How to Legally Shield Crypto Assets from Medicaid’s 5-Year Lookback Period

Medicaid examines asset transfers made within the 60 months before applying for long-term care. Transfers for less than fair market value usually trigger a penalty period when Medicaid will not pay for nursing home care. The penalty is calculated by dividing the value of the transfer by your state’s average monthly nursing home cost (the “penalty divisor”). Early planning using irrevocable trusts, exempt asset conversions, and Medicaid-compliant annuities can lawfully protect savings—especially when implemented before the five-year window. Because rules vary by state, consult an experienced elder law attorney

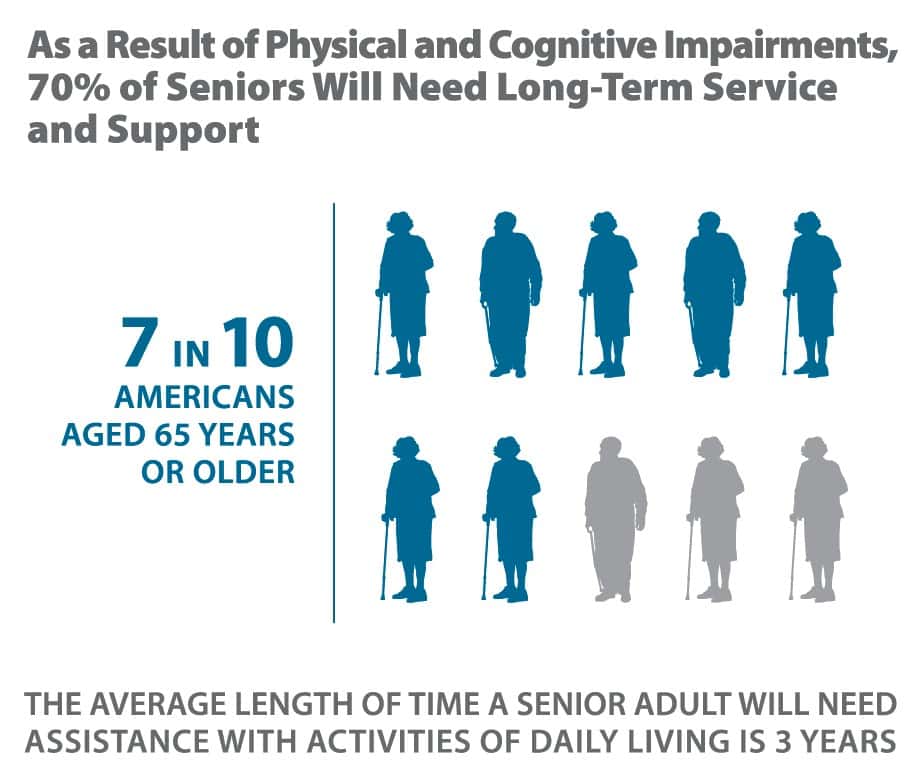

For many older adults, Medicaid becomes the critical safety net for long-term nursing home care. Yet gaining access to this coverage is not automatic. Federal law requires a thorough review of financial transactions to ensure applicants have not attempted to transfer or hide assets simply to qualify. This safeguard is known as the Medicaid “lookback” period. Understanding how this rule works, and how to plan in advance, can mean the difference between preserving your hard-earned savings and facing unexpected financial hardship.

What Is Medicaid’s 5-Year Lookback Period?

The Medicaid lookback period spans 60 months (5 years) prior to the date of application for long-term care coverage. Under federal regulations (42 CFR § 435.735), states must examine whether the applicant sold, gifted, or transferred assets for less than fair market value during this time. The purpose is to prevent individuals from offloading wealth to family members or others just before applying.

If transfers are found, the state imposes a penalty period during which Medicaid will not pay for care. This penalty is calculated by dividing the total value of the transferred assets by the state’s average monthly cost of nursing home care (commonly called the “penalty divisor”). Because nursing home care can cost between $7,500 and $10,000 per month, even modest transfers can create many months of ineligibility.

The Risks of Improper Transfers

Improper asset transfers can carry significant consequences that ripple through both finances and healthcare:

-

Delayed eligibility: You may be responsible for all nursing home bills during the penalty period.

-

Severe financial strain: Out-of-pocket costs can quickly exhaust retirement savings.

-

Loss of control: Transfers made without legal guidance can be hard to reverse, potentially leaving you with limited resources when you most need them.

These risks highlight why proactive planning, well before the five-year window, offers the best protection.

Source: JAMA Network

Legal Strategies to Protect Assets

While Medicaid is strict, there are legitimate strategies recognized by Centers for Medicare & Medicaid Services (CMS) and state Medicaid programs that can shield assets when structured properly.

Irrevocable Medicaid Trusts

An irrevocable trust allows you to remove assets from your ownership while still retaining some indirect benefits. For instance, you may place an investment property into the trust while continuing to receive rental income. To be effective, the trust must be established at least five years before applying for Medicaid. Courts rulings have consistently upheld such trusts when drafted correctly by experienced elder law attorneys.

Converting Countable Assets into Exempt Assets

The Centers for Medicare & Medicaid Services (CMS) provides federal guidelines on which resources do not count against Medicaid eligibility. While details vary by state, common exempt assets include:

-

A primary residence, subject to state-specific home equity limits.

-

One vehicle for personal transportation.

-

Household goods and personal belongings.

-

Prepaid funeral arrangements or burial plots.

In addition, applicants may legally spend down by converting countable assets into exempt categories, for example, paying down a mortgage, purchasing a modest replacement car, or making medically necessary home improvements. These strategies must follow Medicaid’s rules, including compliance with the five-year look-back period on asset transfers.

Medicaid-Compliant Annuities

A Medicaid-compliant annuity transforms a lump sum of savings into guaranteed monthly income. CMS requires that these annuities be irrevocable, non-transferable, and actuarially sound, meaning the payout period cannot exceed the applicant’s life expectancy. This tool is often used to protect a spouse still living in the community, ensuring they continue to receive income while the applicant qualifies for care.

Gifting and Transfers Outside the Lookback Period

While gifts made within the five-year lookback usually trigger penalties, transfers made before the window begins are generally safe. It is important to note that the IRS annual gift tax exclusion does not apply to Medicaid, every gift, even small ones, can be scrutinized if made within the five-year timeframe.

Documented Exceptions to the Rule

Federal and state Medicaid rules recognize that not every asset transfer is considered abusive under the five-year lookback period. Exceptions include:

-

Spousal transfers: Assets transferred to a spouse, or to a trust for the spouse’s sole benefit, are exempt under 42 U.S.C. § 1396p(c)(2)(B).

-

Caregiver agreements: Payments to family members for caregiving are valid only if supported by a written, legally binding contract at fair market rates. Without documentation, states typically treat them as gifts subject to penalty.

-

Special needs trusts: Assets placed in a properly structured special needs trust (d)(4)(A) or pooled trust for a disabled individual under age 65 are excluded.

These exceptions must be carefully structured, comply with federal statute and state Medicaid rules, and be supported by legal documentation to avoid being treated as disqualifying transfers.

Timing and the Importance of Early Planning

The central principle of Medicaid planning is acting early. Once you are within the five-year window, your options narrow dramatically. Establishing a trust, restructuring assets, or setting up annuities is far more effective when done well in advance of needing long-term care. Families that wait until a crisis often face reduced choices, higher risks, and costly mistakes.

Strategy Comparison

| Strategy | What It Does | When It Works Best | Key Requirements | Best For |

|---|---|---|---|---|

| Irrevocable Medicaid Trust | Moves assets out of your countable estate while allowing indirect benefits (e.g., income). | 5+ years before applying for Medicaid. | Proper drafting; funding; no retained control; 5-year seasoning. | Homeowners, investors with time to plan. |

| Exempt Asset Conversion | Converts countable assets into categories Medicaid does not count. | Before or during pre-planning; limited options inside lookback. | Follow state rules; FMV purchases; documentation. | Applicants needing quicker compliance. |

| Medicaid-Compliant Annuity | Turns assets into an income stream, often protecting a community spouse. | Approaching application; crisis planning for married couples. | Irrevocable; non-assignable; actuarially sound; state approvals. | Married couples; late-stage planning. |

When to Seek Legal Help

Medicaid rules are highly technical and differ across states. Missteps can result in months, or even years, of ineligibility. An experienced elder law attorney can:

-

Draft irrevocable trusts that meet Medicaid requirements.

-

Structure annuities to comply with CMS guidelines.

-

Apply state-specific exemptions and penalty divisor rules.

-

Formalize caregiver agreements to avoid later disputes.

Professional guidance ensures compliance with both federal standards and the unique regulations of your state’s Medicaid program.

Conclusion: Safeguarding Assets Through Proactive Strategy

Shielding your assets from Medicaid’s five-year lookback period is possible, but it demands foresight, strategy, and legal expertise. By leveraging irrevocable trusts, converting countable assets into exempt categories, utilizing compliant annuities, and understanding documented exceptions, you can preserve your savings while still securing access to essential care. Above all, the earlier you begin planning, the stronger your protection will be. For families concerned about long-term care costs, consulting an elder law professional can provide peace of mind and ensure financial security during retirement years.