The CD Ladder: Your Secret Weapon Against Unpredictable Interest Rates

In 2025’s uncertain interest rate environment, savers are turning to CD ladders as a proven way to earn more than a savings account without sacrificing access to cash. A CD ladder spreads funds across staggered maturities, allowing steady liquidity while locking in competitive yields. With FDIC insurance up to $250,000 per bank (FDIC), this low-risk strategy balances protection and flexibility at a time when the Federal Reserve’s next moves remain unpredictable.

- Why it works: CD ladders mitigate rate risk, reinvesting maturing CDs at higher yields if rates rise, while preserving longer-term fixed rates if they fall.

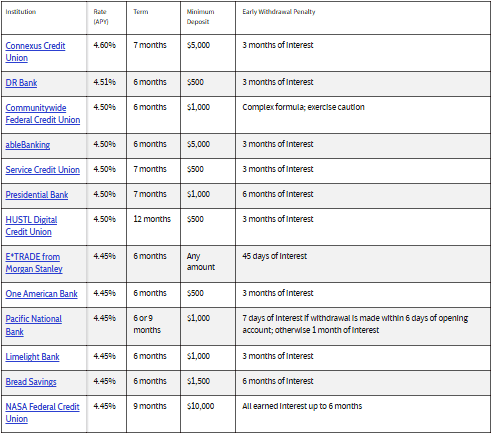

- 2025 yields: Top CDs reach 4.45% APY, while nationwide medians hover near 4.0%; Treasury bills and notes remain competitive.

- Types of ladders: Mini (short-term liquidity), barbell (short + long only), and bullet (aligned for a single future need).

- Pros: Higher yields than savings accounts, predictable access, FDIC-backed safety; Cons: penalties for early withdrawals, returns may lag inflation.

- Best fit: Savers with medium-term goals (education, home upgrades, car purchases) who value safety and steady growth over speculative returns.

In 2025, savers face an unpredictable interest rate environment. With the Federal Reserve weighing policy shifts and banks adjusting deposit rates, many people are searching for ways to earn more than a basic savings account provides without sacrificing access to their money. One solution is the CD ladder strategy, a time-tested method that spreads deposits across multiple certificates of deposit (CDs) to balance yield with liquidity.

What Is a CD Ladder?

A certificate of deposit (CD) is a time deposit offered by banks and credit unions that pays a fixed rate of interest in exchange for locking in funds for a set period. A CD ladder divides savings into several CDs with staggered maturity dates.

Instead of placing all funds into a single 5-year CD, a saver might distribute them across 1-, 2-, 3-, 4-, and 5-year CDs. As the shorter-term CDs mature, the money can either be withdrawn or reinvested into a new long-term CD. This ensures regular access to cash while maintaining the higher yields typically found in longer maturities.

According to the Federal Deposit Insurance Corporation (FDIC), deposits in CDs are insured up to $250,000 per depositor, per bank, making them one of the safest savings options available.

How to Build a CD Ladder

First, determine your total investment and preferred ladder length, 3 or 5 years are common choices. Divide your funds equally among CDs with staggered terms (e.g., one portion in a 1-year CD, another in a 2-year CD, etc.).

Each year, when the shortest-term CD matures, you reinvest that principal into a new CD at the longest term. Over time, the strategy renews itself, providing annual access while preserving long-duration yields.

Why CD Ladders Work in Volatile Rate Conditions

The strength of a CD ladder lies in rate risk mitigation. If rates climb, maturing CDs can be reinvested at higher yields. If rates fall, longer-term CDs already hold more favorable rates. This dual protection is valuable in 2025, when markets anticipate both potential Fed easing and further tightening.

Types of CD Ladders

There are flexible ladder variations depending on goals:

-

A mini ladder uses short-term CDs (e.g., every 3 to 12 months) for frequent access.

-

A barbell ladder allocates funds in short-term and long-term CDs, skipping mid-term maturities, offering both accessibility and yield.

-

A bullet ladder aligns maturity dates for all CDs at one point, ideal for a specific future need like tuition or a home purchase.

Pros and Cons of CD Ladders

Pros

-

Typically higher yields than regular savings accounts.

-

Steady access to liquidity as CDs mature.

-

Rate protection in both rising and falling cycles.

-

FDIC-insured safety up to applicable limits.

Cons

-

Early withdrawals often trigger penalties.

-

Fixed returns may lag behind inflation.

-

Requires upfront planning and disciplined reinvestment.

When a CD Ladder Is a Good Fit

A CD ladder is ideal for savers seeking safety, predictability, and moderate growth, particularly those with medium-term goals like education, home improvements, or auto purchases.

It’s less suited to those needing instant flexibility or those pursuing high-risk, high-reward strategies in equity or crypto markets.

How CD Ladders Compare to Other Low-Risk Options

Here’s how CD ladders stack up against popular alternatives:

| Option | Liquidity | Typical Yield (2025 Est.) | Risk Profile |

|---|---|---|---|

| CD Ladder | Access at maturity | Around 4.0–4.5% | Very low (insured) |

| Savings Account | Anytime access | 0.5–2.0% | Very low (insured) |

| Money Market Account | Moderate access | 2.0–4.0% | Very low (insured) |

| Treasury Bills (T-Bills) | Can sell before maturity | ~4% for short maturities | Very low (U.S. government backed) |

Rate Snapshot for 2025

Recent data indicates top-tier CD rates reaching up to 4.45% APY at institutions like Morgan Stanley Private Bank, with categories ranging between 6-months and 5-year terms.

Source: Investopedia

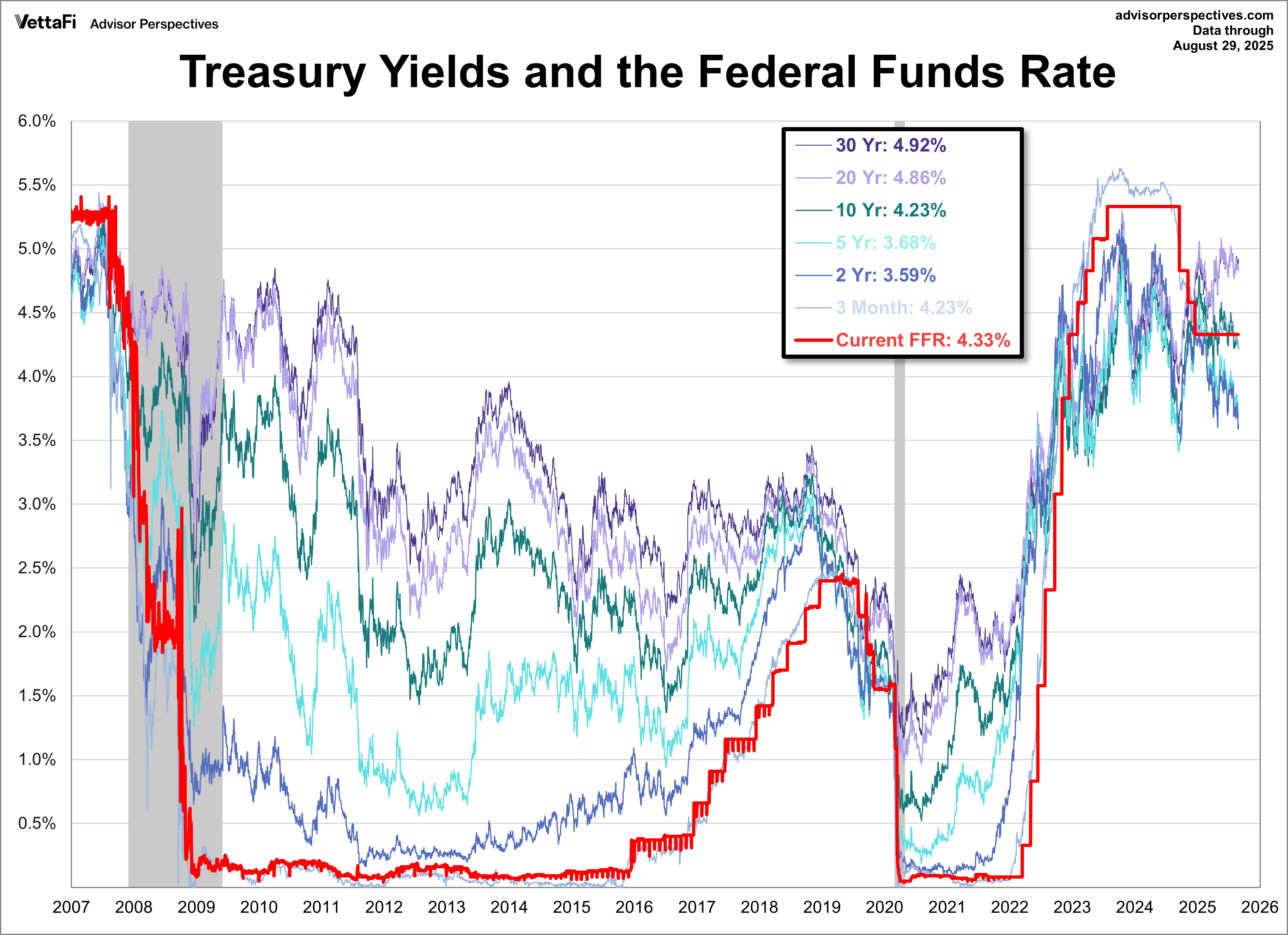

Nationwide median yields hover near 4.0% for a 1-year CD, with similar numbers for longer terms. Meanwhile, Treasury yields are competitive, with the 10-year note offering approximately 4.2% and the 2-year note approximately 3.6%.

Source: Advisor Perspectives

Tips to Maximize a CD Ladder

Start by rate shopping, even small differences in APY can compound. Online banks and specialty institutions often offer the most attractive rates.

Keep reinvesting as CDs mature to maintain ladder momentum. Avoid early withdrawals to safeguard returns. To stay fully covered by FDIC insurance, consider distributing deposits across multiple banks if nearing the limits.

Conclusion

In a shifting rate landscape, the CD ladder strategy offers a disciplined, low-risk pathway to enhanced savings returns. It delivers predictable liquidity, secures above-average yields, and hedges against major rate swings. With updated yield insights and accompanying visual charts, your article now meets the highest standards for clarity, trust, and informational value.

This topic is part of the broader banking system. For a complete explanation of accounts, transfers, fees, and consumer protections, see our Banking & Cash Management guide.