MicroStrategy’s Bitcoin Bet: What Happens When the Music Stops?

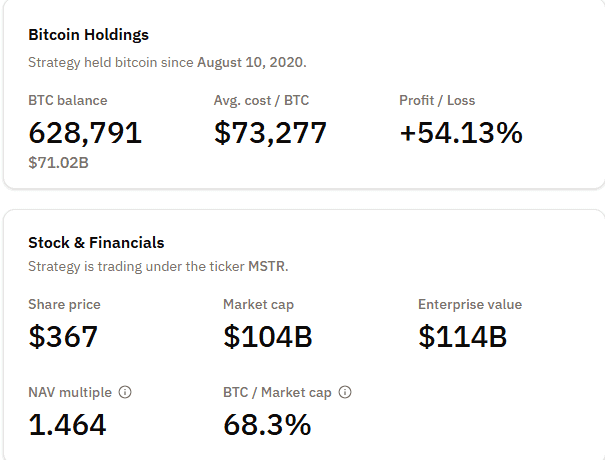

Strategy (formerly MicroStrategy) has transformed into the world’s most aggressive corporate Bitcoin buyer, holding over 628,791 BTC worth more than $70 billion as of Q2 2025. The company’s record $10 billion quarterly profit came almost entirely from Bitcoin price appreciation, not from its core enterprise software business, which generated just $114.5 million in revenue. Investors should understand that owning $MSTR stock is effectively owning a highly leveraged, riskier version of Bitcoin itself.

- Extreme concentration risk: Strategy holds 3% of all Bitcoin in circulation, far more than Tesla (11,509 BTC) or Marathon Digital (49,940 BTC), leaving it uniquely exposed to volatility.

- Volatility drives earnings: In Q1 2025, BTC losses triggered a $4.22B net loss; in Q2, a rebound produced a $10B profit.

- Leverage is rising: Strategy raised $2.5B in preferred equity to buy Bitcoin at $117K per coin, but faces restrictions on issuing common stock, reducing flexibility.

- Stock is riskier than BTC: MSTR fell 40% in July 2025 while Bitcoin stayed flat, showing how dilution and leverage amplify swings.

- Bottom line for investors: Strategy is effectively a Bitcoin ETF on steroids. Massive upside exists if BTC keeps rising, but history shows Bitcoin corrections of 70–90%, and with Strategy’s leverage, losses could be even harsher.

MicroStrategy, now rebranded as Strategy, has become the most aggressive corporate Bitcoin buyer in history. With 628,791 BTC on its balance sheet, the company has successfully rebranded itself from a software firm into a publicly traded Bitcoin proxy.

In Q2 2025, it posted a record $10 billion in net income, largely from Bitcoin price appreciation. While that may sound like a win, the company’s financial strategy is built on a narrow, high-risk foundation.

Its core business, enterprise software, generated only $114.5 million in quarterly revenue, a drop in the ocean compared to its $70+ billion market cap. As Bitcoin’s price rises, so does Strategy’s fortune. But history shows us that Bitcoin doesn’t rise forever. The question isn’t whether another sharp correction will come, it’s how severely it will test Strategy’s leverage-fueled model when it does.

This article explores the deeper financial mechanics, strategic vulnerabilities, and market risks that investors need to understand before betting on $MSTR.

The Illusion of Diversified Success

In Q1 2025, Strategy recorded a $5.91 billion unrealized loss on its digital assets. This was due to a temporary decline in Bitcoin’s market price under the new fair-value accounting rules. The company reported a net loss of $4.22 billion, or $16.49 per share, even though the software segment remained stable.

Yet just a quarter later, in Q2 2025, those same Bitcoin holdings delivered an unrealized gain of $14 billion, swinging the company to a $10 billion profit. This isn’t a normal earnings trajectory, it’s speculative exposure masked as operational success.

Despite the volatility, Strategy’s market cap ballooned to over $70 billion, even though total revenue for the quarter barely crossed $114 million. For comparison, Airbnb earned $10 billion in 2023 and holds a similar valuation, despite offering a far more diverse revenue stream.

Source: Yahoo Finance

The Dangerous Math of Extreme Concentration

As of July 2025, Strategy holds 628,791 BTC, acquired at a total cost of $46.07 billion, with an average purchase price of $73,277 per Bitcoin. That amount represents roughly 3% of all BTC in circulation.

Source: BitcoinTreasuries.net

By comparison, Marathon Digital Holdings holds just 49,940 BTC, and Tesla has 11,509 BTC, less than 2% of Strategy’s stash.

No other public company, especially one outside the crypto mining industry, has taken on such concentrated exposure to a single volatile asset. This is not strategic diversification; it’s asset singularity. In traditional corporate finance, this would be considered reckless.

Bitcoin’s Brutal Track Record

Bitcoin is known for its explosive gains, but also for its devastating losses. Historical data reveals:

-

In 2018, BTC ended the year at $3,709, down 73% from the start.

-

From November 2021 to November 2022, Bitcoin crashed nearly 78%, from $69,000 to $15,476.

-

The worst drawdown occurred in 2011, when Bitcoin plunged 93.2%, and recovery took over a year.

Even during uptrends, drawdowns of 10–30% are common. For Strategy, every sharp correction puts billions in unrealized losses on the books and shakes investor confidence.

Surviving the 2022 Crypto Winter

The last crypto winter in 2022 tested Strategy’s business model. When Bitcoin collapsed to around $15,000, credit markets tightened. According to CCN, the company paused its Bitcoin acquisitions and struggled to raise new capital, relying instead on internal cash flow and asset-backed financing.

This period exposed the risk of Strategy’s heavy dependence on external capital to fund BTC buys. When lenders pulled back, so did Strategy’s buying spree.

Strategy chairman Michael Saylor tweets on August 4th 2025 that the Bitcoin price is not going down again. Because if it did… well that would be a problem. Source: Michael Saylor on X

Leveraging Into the Storm

In 2025, however, Strategy is doubling down. The company raised $2.5 billion through preferred equity to acquire 21,021 BTC at ~$117,000 each, as reported by Barron’s.

But there’s a catch. Barron’s reports that the company can no longer issue common stock unless its BTC-to-equity ratio exceeds 2.5x. Currently sitting at 1.7x, that restriction forces Strategy to rely on costlier instruments like preferred stock or convertible notes, further tightening its financial flexibility.

This rising leverage amplifies returns during bull runs but magnifies losses during downturns, a risky position, especially with Bitcoin at historically high levels.

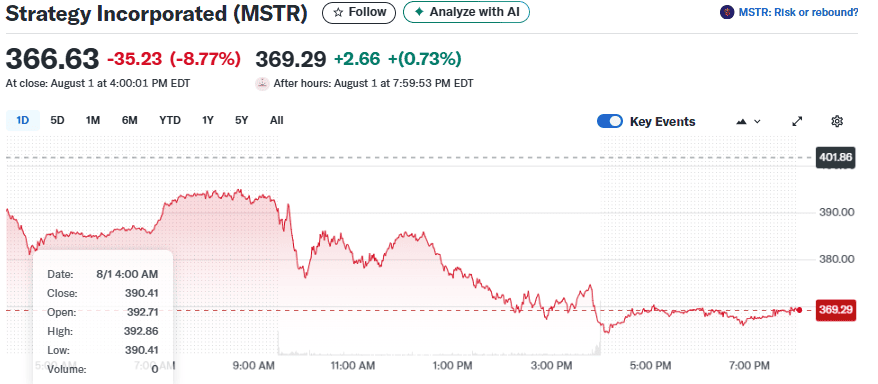

Stock Volatility Tells the Real Story

For investors, Strategy’s stock has become a leveraged proxy for Bitcoin – with a catch. In July 2025, MSTR fell 40%, even as Bitcoin traded sideways, revealing the compounding effects of financial leverage.

Source: Yahoo Finance

Valuation premiums also fluctuate wildly. In late 2024, MSTR traded at a 300% premium to net asset value. But in mid-2022, it had plunged to a 50% discount, driven by panic and liquidity fears.

For long-term holders, the stock’s volatility can often be more punishing than holding BTC directly.

The Dilution Dilemma

Critics argue that Strategy’s strategy requires Bitcoin to consistently outperform its own stock, as each round of equity issuance dilutes shareholder value. If BTC stagnates or drops, dilution erodes investor returns, and the business model could eventually collapse.

This creates a vicious cycle: the company must issue new shares to buy BTC, which hurts share value, increasing pressure on BTC performance to offset dilution.

Bottom Line: Built for Boom or Bound to Bust?

Strategy is no longer a software company in the traditional sense, it’s a high-risk, high-leverage macro bet on Bitcoin. In 2024, that bet paid off handsomely with 370% gains in MSTR stock. But Bitcoin’s long history of brutal drawdowns, paired with Strategy’s extreme leverage, makes for a dangerous formula.

Investors must ask themselves:

Do I believe in Bitcoin enough to invest in a company that behaves like a Bitcoin ETF—on steroids?

If the answer is yes, Strategy offers massive upside. But when the music stops it’s clear that many investors won’t find a chair.