The Fastest Way to Pay Off Credit Card Debt: This 3-Step Method Could Cut Your Time in Half

With average credit card APRs now above 20% (Federal Reserve, 2025), carrying a balance is one of the most expensive ways to borrow. A $5,000 balance at 22% APR can take 15+ years to pay off with minimums—costing thousands in interest. The key to financial freedom is adopting a repayment strategy, automating payments to avoid penalties, and freeing up extra cash to accelerate progress.

- Pick a strategy: Use the avalanche (highest APR first) to save the most money, or the snowball (smallest balance first) for faster wins.

- Automate payments: Set up autopay for minimums to avoid late fees, and direct extra payments toward your target card.

- Increase cash flow: Cut $100–$200 from expenses or add side income to shave years off repayment.

- Stay debt-free: Build a $500–$1,000 emergency fund, track spending, and avoid new debt after payoff.

Bottom line: With rates at record highs, every extra payment counts. A smart plan combining strategy, consistency, and extra payments can cut your payoff time in half and save thousands in interest.

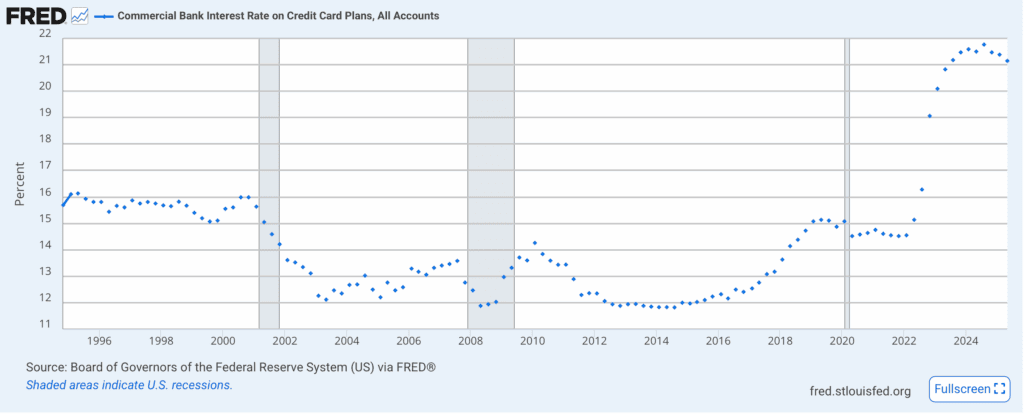

Credit card debt is one of the costliest types of borrowing. According to Federal Reserve data, the average annual percentage rate (APR) on credit cards in 2025 is now above 20%. That means carrying a balance is like paying a steep penalty every month.

Source: FRED

For example, if you owe $5,000 at 22% APR and pay only the minimum (about $125 per month), it could take more than 15 years to clear the debt and cost thousands of dollars in interest. The longer balances linger, the more money slips away in fees and finance charges. Paying off debt quickly isn’t just about peace of mind, it’s about protecting your financial future.

Step 1 — Choose a Repayment Strategy

For people with multiple credit cards, the first step is to adopt a structured repayment method. Two time-tested approaches dominate:

-

Debt Avalanche (highest interest first): This method targets the card with the highest APR. Make minimum payments on all cards, then put every extra dollar toward the most expensive debt. You’ll save the most on interest and usually get out of debt faster.

-

Debt Snowball (smallest balance first): This strategy starts with the smallest balance. Pay minimums on all cards, then focus extra money on wiping out the lowest balance before moving to the next. This method creates quick wins and strong momentum.

Both strategies work. If you’re motivated by fast psychological wins, the snowball may be better. If your goal is to save the maximum amount of money, the avalanche is more efficient.

Step 2 — Automate and Prioritize Payments

Automation is critical for staying consistent. Missing even a single payment can trigger late fees, often $30–$40, and may cause your interest rate to climb. To prevent this:

-

Set up automatic payments for at least the minimum balance on every card.

-

Direct scheduled extra payments to your “target card” under the avalanche or snowball plan.

-

If possible, split payments into two per month instead of one, which reduces your average daily balance and lowers interest charges.

This system ensures you never miss deadlines and keeps your payoff plan on track.

Step 3 — Free Up Cash to Pay More Each Month

The speed of your debt payoff depends on how much extra money you can allocate. Even modest increases make a huge difference.

Cutting costs: Review your budget for quick wins. Cancel unused subscriptions, cook at home more often, shop around for lower insurance rates, or replace costly outings with free alternatives. Saving even $100–$200 a month can shave years off your repayment timeline.

Boosting income: Additional income can be just as powerful as trimming expenses. Side hustles such as tutoring, delivery driving, freelancing, or selling unused items online can add hundreds each month. Even small windfalls, like cash-back rewards, should be directed to debt repayment instead of new spending.

Source: Nerdwallet

Example: Cutting Debt Time in Half

Let’s look at how these principles play out in practice. Suppose you owe $7,500 across three cards, with an average APR of 22%:

-

Minimum payments only: Paying around $142.93 per month would take over 15 years and cost $18,227.71 in interest.

-

Avalanche with $286.43/month: You’d be debt-free in under three years, saving roughly $2,811.42 in interest.

-

Avalanche with $389.09/month: You’d be debt-free in just two years, with $1,838.07 in interest paid.

This example shows that repayment isn’t only about willpower, it’s about strategy. A smart plan can save both time and money, drastically changing your financial future.

source: Bankrate

Staying Debt-Free After Payoff

Paying off credit card debt is a major achievement, but staying debt-free requires discipline. Experts recommend building a small emergency fund of $500–$1,000 so unexpected expenses don’t push you back onto credit cards. Tracking spending with a budgeting app or spreadsheet keeps you accountable, while avoiding new debt ensures long-term stability.

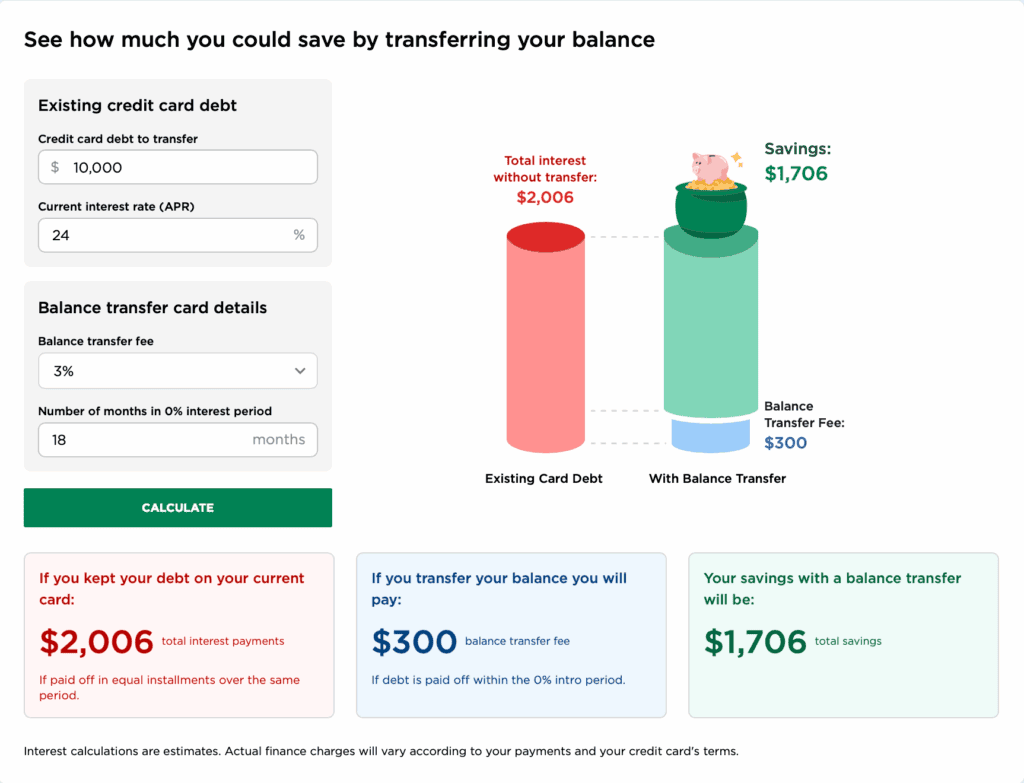

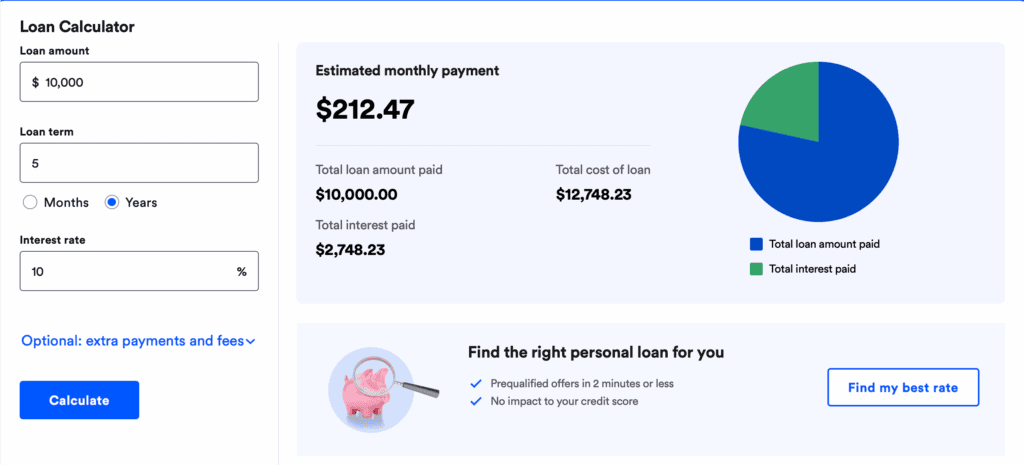

For some, a balance transfer card or debt consolidation loan can help reduce interest rates, provided you commit to not taking on additional debt.

Bottom Line

Credit card debt can feel like an unbreakable cycle, especially with today’s record-high interest rates. But by choosing a strategy that suits your mindset (avalanche or snowball), automating payments to protect against costly mistakes, and finding ways to free up cash for extra payments, you can cut your payoff time dramatically.

The formula is simple: strategy + consistency + extra payments = financial freedom. With discipline and a clear plan, it’s possible to save thousands in interest, cut your repayment time in half, and take control of your financial future.

Related: This topic is part of the broader credit system. For an overview of how credit scores, loans, and debt work together, see our Credit & Debt guide.