Federal vs. Private Student Loans: Why This Decision Could Cost You $50,000

The Numbers That Matter

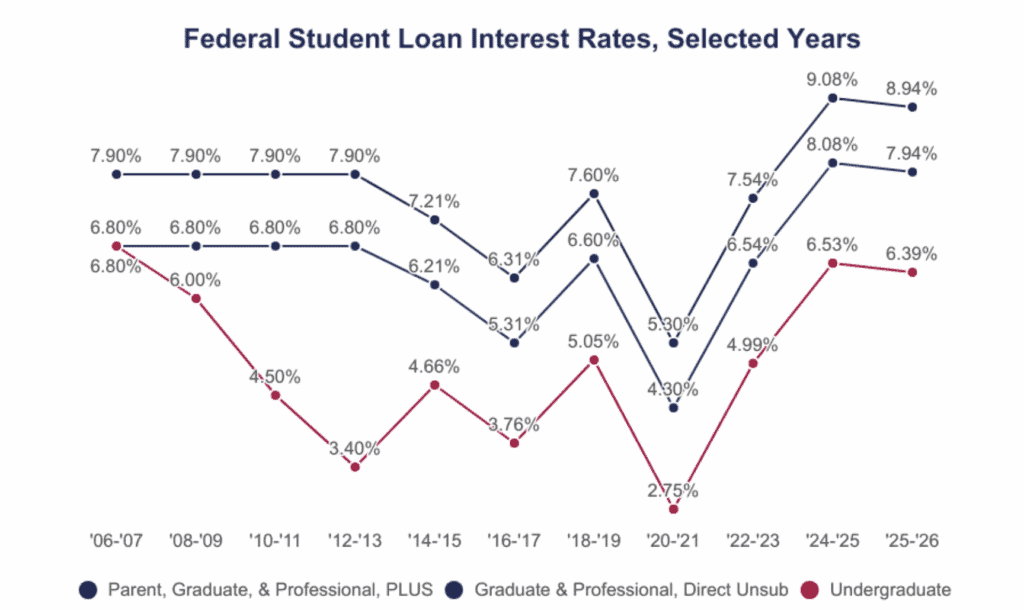

For the 2025–26 academic year, federal undergraduate loan rates are 6.39%, graduate students pay 7.94%, and parents taking out PLUS loans face 8.94%, according to the U.S. Department of Education. These rates apply uniformly, your credit score, income, and family wealth don’t affect the rate. However, PLUS loans require a credit check for adverse history, even though the rate itself is fixed.

Why Federal Loans Win for Most Borrowers

This is one of the biggest advantages of federal student loans. Whether you come from a wealthy family with perfect credit or you’re a first-generation student with no credit history, you’ll pay the same fixed interest rate for your loan type.

For the 2025-26 academic year, undergraduate Direct Subsidized and Unsubsidized Loans carry a 6.39% interest rate. Graduate students pay 7.94%, and parents taking out PLUS Loans face 8.94%. These rates apply equally to everyone, your credit score, income, or family wealth doesn’t affect them.

Private lenders, by contrast, set rates based on credit and perceived risk. Borrowers with weaker credit or no co-signer often face much higher rates, which disproportionately affects students from lower-income backgrounds.

Protections You Can’t Get Anywhere Else

Federal loans include built-in safety nets that can turn overwhelming debt into something manageable:

-

Income-Driven Repayment (IDR) plans cap your monthly payments at 10%–20% of your discretionary income, depending on the plan.

-

Public Service Loan Forgiveness (PSLF) cancels remaining balances after 10 years of qualifying public service.

-

Deferment and forbearance options let you pause payments during unemployment or financial hardship.

-

Death and disability discharge eliminates your debt if you die or become permanently disabled.

Private loans offer far fewer safeguards. Some lenders provide limited forbearance or hardship options, but they rarely match the flexibility and protections of federal programs.

No Credit Check (for Most Federal Loans)

Most federal loans, specifically Direct Subsidized and Unsubsidized Loans, require no credit check or co-signer. This makes them accessible to students just beginning their financial lives. However, PLUS Loans (for parents and graduate students) do require a credit check to ensure there’s no adverse credit history. Private student loans always involve a credit review, and most students need a creditworthy co-signer, usually a parent, to qualify for competitive rates.

The Federal Loan Coverage Gap

If federal loans are so superior, why does anyone take private loans? Simple: federal loans often don’t cover the full cost of attendance.

For dependent undergraduate students, annual federal loan limits range from $5,500 to $7,500 per year, with a lifetime cap of $31,000. Independent undergraduates can borrow up to $57,500 total, while graduate students face a $20,500 annual limit and a $138,500 lifetime maximum, including any undergraduate borrowing. These limits are set by the U.S. Department of Education under the Direct Loan Program.

Meanwhile, the average cost of attendance at a public four-year university is roughly $27,000 annually for in-state students and around $45,000 for out-of-state students, while private universities average close to $59,000 per year, according to national higher-education cost data. Even after accounting for scholarships, grants, and work-study, most families still face a funding gap once federal loans are maxed out.

Recent policy changes have added new constraints. Starting with students entering school in fall 2026, Parent PLUS loans will be capped at $20,000 per year and $65,000 total per student, replacing the current system that allowed borrowing up to the full cost of attendance. However, there is no confirmed change yet to the graduate student lifetime limit, which remains $138,500 until officially updated in federal regulations.

When Private Loans Make Sense

Private loans should be your last resort, but they’re sometimes necessary:

After Exhausting Federal Options

The hierarchy is clear: Free money first (grants, scholarships, work-study), then federal loans, then private loans. Never skip federal loans to go straight to private borrowing.

If You Have Excellent Credit

Borrowers with credit scores above 750 and stable income can sometimes secure private rates below federal rates – particularly on variable-rate loans. But remember: private loans lack the safety nets that make federal loans valuable during tough times.

For Refinancing After Graduation

Once you’ve graduated and established strong credit and income, refinancing federal loans into private loans can save money if you’re confident you won’t need federal protections. This is only advisable for borrowers in stable, high-paying careers.

The Default Risk Factor

Default rates underscore why loan choice matters. Historically, about 10% of federal student loan borrowers defaulted within three years of entering repayment, though the pandemic payment pause temporarily pushed that figure down to around 2.3% for the most recent cohort. Students from for-profit colleges face the highest default rates, about 14.7%, while those at private nonprofit institutions average around 6.7%, according to federal data.

Those who default face serious consequences: wage garnishment, tax refund seizure, damaged credit, and loss of eligibility for future aid. Borrowers who take out loans but fail to complete their degrees are most at risk, roughly 45% default within 12 years, according to national studies.

Source: BestColleges

Private student loans show similar risk patterns but come with a crucial difference: they lack income-driven repayment and forgiveness protections.

The Income-Based Reality Check

Here’s the uncomfortable truth that makes federal loans essential: your financial situation after graduation is unpredictable. The 22-year-old engineering student confident in their six-figure salary prospects might face a recession, industry collapse, health crisis, or family emergency.

Federal income-driven repayment plans (IDR) ensure that student loan payments stay affordable based on actual earnings. Under these plans, borrowers typically pay 10–20% of their discretionary income, with remaining balances forgiven after 20–25 years of qualifying payments. Private loans offer no such safety net, your monthly payment remains fixed regardless of your income, and most lenders provide no path to forgiveness or income-based adjustment.

Action Items

Before borrowing a single dollar for college, complete the FAFSA to qualify for federal loans, grants, and scholarships. Always accept federal loan offers first, starting with Direct Subsidized Loans, which don’t accrue interest while you’re in school, followed by Direct Unsubsidized Loans. Only consider private loans once you’ve exhausted all federal options, and if you must borrow privately, compare offers from multiple lenders, as rates can vary widely. Before signing anything, calculate your total borrowing costs using a student loan calculator to understand the long-term impact.

The student loan landscape is changing rapidly. Starting in 2026, new borrowers will face stricter federal limits and fewer repayment protections. That makes careful planning more essential than ever. Still, one principle remains constant: federal loans first, private loans last, your future financial stability may depend on getting this sequence right.