HDHPs were associated with significant reductions in preventive care in seven of twelve studies and significant reductions in office visits in six of eleven studies, leading to reductions in both appropriate and inappropriate care.

Some research shows more favorable results. One study found HDHPs led to 13.7% reductions in low-value outpatient services spending and 5.2% reductions in overall outpatient spending, with some evidence suggesting HDHPs disproportionately reduce low-value spending relative to overall spending.

Source: PMC

The RAND Corporation’s analysis found that while evidence suggests the health of the overall population may not change with increased cost sharing, lower income and less healthy individuals in plans with high cost sharing tend to experience poorer health outcomes than similar individuals with low or no cost sharing.

How to Decide if an HDHP Is Right for You

Choosing an HDHP requires careful consideration of your health status, finances, and risk tolerance.

-

Estimate annual costs. Compare premiums and expected out-of-pocket expenses across HDHPs and traditional plans.

-

Evaluate your health needs. Chronic conditions, planned surgeries, or regular prescriptions usually make standard plans more cost-effective.

-

Check your emergency savings. You should have enough to cover the full deductible if needed.

-

Factor in HSA potential. If you can fully fund your HSA, the tax benefits can offset higher short-term costs.

Risk-averse individuals often prefer predictable monthly premiums, while those with stable health and financial cushions may benefit from the long-term savings an HDHP provides.

The Bottom Line

High deductible health plans offer lower premiums and valuable HSA eligibility but require higher out-of-pocket spending before insurance coverage begins. They work well for healthy individuals with financial resources to cover potential deductibles and the discipline to maximize HSA contributions.

Research indicates HDHPs reduce healthcare utilization and costs but often do so by limiting access to necessary care, particularly among lower-income populations and those with chronic conditions. The plans can widen existing healthcare disparities.

For those who can afford the potential out-of-pocket costs and primarily need preventive care, HDHPs paired with HSAs provide significant financial advantages. For those with ongoing healthcare needs, limited financial resources, or chronic conditions, traditional plans with higher premiums but lower deductibles typically provide better value and healthcare access.

The key is matching your insurance choice to your actual healthcare needs, financial situation, and risk tolerance rather than simply choosing the lowest premium option.