The $93 Million Per Employee Secret: Why Every Bank Wants to Issue Stablecoins

In July 2025, the U.S. government formally legitimized stablecoins with the GENIUS Act, sparking a rush from major banks like JPMorgan, Citigroup, and Bank of America to launch their own tokens. Stablecoins, once niche tools for crypto traders, are now positioned to reshape profits, payments, and consumer finance. The shift is less about new technology and more about Washington’s green light and Wall Street’s hunger for yield and payment revenue.

- Regulatory breakthrough: The GENIUS Act (July 18, 2025) requires 100% reserves in U.S. dollars or Treasuries, shields stablecoins from SEC/CFTC jurisdiction, and grants priority rights to holders in bankruptcy.

- Massive profitability: Tether earned $14B in 2024 with only 150 employees, $93M per worker, by investing reserves in U.S. Treasuries at 4–5% yields.

- Payments disruption: Stablecoin transfers cost under 0.1% versus credit card fees of 1.1–3.5%, threatening the $187B U.S. payments industry and pressuring Visa, Mastercard, and banks to adapt.

- Consumer impact: Faster, cheaper, 24/7 payments could lower cross-border costs (6.62% average per World Bank) to near-zero and enable micropayments, discounts, and new retail models.

- Market outlook: With the global stablecoin market forecasted to surpass $2T by 2028, the competition now centers on who controls the flow, and profit, of digital dollars.

For years, stablecoins existed in the shadows of crypto markets, useful for traders, ignored by banks, and distrusted by regulators. They were simple in concept: digital tokens pegged to the U.S. dollar, designed to provide stability in a volatile market. Nothing revolutionary, at least on the surface.

Yet in 2025, something shifted. Suddenly, Wall Street’s biggest names, JPMorgan, Citigroup, Bank of America, even Mastercard, are treating stablecoins as the hottest opportunity in finance. What changed wasn’t the technology. It was the profit model and, more importantly, Washington’s blessing.

Washington Opens the Floodgates

On July 18, 2025, President Trump signed the GENIUS Act into law, a landmark bill creating the first federal framework for stablecoins in the United States. The legislation requires issuers to maintain 100% reserves in U.S. dollars or short-term Treasuries, prohibits deceptive marketing, mandates anti-money laundering compliance, and even grants holders special priority in the event of bankruptcy.

Just as important, the Act clarified that payment stablecoins are not securities or commodities, keeping them outside the jurisdiction of the SEC and CFTC. For banks that had been sitting on the sidelines, unsure of their legal footing, the law was effectively a green light.

The reaction was immediate. Citi CEO Jane Fraser told investors her bank was exploring a Citi-branded stablecoin. JPMorgan’s Jamie Dimon confirmed the bank would move forward with both its internal “deposit coin” and a stablecoin product. Even Bank of America signaled it was preparing to enter the space. The GENIUS Act had fired the starting gun on what many now call a digital gold rush.

The $93 Million-Per-Employee Business

Why the frenzy? Because the stablecoin business model might be the most profitable in modern finance.

Consider Tether, the world’s largest issuer. In 2024, the company reported $14 billion in profit with just 150 employees, a staggering $93 million per worker.

The mechanics are simple. When a customer buys one Tether, they hand over a dollar. That dollar is then invested in yield-bearing assets such as U.S. Treasuries. With over $162.5 billion in Treasury holdings, Tether has become one of the largest buyers of American debt, rivaling mid-sized countries.

At interest rates of 4–5%, that balance generates billions in annual income. Unlike traditional banks, which face strict capital requirements and regulatory costs, stablecoin issuers operate with fewer constraints, letting them allocate reserves more aggressively. The result: a profit engine unlike anything in mainstream banking.

The Payments Battle

But the appeal doesn’t stop at yield income. Stablecoins also threaten to upend the $187 billion U.S. payments industry.

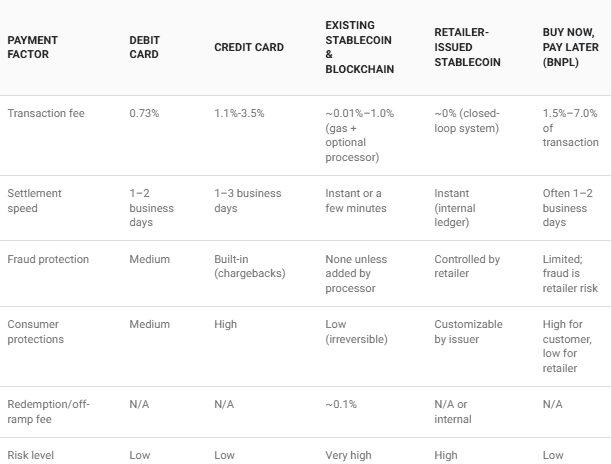

Credit card networks charge merchants between 1.1% and 3.5% per transaction. Stablecoin transfers, by contrast, cost under 0.1% and settle almost instantly. For a coffee shop, that means keeping an extra few cents on every latte sold. For a supermarket giant like Kroger, it could mean doubling margins in an industry where profit and payment costs are often neck-and-neck.

Source: The Motley Fool

Banks see the writing on the wall. Fintech challengers are already experimenting with stablecoin-based payments that bypass credit card networks entirely. By issuing their own stablecoins, banks can protect their turf, earning yield on reserves while capturing payment revenue in a system with fewer middlemen.

What It Means for Consumers

For everyday people, the impact could be transformative. Stablecoins promise faster payments, lower fees, and round-the-clock availability. Cross-border transfers, which currently cost an average of 6.62% according to the World Bank, could fall to pennies on the dollar.

Source: World Bank RPW

Perhaps most intriguing is the potential for micropayments. Credit card fees make transactions of just a few cents impractical, but stablecoins could enable pay-per-article content, tiny streaming tips, or micro-donations. Retailers might even offer discounts for customers who pay in stablecoins, passing along their savings.

Big tech firms are already exploring the opportunity. Both Amazon and Walmart are reportedly considering launching their own tokens, potentially creating closed-loop systems that eliminate processing fees while locking customers into their ecosystems.

Profit, Not Innovation

The irony is hard to miss. Cryptocurrency was born from a vision of eliminating financial intermediaries. Yet today, banks and corporations are embracing stablecoins to become the ultimate intermediaries, issuing digital dollars, investing the reserves, and charging fees at every turn.

The global stablecoin market, currently worth over $250 billion, is projected to surpass $2 trillion by 2028. With those kinds of numbers, it’s clear why financial institutions are racing to stake their claim.

At its core, this rush isn’t about revolutionary technology. It’s about control and who profits every time money moves. Right now, the answer is shifting rapidly toward Wall Street and corporate America.