Robinhood Q2 Earnings Beat Expectations, But Key Risk Factors Loom for Investors

Robinhood Markets Inc. posted a blowout Q2 2025 with revenue up 45% year-over-year to $989 million, EPS doubling to $0.42, and assets under custody hitting $279 billion. Yet beneath the strong numbers lie critical risks tied to regulation, market volatility, credit exposure, and expansion challenges. For investors asking whether Robinhood can evolve into a durable fintech platform, or remain dependent on cyclical trading enthusiasm, the answer hinges on its ability to manage costs and regulatory shifts while diversifying revenue.

- Trading dependency: Transaction-based revenue rose 65% to $539M, led by crypto (+98%) and options (+46%), but remains vulnerable to market downturns.

- PFOF scrutiny: Payment for order flow, a core revenue source, faces ongoing regulatory risk in the U.S. and abroad.

- Expansion challenges: Acquisitions of Bitstamp and WonderFi expand global reach but add regulatory and integration risk.

- Credit risk rising: Margin lending hit $9.5B (+90%), with provisions for credit losses up 56%—a red flag if markets tighten.

- Cost pressures: Marketing spend jumped 55% to $99M, and FY25 expenses are projected at $2.15–$2.25B, squeezing margins.

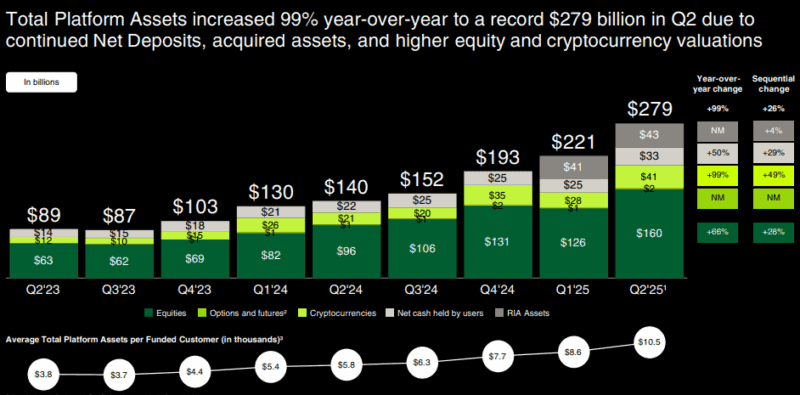

Robinhood Markets Inc. reported stellar financial results for Q2 2025, with revenue surging 45% year-over-year to $989 million and diluted EPS doubling to $0.42. The company added 2.3 million funded accounts, while assets under custody soared to $279 billion, nearly double from a year ago.

Source: Robinhood

However, despite these standout numbers, several underlying risks may cloud Robinhood’s growth narrative.

1. Overdependence on Market Volatility

Robinhood’s core revenue remains heavily reliant on trading activity, which is inherently cyclical. Transaction-based revenue climbed 65% to $539 million, led by:

-

Options trading: $265 million (up 46%)

-

Cryptocurrency trading: $160 million (up 98%)

Source: Robinhood

While impressive, these gains expose Robinhood to volatility-driven revenue swings. In a sustained market downturn, trading activity, and thus income, can decline sharply.

2. Regulatory Headwinds: PFOF Under Fire

A critical revenue stream, payment for order flow (PFOF), is still under scrutiny. Regulators in the U.S. and abroad have raised concerns over this practice, where Robinhood routes customer trades to market makers in exchange for compensation.

In its own filings, the company highlights “new regulation or bans on PFOF and similar practices” as a major risk factor. Should restrictions tighten, Robinhood may be forced to revamp its business model, potentially lowering margins or raising fees.

3. Global Expansion Carries Execution Risks

Robinhood’s international growth ambitions are accelerating. The company recently completed its acquisition of Bitstamp, a well-established cryptocurrency exchange with over 50 active licenses globally, and has also agreed to acquire WonderFi, a Canadian digital asset services firm.

While these moves diversify revenue, they come with challenges:

-

Navigating fragmented regulatory regimes

-

Integrating new operational infrastructures

-

Managing cross-border compliance and customer support

International expansion often demands significant resources and mistakes can be costly.

4. Rising Credit Risk Signals Caution

Robinhood’s credit risk is also quietly increasing. The provision for credit losses rose 56% year-over-year to $28 million, while Robinhood’s margin book jumped 90% to a record $9.5 billion. Rapid margin lending growth, paired with rising defaults, is a classic red flag. If economic conditions tighten or markets decline, loan delinquencies could spike, hurting the bottom line.

5. Crypto Exposure Deepens Risk Profile

Robinhood continues its aggressive push into crypto. With crypto-related revenue up 98% and new product launches rolling out in the U.S. and European Union, the company is increasingly banking on digital assets.

CEO Vlad Tenev recently said tokenization is “the biggest innovation our industry has seen in the past decade.” But exposure to crypto markets, which remain highly volatile and regulatory gray zones, adds further uncertainty to the company’s outlook.

6. Expense Growth Outpaces Revenue Momentum

Although revenue is surging, costs are accelerating too:

-

Marketing expenses rose 55% to $99 million

-

FY 2025 expenses are forecasted at $2.15–$2.25 billion, excluding items like credit loss provisions and costs related to WonderFi

This suggests customer acquisition is becoming more expensive, and headline growth may not translate into sustainable margins.

Investment Outlook: Proceed With Caution

While there is no doubt Robinhood’s headline numbers impress, the fine print reveals a company navigating some significant headwinds. With global ambitions and product innovation driving future growth, execution and risk management will determine whether the company matures, or stumbles. Robinhood’s Q2 performance underscores strong momentum in a favorable market environment. Its expansion into wealth management, crypto, and international markets demonstrates strategic intent to evolve beyond day trading.

But the company remains exposed to regulatory, operational, and credit risks. It also relies heavily on market enthusiasm, a fickle fuel for long-term stability. For investors, the key question is whether Robinhood can transition from a high-growth trading app to a durable fintech platform capable of weathering market cycles and regulatory changes.