Bank Overdraft Protection: How New CFPB Rules Could Save You $225 Per Year (Or End the Service Entirely)

In December 2024, the Consumer Financial Protection Bureau finalized a rule that would have capped overdraft fees at large U.S. banks and credit unions at as little as $5 per transaction, a change the agency estimated could save affected households about $225 per year. That rule never took effect. In May 2025, Congress used the Congressional Review Act and President Donald Trump signed the resolution overturning it, preserving current overdraft practices and blocking the CFPB from issuing a similar rule without new congressional approval.

- The repealed rule would have applied to banks and credit unions with more than $10 billion in assets and capped overdraft fees at $5, actual cost, or required treatment as credit under the Truth in Lending Act.

- Without the rule, banks remain free to charge overdraft fees that typically range from about $27 to $35 per transaction.

- Even without federal caps, overdraft revenue at large banks fell roughly 45–50% from 2019 to 2023, driven by competitive pressure and voluntary reforms.

- Most overdraft fees are paid by a small share of customers who overdraw frequently, while many banks now offer fee-free buffers, grace periods, or no-overdraft accounts.

In December 2024, the Consumer Financial Protection Bureau finalized what appeared to be a major consumer-focused reform: a new overdraft rule that would have limited fees at large banks and credit unions to as little as $5, a change the agency estimated could save households that pay overdraft fees roughly $225 per year on average. The regulation was scheduled to take effect in October 2025.

That rule, however, never took effect. In May 2025, Donald Trump signed a Congressional Review Act resolution passed by Congress that nullified the regulation before implementation, leaving existing overdraft practices intact. As a result, banks and credit unions remain free to charge overdraft fees that often exceed $30 per transaction. The swift reversal underscores a continuing national debate over whether overdraft programs function primarily as a necessary short-term safety net or as a long-standing profit center built on consumer financial distress.

The Rule That Wasn’t

The CFPB’s proposed regulation would have applied to financial institutions with more than $10 billion in assets, covering the nation’s largest banks and credit unions. Under the proposal, these institutions would have had three compliance options: cap overdraft fees at $5, limit fees to the institution’s actual cost of providing the service, or treat overdraft coverage as credit subject to Truth in Lending Act disclosure requirements.

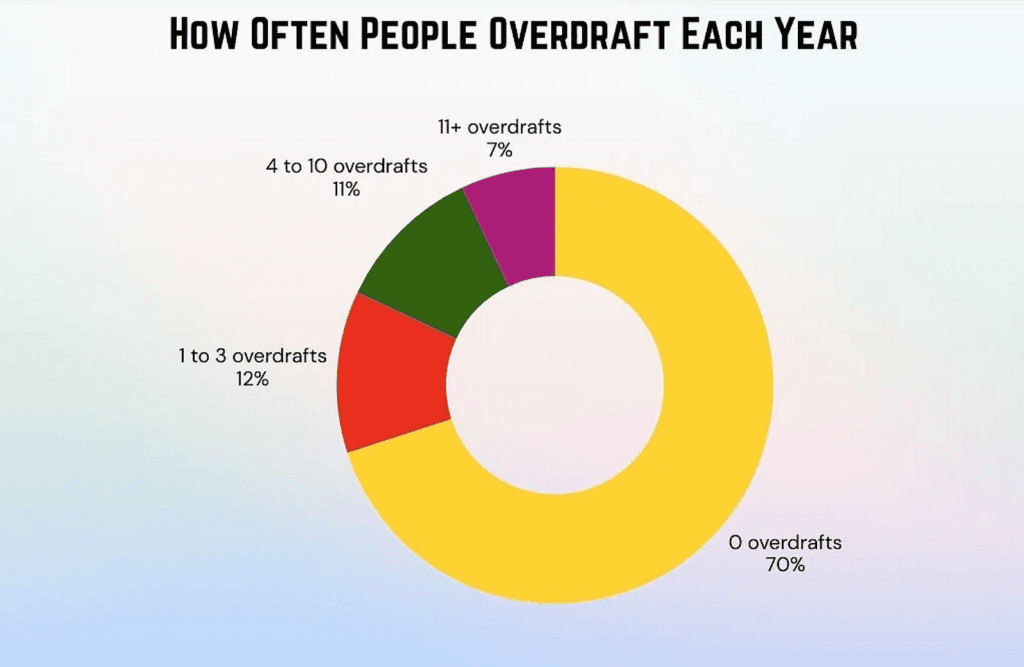

The regulation sought to overturn a longstanding regulatory interpretation dating back to the late 1960s that excluded overdraft fees from being treated as finance charges under federal lending law. CFPB Director Rohit Chopra argued that this interpretation had become outdated as overdraft programs evolved into a major source of fee revenue. The agency estimated that the rule could save consumers up to $5 billion annually, with most benefits accruing to a small segment of customers, roughly 9% of account holders, who generate close to 80% of all overdraft fees by overdrawing their accounts more than ten times per year.

Financial institutions strongly opposed the proposal. Banking trade groups argued that the CFPB had exceeded its statutory authority and that overdraft services do not constitute credit under existing law. They warned that imposing strict fee caps or reclassifying overdraft coverage as credit could lead banks to curtail or eliminate overdraft programs altogether, potentially pushing some consumers toward higher-cost alternatives such as payday lending.

Congressional Republicans Step In

The banking industry’s concerns quickly found receptive ears in Congress. In February 2025, Republican leaders in both chambers introduced Congressional Review Act (CRA) resolutions to overturn the Consumer Financial Protection Bureau’s overdraft rule. The effort was led by Tim Scott, chairman of the Senate Banking Committee, and French Hill, chairman of the House Financial Services Committee. Both lawmakers characterized the regulation as a form of “government price controls,” arguing it would limit consumer choice and restrict access to short-term liquidity.

The Senate approved the resolution in March 2025 by a 52–48 vote, followed by passage in the House in April by a 217–211 margin. Donald Trump signed the measure into law in May 2025, effectively nullifying the rule before it could take effect.

Under the Congressional Review Act, the Consumer Financial Protection Bureau is now prohibited from issuing a “substantially similar” overdraft rule in the future without explicit authorization from Congress.

What Banks Actually Make From Overdrafts

Despite predictions of financial disruption, bank overdraft revenue has already declined sharply in recent years without new federal mandates. According to data from the Consumer Financial Protection Bureau (CFPB), overdraft and non-sufficient funds (NSF) fee revenue at large banks fell from roughly $12 billion in 2019 to about $6 billion in 2023, a decline of roughly 45–50%, driven largely by voluntary changes as banks responded to competitive pressure and regulatory scrutiny.

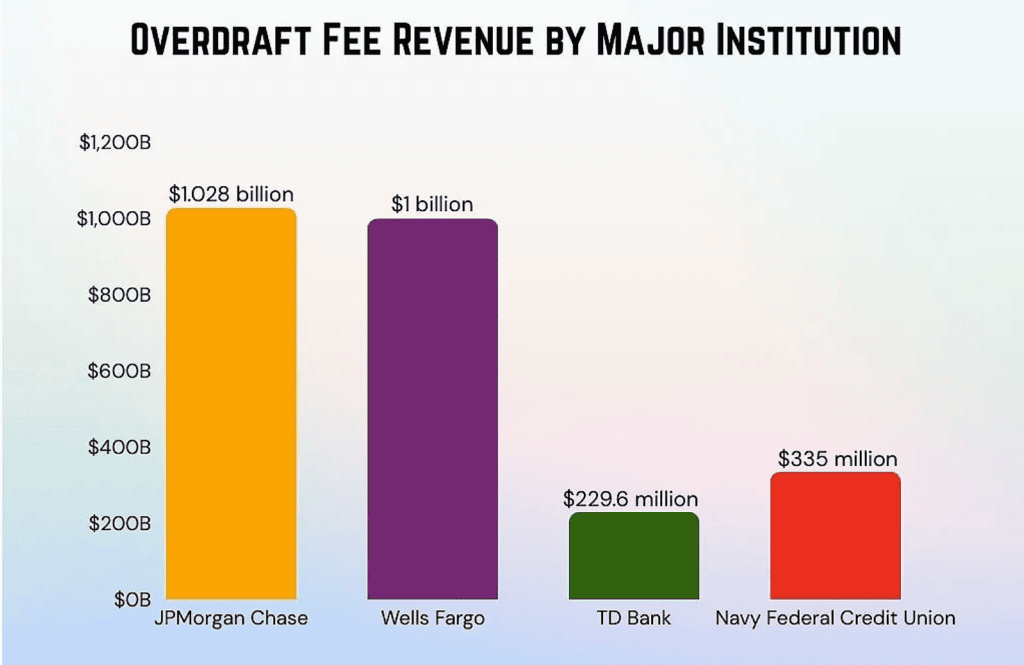

Even after that drop, overdraft fees remain a meaningful revenue source. In 2023, JPMorgan Chase reported just over $1 billion in overdraft revenue, followed closely by Wells Fargo at just under $1 billion, according to public disclosures and analysis from the National Consumer Law Center. Navy Federal Credit Union generated roughly $330–340 million, despite serving fewer members than the largest banks, resulting in higher overdraft revenue per account than many national institutions.

Source: CoinLaw

The average overdraft fee now ranges from about $27 to $35, down from pre-2020 levels. Many banks have reduced fees, eliminated NSF charges, or introduced grace periods and low-balance thresholds. A small number, including Capital One and Citibank, have eliminated overdraft fees entirely, though these remain exceptions rather than the industry norm.

The Market-Driven Changes Continue

Even without federal mandates, the overdraft landscape continues to evolve. Competitive pressure from online banks and fintech companies, many of which charge no overdraft fees, has pushed traditional banks to reform their practices. At least 12 major U.S. banks now offer checking accounts with no overdraft fees, and more than 60% of fintech-style banks waive overdraft charges entirely or substantially reduce them through fee-free buffers or low-cost alternatives.

Source: CoinLaw

The reforms vary widely. Some banks cap the number of overdraft fees charged per day, others require a minimum negative balance before a fee is triggered, and many now provide low-balance alerts or grace periods that allow customers to avoid fees if the account is quickly restored to a positive balance. Together, these changes have contributed to a meaningful reduction in consumer overdraft costs without eliminating overdraft services altogether.

For consumers who rely on overdraft protection as an occasional safety net, the service remains available at most institutions. However, the repeal of the CFPB’s proposed overdraft rule means these fees will continue to be determined by market competition and individual bank policies rather than federal caps. Whether this represents a preservation of consumer choice or a missed opportunity for regulatory protection depends largely on perspective, and on how frequently overdraft fees are incurred.

What This Means for Your Bank Account

With the federal rule off the table, consumers need to be more strategic about overdraft protection. The first step is understanding your bank’s current fee structure and the alternatives it offers. Many institutions now provide options such as overdraft lines of credit, account linking to savings accounts, grace periods, or low-balance alerts that can reduce or eliminate traditional overdraft fees.

It’s also worth evaluating whether you need overdraft coverage at all. Under federal regulations, banks must obtain affirmative consent before charging overdraft fees on ATM withdrawals and one-time debit card transactions. Consumers can opt out of this coverage without closing their accounts, though checks, ACH payments, and recurring debit transactions may still trigger overdraft fees if they exceed the available balance.

For customers who frequently overdraw their accounts, comparison shopping has become increasingly worthwhile. Online banks and many credit unions tend to offer lower fees, fee-free overdraft cushions, or no overdraft fees at all. While the market has not eliminated overdraft costs uniformly, competitive pressure has expanded consumer choice significantly compared with a decade ago, creating alternatives that may persist regardless of future regulatory action.

This topic is part of the broader banking system. For a complete explanation of accounts, transfers, fees, and consumer protections, see our Banking & Cash Management guide.