How Retirees Can Unlock Home Equity: Beyond the Traditional Reverse Mortgage

In 2025, older homeowners have more ways than ever to unlock housing wealth beyond traditional reverse mortgages. While the FHA’s Home Equity Conversion Mortgage (HECM) limit rose to $1,209,750, new products like home-equity investments and sale-leaseback programs are reshaping how retirees convert home value into cash without monthly payments or new debt. Each offers trade-offs between liquidity, long-term cost, and future appreciation. Here’s what to know:

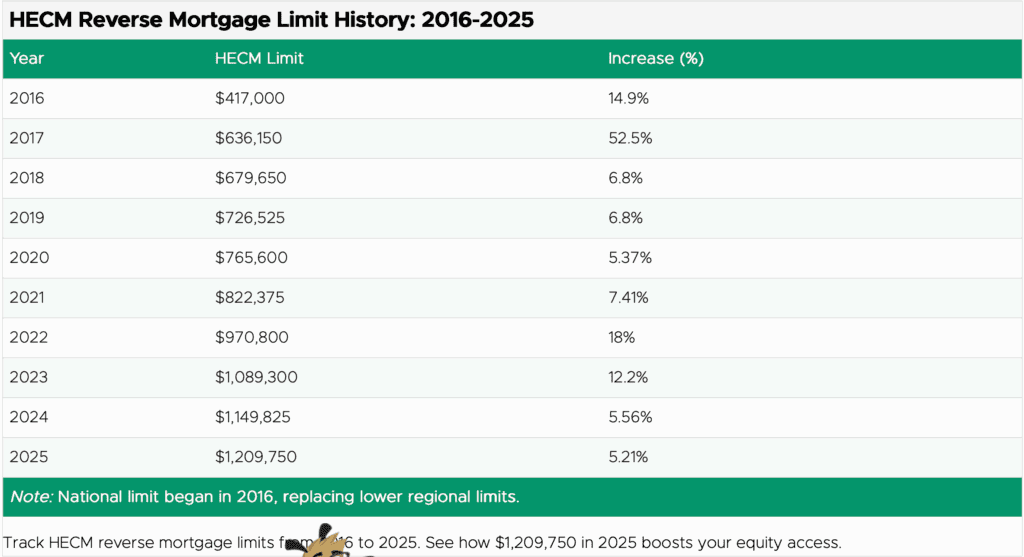

- Reverse mortgage update: The 2025 HECM lending cap increased to HUD’s $1,209,750, letting retirees access more equity as interest rates ease. But taxes, insurance, and upkeep remain required to avoid foreclosure.

- Home equity investments (HEIs): Firms like Hometap, Point, and Unison offer cash upfront in exchange for a share of future appreciation—no monthly payments, but effective long-term costs can approach 20%.

- Bonus Homes model: Converts a property into a managed rental, covering repairs and operations while homeowners retain ~33% of future appreciation, a hybrid between ownership and sale.

- Trade-offs: New models eliminate debt but exchange future gains for liquidity. Fees (≈4–5%) and eligibility limits apply; repayment usually occurs at sale or after 10–30 years.

- Retirement planning insight: With reverse mortgages, HEIs, and sale-leaseback options expanding, retirees should compare scenarios, especially if legacy goals or relocation plans are factors, before choosing how to tap equity.

New financial tools are transforming how older Americans unlock their home equity in 2025. For decades, reverse mortgages, especially the FHA-insured Home Equity Conversion Mortgage (HECM), have helped retirees convert home value into cash without monthly payments. Today, that once-niche product is evolving alongside a new generation of options, including home-equity sharing agreements, sale-leaseback programs, and jumbo reverse mortgages designed for higher-value homes. Together, these innovations are expanding how homeowners access housing wealth, offering flexible ways to boost retirement income while remaining in their homes.

The Reverse Mortgage Renaissance

Reverse mortgages, especially the government-backed Home Equity Conversion Mortgage (HECM), have evolved significantly in 2025. The lending limit increased to $1,209,750, roughly $60,000 higher than in 2024, according to the U.S. Department of Housing and Urban Development (HUD). The industry continues to expand, with major lenders forming partnerships with traditional mortgage companies and integrating forward and reverse products to reach more homeowners.

Source: All Reserve

While no sweeping new federal rules have been issued, lenders are emphasizing enhanced loss-mitigation options and repayment plans to help borrowers stay current on property taxes and insurance, key factors that can trigger foreclosure. Lower interest rates are also improving borrower terms, allowing some to access a larger share of home equity as the Federal Reserve eases policy in 2025.

Still, the fundamentals remain the same. Major banks like Bank of America and Wells Fargo exited the reverse-mortgage business years ago and remain absent from the market. The products themselves remain complex, carrying high upfront costs, accruing interest, and a continued risk of foreclosure if homeowners fail to maintain taxes, insurance, or property upkeep.

The New Guard: Home Equity Investments

The most significant innovation in home-equity finance isn’t a tweak of reverse mortgages, it’s a new model called Home Equity Investments (HEIs) or Home Equity Agreements.

Companies like Point, Hometap, Unlock, Unison, and Splitero allow homeowners to receive a lump sum of cash in exchange for a share of their home’s future value, no monthly payments, no traditional interest, and often more flexible credit requirements.

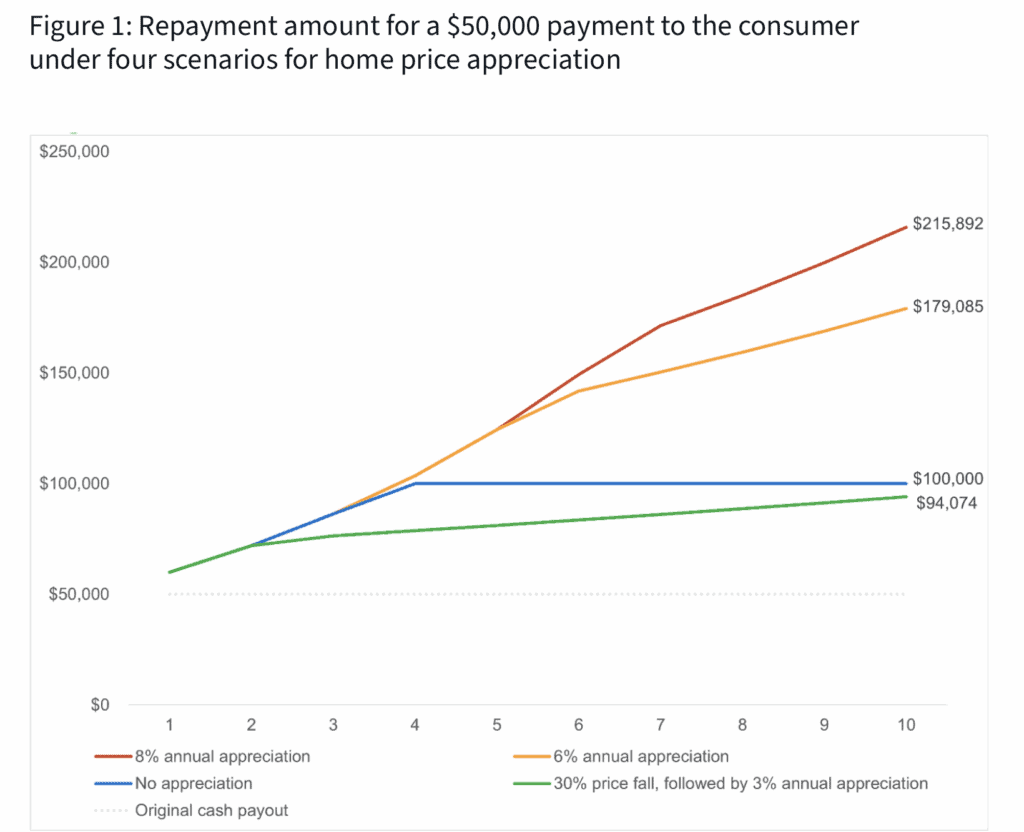

Here’s how it works: a homeowner can access roughly 10–30% of their home’s value upfront and agree to repay the original amount plus a portion of any future appreciation when they sell the home or the agreement term ends, typically 10–30 years later. These agreements are structured as equity investments rather than loans, meaning the investor shares in both appreciation and, in some cases, depreciation.

Point offers investments from $25,000 to $500,000 with terms up to 30 years. Hometap provides up to $600,000 with a standard 10-year term. Unlock requires at least 20% home equity and offers some of the fastest funding timelines in the sector.

Source: CFBP

While appealing for those seeking cash without new debt, the Consumer Financial Protection Bureau warns that these contracts can carry steep long-term costs. Because repayment depends on home appreciation, investors’ returns can translate into effective annual rates near 20%, making HEIs best suited for homeowners who understand the trade-off between immediate liquidity and future equity loss.

The Most Innovative Play: Bonus Homes

One of the most forward-thinking home-equity models comes from Bonus Homes, which enables homeowners to unlock all their available equity, essentially as if they sold the home, without taking on debt or monthly payments.

Through its Home Appreciation Partnership program, the company converts the property into a managed rental, covering maintenance, repairs, and tenant operations, while the homeowner retains up to about one-third (≈ 33 %) of any future appreciation. Participants also benefit from flexible move-out timing, typically after a minimum five-year hold period, allowing them to capture future market gains without the burdens of ongoing ownership.

Independent analysis from the Economic Architecture Project highlights Bonus Homes as a new wealth-building alternative for middle-class homeowners, while Inman News describes it as a “don’t-sell solution” that bridges the gap between ownership and liquidity.

The Trade-offs

These new products address many of the reverse mortgage market’s biggest drawbacks, offering no monthly payments, no interest, and often no strict credit requirements. But they come with their own trade-offs.

You’re essentially exchanging future home appreciation for immediate cash access. If your home’s value rises substantially, you’ll owe far more than you received. Most home equity agreement contracts require repayment within 10–30 years, or when you sell, refinance, or buy out the investor. While these products avoid monthly debt accumulation, they’re still secured by your property. Origination and service fees can reach 4–5%, and eligibility is limited, homes must meet equity and valuation thresholds.

These agreements solve key pain points but shift risk toward the homeowner, a fair trade for liquidity, but one that demands careful long-term planning.

What This Means for Retirees

For a retired couple sitting on significant home equity, the landscape has shifted. Traditional reverse mortgages remain a viable option for those planning to stay in their homes long term and seeking predictable access to funds. With the 2025 HECM lending limit raised to $1,209,750 and lower interest rates improving borrowing power, qualified homeowners can now access a larger share of their equity.

Meanwhile, home equity investments (HEIs) appeal to retirees who prefer no monthly payments or traditional debt, especially those uncertain about how long they’ll stay put. These agreements provide cash upfront in exchange for a portion of future appreciation, offering flexibility but also reducing the potential inheritance for heirs.

The bottom line: after decades of limited options, retirees now have a genuine menu of choices for unlocking home wealth. Each approach carries trade-offs between immediate access, long-term costs, and future equity preservation. Financial advisors increasingly recommend comparing every option, including downsizing, before committing to any strategy.

This article is part of Mooloo’s Retirement & Long-Term Planning Hub, covering retirement income, Social Security decisions, investment risk, healthcare costs, and long-term financial security.