Debt Consolidation vs Bankruptcy: The Truth About Your Credit Score

When debt feels unmanageable, choosing between debt consolidation and bankruptcy is critical because both affect your credit score differently. Consolidation or debt management can preserve your credit profile if payments stay current, while settlement and bankruptcy carry steeper, longer-lasting credit consequences. Understanding how each option impacts your FICO score and recovery timeline helps you decide the most effective path toward financial stability.

- Bankruptcy: Chapter 7 lasts up to 10 years on credit reports, typically dropping scores by 130–200 points; Chapter 13 stays for 7 years but may provide faster debt relief when obligations are unmanageable.

- Debt Consolidation & DMPs: Lower interest and one payment can stabilize credit; long-term improvement depends on consistent on-time payments and income stability.

- Debt Settlement: Settled accounts remain for 7 years, usually after missed payments that heavily damage FICO scores, making this the riskiest strategy.

- Credit Recovery: Across all paths, rebuilding hinges on timely payments, keeping utilization under 30%, and using tools like secured credit cards and credit-builder loans.

- Key Tradeoff: Bankruptcy delivers a faster reset but harsher short-term damage; consolidation or management preserves credit health if you have steady income and discipline.

When debt becomes overwhelming, many people find themselves weighing the choice between debt consolidation and bankruptcy. Both strategies are designed to provide relief, but they carry very different implications for your financial health, especially your credit score. Understanding these differences in depth can help you make an informed decision about which path may be right for your circumstances.

Debt Consolidation, Debt Management, and Settlement Explained

Debt consolidation typically involves taking out a new loan, often a personal loan or balance transfer credit card, to combine multiple high-interest debts into one. The goal is a lower overall interest rate and a single monthly payment, which can reduce stress and improve repayment consistency. When managed properly, consolidation can help stabilize your credit profile, as FICO scoring models view on-time payments positively.

A debt management plan (DMP) is facilitated through nonprofit credit counseling agencies. Instead of negotiating for less than you owe, the agency works with creditors to reduce interest rates or waive fees. You then make one monthly payment to the agency, which distributes funds to your creditors. DMPs generally take 3–5 years to complete, and while they do not carry the stigma of bankruptcy, they require strong discipline and consistent income.

Debt settlement, on the other hand, is a more aggressive strategy. For-profit companies negotiate with creditors to settle your debts for less than the full balance owed. However, these negotiations usually begin only after you’ve stopped making payments, which results in late fees, collections, and charge-offs on your credit report. The short-term damage to your FICO score is often severe, and many consumers do not complete these programs successfully.

Bankruptcy is the most formal option. Chapter 7 allows eligible filers to discharge unsecured debts, such as credit card balances and medical bills, in a matter of months. Chapter 13 sets up a court-supervised repayment plan over three to five years. Both forms of bankruptcy are public records and have the harshest impact on credit scores, but they can also provide a clear reset when debts are truly unmanageable.

How Each Option Affects Your Credit Score

Credit scoring models treat these debt relief strategies very differently:

-

Bankruptcy: According to FICO research, a bankruptcy filing can reduce a score by 130 to 200 points or more. The effect is greater for individuals who had higher scores before filing, because the drop is relative to the starting point.

-

Debt Consolidation Loans: A new loan may trigger a small, temporary dip due to a hard inquiry and the opening of a new account. However, as balances decline and on-time payments accumulate, scores often stabilize and eventually improve.

-

Debt Management Plans: Entering a DMP does not itself damage your score, but missed payments during the plan can be reported as delinquencies, undermining its benefits.

-

Debt Settlement: Because creditors typically require missed payments before negotiating, scores can plummet before any settlements are reached. Even after settlement, credit reports reflect “settled for less than owed,” which is viewed negatively by lenders.

The reason bankruptcy hits harder is because public records weigh heavily in scoring models, whereas new accounts or inquiries carry less weight over time.

How Long the Impact Lasts

The long-term visibility of these strategies also differs:

-

Bankruptcy: Chapter 7 remains on your credit report for up to 10 years, while Chapter 13 typically stays for 7 years. The negative impact is strongest in the early years but diminishes as you build positive credit history afterward.

-

Debt Consolidation Loans: These appear as installment accounts. Positive payment history benefits your score, while missed payments remain visible for up to 7 years.

-

Debt Management Plans: Your accounts remain open, and as long as payments are made on time, you can build positive history. Missed payments, however, linger on your report just like any other delinquency.

-

Debt Settlement: Notations of accounts settled for less than the full balance owed remain for 7 years. The long-term damage is significant, especially if multiple accounts were involved.

Long-Term Recovery Outcomes

Looking at 5–10 year horizons provides more perspective. Federal Reserve studies and academic research show that bankruptcy filers often re-enter the credit market sooner than expected. Many obtain credit cards or auto loans within a few years, albeit at higher interest rates, and some reach FICO scores in the mid-600s or higher within a decade if they avoid new delinquencies.

Debt management participants tend to experience steady improvements over time. Completing a DMP often correlates with lower rates of future bankruptcy filings, as individuals learn to manage credit more responsibly.

Debt settlement outcomes are mixed. While some succeed in reducing their overall debt burden, many fail to complete the programs, leaving accounts unresolved and credit scores damaged. This inconsistency makes settlement one of the riskiest strategies.

Choosing the Right Option

The right solution depends on your financial position:

-

Debt consolidation or DMP may be appropriate if you have a stable income, mostly unsecured debts such as credit cards, and the ability to commit to structured payments over several years.

-

Bankruptcy may be necessary if debts are clearly unmanageable, if you face legal actions like garnishments, or if a court-supervised discharge is more cost-effective than years of partial repayment.

Rebuilding Credit Afterward

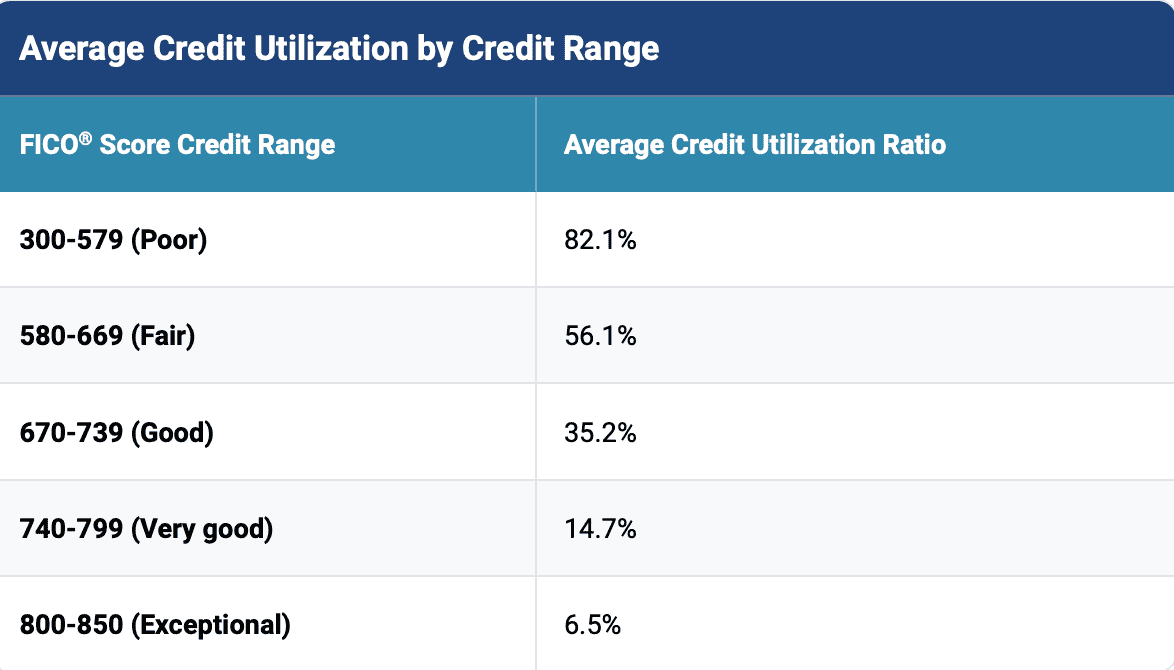

No matter which strategy you choose, the real work begins with rebuilding credit. Payment history makes up the largest portion of your FICO score, so making all future payments on time is essential. Keeping credit utilization below 30%, and ideally under 10%, shows responsible use of credit.

Source: Experian

Secured credit cards and credit-builder loans can help demonstrate positive activity. Regularly monitoring your reports through AnnualCreditReport.com ensures accuracy and gives you the chance to dispute errors. Finally, be cautious of scams, especially debt settlement companies charging high upfront fees. Nonprofit credit counseling agencies and court-approved programs remain safer options.

Final Takeaway

Debt relief is not one-size-fits-all. Bankruptcy is the most damaging in the short term but can provide a clean slate for those facing overwhelming obligations. Consolidation and DMPs are less harmful to credit if payments are maintained, but they require discipline and steady income. Settlement may resolve debts for less than owed but leaves lasting scars on your credit history.

Ultimately, your financial future depends less on the option you choose and more on what you do afterward. Consistent, positive credit behavior, on-time payments, low balances, and cautious borrowing, determines how quickly you recover and regain financial stability.

Related: This topic is part of the broader credit system. For an overview of how credit scores, loans, and debt work together, see our Credit & Debt guide.