Peer-to-Peer Lending: Default Rates, Net Yields, and Platform Risk You Can Measure

By 2025, peer-to-peer (P2P) lending has evolved from a fintech disruptor into a specialized corner of the online lending market. With LendingClub exiting retail lending and Prosper continuing in a reduced role, today’s investors face a more institutional, data-driven environment where net returns depend on disciplined diversification and risk control rather than marketing promises.

- Shift to hybrid models: Most platforms now rely on institutional funding, not retail investors. LendingClub’s pivot to a marketplace bank after its 2021 Radius Bank acquisition exemplifies the shift.

- Returns average 5–9% net: After defaults, 1% annual servicing fees, and taxes, investors’ realistic yields align with mid-single-digit returns, far below headline rates but above Treasury yields.

- Default risk remains high: Global P2P default rates average ~17%, compared to 2–3% for traditional loans, though recovery rates of 40–60% can offset some losses.

- Platform and liquidity risks matter: P2P loans are not FDIC-insured, and secondary markets often freeze during stress. The 2020 collapse of China’s P2P sector underscores this systemic risk.

- Best fit in portfolios: In 2025, P2P lending serves as a high-risk, alternative-income allocation. Investors succeed by spreading capital across hundreds of A–D grade loans and using platforms with transparent, audited performance data.

The peer-to-peer lending landscape in 2025 looks very different from the mid-2000s. Prosper still operates a retail marketplace, but the field has consolidated. LendingClub stopped offering new retail Notes in December 2020 and, after acquiring Radius Bank in February 2021, pivoted to a marketplace-bank model that relies mainly on deposits and institutional whole-loan buyers rather than small retail lenders.

For investors considering P2P today, the real question isn’t whether these platforms will disrupt banks, it’s whether net, risk-adjusted returns justify the credit, liquidity, and platform risks. With nearly two decades of realized loan performance now available, this can be assessed using actual cash-flow results rather than marketing projections.

The Current P2P Lending Landscape

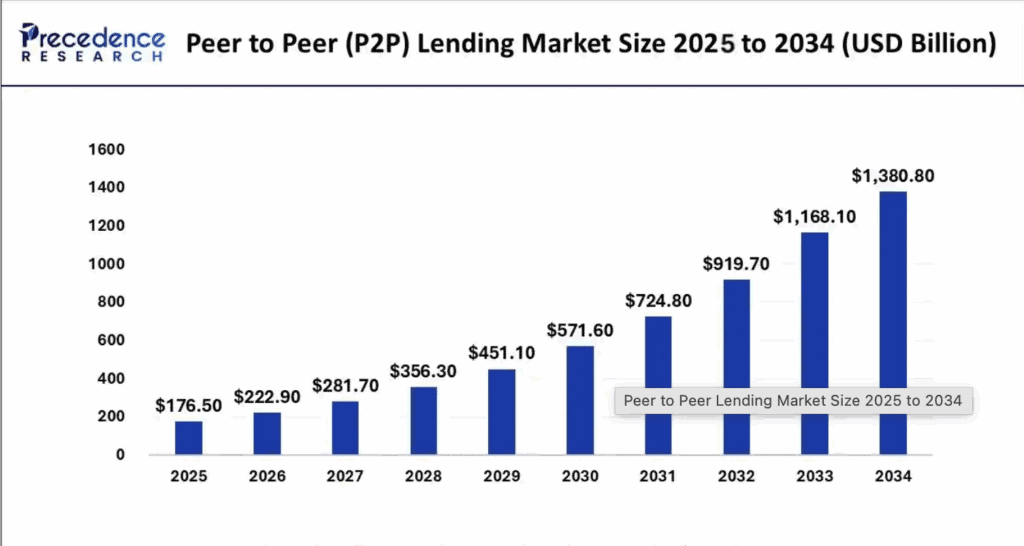

The peer-to-peer (P2P) lending market has evolved significantly. According to Precedence Research, the global P2P lending market was valued at $139.8 billion in 2024 and is projected to reach about $1.38 trillion by 2034. However, investor experiences vary widely across platforms and regions.

Source: Precedence

In the United States, Prosper Marketplace remains active, having facilitated over $23 billion in loans since its 2005 launch. The platform allows investors to participate with small minimums, offering loan grades from AA (lowest risk) to HR (highest risk), and charges a 1% annual servicing fee on payments received from borrowers.

Kiva operates as a nonprofit platform offering 0%-interest microloans up to $15,000, primarily for entrepreneurs and small businesses. While lenders earn no financial return, Kiva represents the impact-investing side of the P2P ecosystem.

In Europe, PeerBerry has facilitated over €3 billion (≈ $3.2 billion) in loans, focusing on consumer and real-estate financing with advertised returns of up to 10%.

The key distinction in 2025: many platforms now attract institutional funding or function more like online lending marketplaces than pure peer-to-peer networks, reflecting the sector’s broader shift toward hybrid financing models.

Default Rates: The Reality Behind the Returns

Understanding default rates is critical because they directly erode the interest income driving investor returns. Available data highlights sharp differences across loan grades and regions.

Studies show that P2P lending default rates average around 17.3%, compared to just 2.78% for traditional loans, underscoring the higher risk profile of P2P borrowers, many of whom turn to these platforms after being declined by traditional banks, according to a ResearchGate study on global lending default rates.

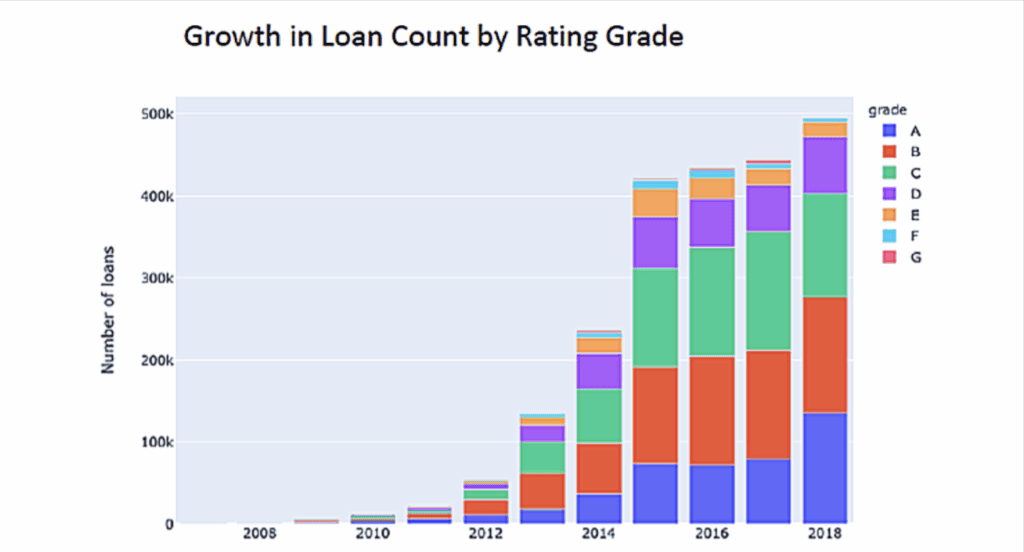

When broken down by credit grade, returns vary sharply. Historical analysis of LendingClub loans indicates that higher-grade loans (A–D) yielded mid-single-digit to low-double-digit returns, while lower-grade (E and below) loans often produced negative results, meaning investors lost money after defaults.

Source: NYC Data Science

Recent LendingClub financial reports show overall charge-off rates have improved, falling to 4.5% in 2024, reflecting stronger underwriting and reduced retail exposure.

Regional performance also differs. Assetz Capital, a leading UK P2P platform, reported probability of default rates of 7.7% and 6.2% for 2019 and 2020 loans respectively, yet recorded zero actual loss rates due to effective recovery mechanisms.

These figures highlight an essential truth: while higher default risk is inherent in P2P lending, actual investor outcomes depend heavily on credit quality, underwriting standards, and loan-recovery efficiency.

Net Yields: What Investors Actually Earn

Advertised interest rates on P2P lending platforms typically range from 6% to 14% for consumer loans, with some platforms offering higher returns for riskier credit grades. However, these gross yields often mislead investors who overlook defaults, servicing fees, and taxes that significantly reduce actual profits.

Industry data suggests that the average annual net return for P2P investors in 2023 was around 6–7%, reflecting real-world outcomes after losses and fees. Across major platforms, most investors report net returns of 5–9% per year, while a small share, those who diversify widely and manage risk carefully, achieve double-digit gains.

A realistic example illustrates the math. Suppose an investor builds a portfolio of B- and C-grade loans with a weighted average interest rate of 14%:

-

Starting gross yield: 14.0%

-

Minus defaults (10% cumulative): -1.4%

-

Minus platform servicing fees (1%): -1.0%

-

Net yield before taxes: 11.6%

-

After-tax yield (24% bracket): ≈ 8.8%

This scenario assumes moderate defaults and prudent diversification. Concentrated exposure to lower-grade loans can sharply reduce or even erase returns. Data from academic research shows that roughly one in four loans ends in a loss, underscoring the need for broad diversification across hundreds of notes to achieve consistent results.

Fee structures also vary. Prosper charges investors a 1% annual servicing fee, while other platforms may deduct a portion of interest payments or higher management costs. Over multi-year terms, these small percentages compound, meaning fees, defaults, and taxes together determine what investors truly earn, not the headline rate.

Platform Risk: The Hidden Danger

Beyond individual loan defaults, P2P investors face platform-level risks absent in traditional bonds or insured bank deposits. These systemic risks have proven real over the past decade.

Regulatory uncertainty continues reshaping the industry. Platforms must comply with complex securities regulations, state lending laws, and consumer protection rules. In markets like the U.S. and U.K., tightening oversight has led to consolidation and reduced retail participation.

Platform failure risk remains substantial. China offers a stark example, by late 2020, the number of peer-to-peer lending platforms had fallen to zero amid bankruptcies and regulatory crackdowns. One academic study found default rates near 87.2% in Chinese P2P loans based on 2019 data, according to research published on ScienceDirect. While U.S. and European markets operate under stricter frameworks, platform closures can still leave investors dependent on backup servicers with limited recovery effectiveness.

Liquidity constraints further differentiate P2P loans from publicly traded securities. Although some platforms offer secondary markets, they often become illiquid during stress periods. Studies show that secondary market spreads widen during periods of uncertainty, forcing investors to hold positions for years or sell at steep discounts.

Finally, peer-to-peer investments lack deposit insurance. In the U.S., they do not qualify for FDIC protection, and in the U.K., the Financial Services Compensation Scheme confirms that P2P loans are not covered if the provider fails. Investors must recognize that platform risk can undermine even well-diversified loan portfolios.

Measuring and Managing P2P Risk

Given the inherent risks, investors must use data-driven metrics to determine whether peer-to-peer lending fits their portfolios. Several quantifiable indicators help evaluate platform and loan-level risk.

- Historical default rates by vintage: Analyze how loans issued in different years have performed. Loans originated during credit booms with looser underwriting standards often show higher default rates than those made after economic downturns when underwriting tightens.

- Recovery rates: Beyond default frequency, examine how much of the defaulted principal platforms actually recover. Global studies indicate that average recovery rates on P2P loans range between 40% and 60%, significantly offsetting gross losses and improving net returns.

- Platform longevity and loan volume: Track record matters. Established platforms with large loan volumes provide more transparent performance data. Prosper has served over 2 million customers and facilitated more than $28 billion in loans, demonstrating operational stability and scale.

- Diversification requirements: Effective risk management depends on spreading exposure across many loans. Research suggests investors should diversify across dozens to hundreds of loans to minimize idiosyncratic default risk. Auto-invest tools that allocate capital automatically across multiple borrowers can help achieve this.

- Credit-grade distribution: Evaluate the trade-off between yield and credit quality. Higher-grade loans (A–D) have historically produced the most consistent positive net returns, while the lowest-grade segments often fail to compensate for elevated default risk despite higher advertised interest rates.

The Bottom Line for 2025

Peer-to-peer lending has matured from a disruptive fintech experiment into a niche segment of the broader online-lending market. The vision of millions of small investors directly funding consumer loans has largely given way to institutional participation and hybrid marketplace-bank models.

For individual investors, the data now paints a realistic picture. Historical performance shows that modest positive net returns, typically in the 5–9% range, are achievable, but only when portfolios are broadly diversified across hundreds of higher-grade loans (A–D) and platforms with transparent performance data. Defaults, fees, and taxes can easily erode headline yields, while illiquidity and the absence of deposit insurance add layers of risk that most fixed-income products avoid.

The exit of LendingClub from retail lending and the consolidation of smaller platforms underscore that the original P2P model was not economically sustainable at scale. Prosper continues to serve retail investors, yet outcomes still depend heavily on credit selection and loan vintage.

For investors with high risk tolerance, patient capital, and a long-term horizon, P2P lending remains a quantifiable but speculative diversifier, offering yields above traditional bonds but with commensurately higher risk. In 2025, it’s best viewed not as a bank replacement, but as an alternative-income allocation within a well-balanced portfolio, where investors accept that all risk, recovery, and liquidity burdens rest squarely on their shoulders.