EV Makers vs Battery Producers — Which Is the WORST Investment?

The electric vehicle (EV) revolution is maturing, and investors are rethinking where value lies. While both automakers and battery producers benefit from global EV adoption, cooling demand, overcapacity, and falling margins are hitting battery manufacturers harder. Established carmakers like Tesla, BYD, and Hyundai retain pricing power, diversified revenue, and scale advantages that battery producers increasingly lack.

- Oversupply pressures margins: Global battery capacity exceeded 3.3 TWh in 2024, already enough to meet demand, pushing prices down and squeezing producers’ profits.

- China’s dominance raises risk: China refines over 90% of graphite anodes, creating geopolitical and tariff exposure for Western suppliers.

- Automakers hold strategic control: Carmakers can reuse plants, diversify models, and integrate battery supply, while producers face commodity-like pricing and technology obsolescence.

- EV demand growth is slowing: Global EV sales are projected to surpass 20 million units in 2025, but growth has moderated due to weaker subsidies and high interest rates.

- Investor takeaway: Vertically integrated automakers with strong brands and cost efficiency offer more resilience than pure-play battery manufacturers in the next phase of the EV cycle.

The electric vehicle (EV) revolution has created two compelling investment narratives. On one side are the carmakers building the EVs themselves. On the other are the battery producers supplying the essential technology that enables those vehicles. Both groups have been hailed as major beneficiaries of the global energy transition. As 2025 unfolds, however, with growth in EV demand cooling, input costs rising, and competitive pressures intensifying, the landscape is shifting, and the risks appear greater for battery manufacturers than for most automakers.

The growth backdrop

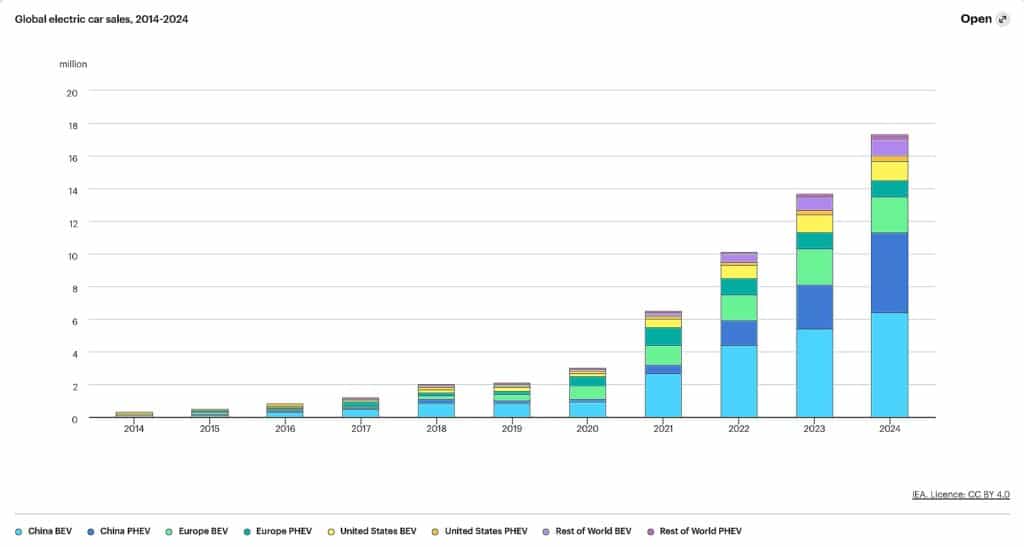

EV sales continue to expand, though not at the breakneck pace of the early 2020s. According to the International Energy Agency (IEA), global electric car sales exceeded 17 million in 2024, about one in five cars sold worldwide, and are projected to surpass 20 million in 2025, accounting for more than a quarter of all new car sales.

China remains the dominant market, responsible for roughly two-thirds of global EV sales, while Europe’s momentum has softened as subsidies were reduced and high interest rates dampened demand. North America’s share continues to rise gradually but remains below 12%, reflecting slower consumer adoption.

Source: IEA

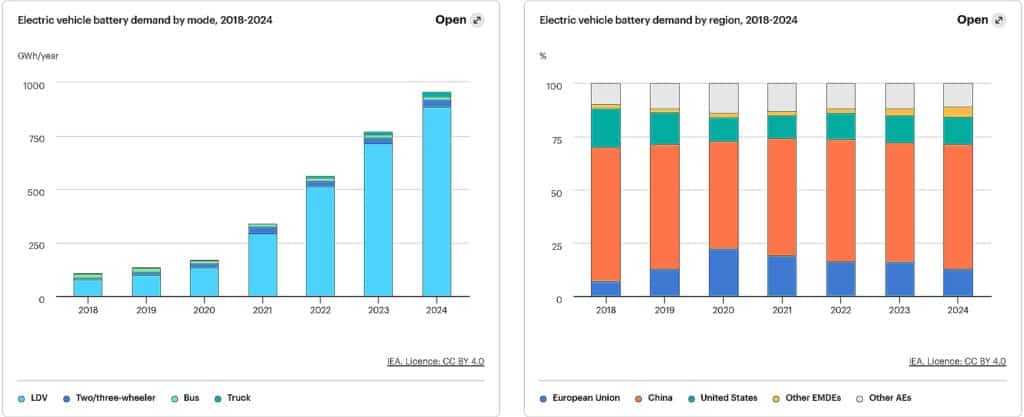

Battery demand is also rising sharply. The IEA estimates that global demand for EV batteries surpassed 1 terawatt-hour in 2024 and could exceed 3 TWh by 2030, more than tripling within the decade. Yet, rapid manufacturing expansion has outpaced demand growth. Global cell production capacity reached about 3.3 TWh in 2024 and is projected to double by 2030, creating oversupply pressures that are driving battery prices and producer margins lower.

Source: IEA

The strain on EV makers

Carmakers face growing financial and operational pressure as the shift to electric vehicles proves more expensive and complex than expected. Building EVs requires massive upfront investment in factories, batteries, and supply chains. Automakers such as Ford, General Motors, and Volkswagen have each committed tens of billions of dollars to expand production and secure battery supply. Yet demand growth has slowed relative to those ambitions, particularly as higher interest rates and reduced subsidies weigh on consumer adoption.

Profitability is under strain as price wars in China intensify and Tesla’s repeated cuts force rivals to follow suit. In early 2025, Lucid Group trimmed its annual production forecast amid weaker demand and rising costs, highlighting the fragile economics facing pure-play EV startups. Still, established automakers retain valuable fallback options: their internal combustion businesses continue to generate cash, and their scale, distribution networks, and brand strength offer resilience that battery producers and smaller entrants lack.

Why battery producers are under more pressure

Battery makers are caught in a tougher squeeze. While long-term demand remains strong, the industry faces overcapacity, fierce price competition, and reliance on volatile raw materials such as lithium, nickel, and graphite. According to the International Energy Agency (IEA), global lithium-ion battery pack prices fell sharply in 2024, around 30% in China and roughly 10–15% in the United States and Europe. Falling costs benefit carmakers but severely compress producers’ margins.

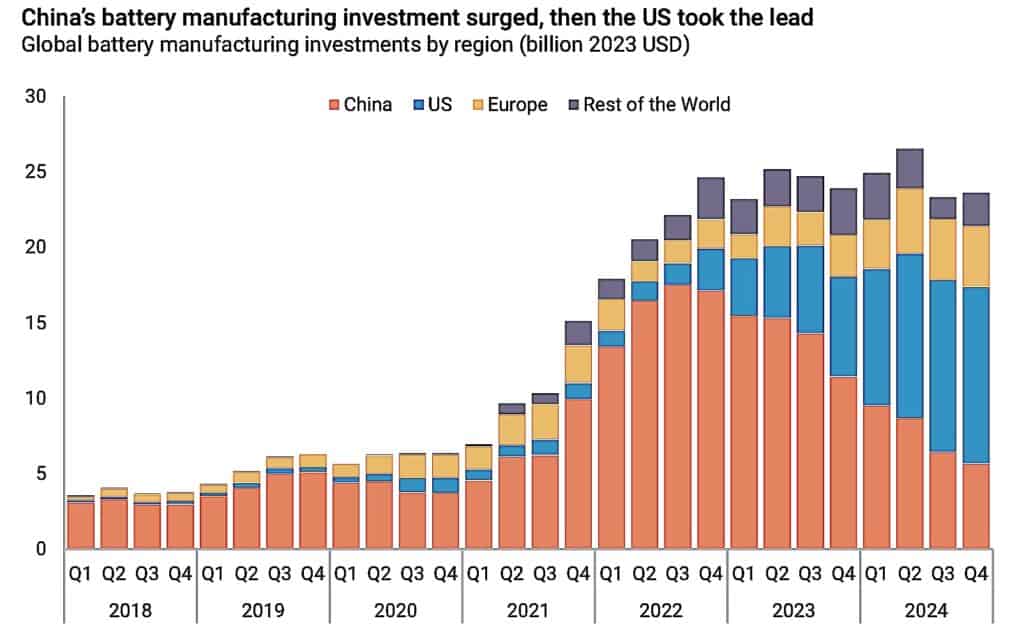

China’s manufacturing dominance compounds the problem. A 2025 report by Rhodium Group found that Chinese battery production capacity is nearly double its domestic demand and could already exceed global requirements if all plants operate at scale. With factories running ahead of consumption, global supply has outpaced demand, driving prices lower and heightening competition across producers.

Source: Rhodium Group

Geopolitics add further risk. More than 90% of the world’s graphite anode material, vital for EV batteries, is refined in China, according to Reuters. This concentration exposes Western manufacturers to export restrictions and potential supply shocks. Meanwhile, new tariffs among the U.S., EU, and China have clouded expansion plans, leading several proposed battery factories in the U.S. to be delayed or canceled amid uncertain incentives and rising costs.

In essence, battery manufacturing is increasingly resembling a commodity business, high volume, low margin, and highly sensitive to global trade and pricing dynamics.

Side-by-side comparison

Growth potential: Both sectors benefit from EV adoption, but automakers own the end-customer relationship and can layer revenue via options, financing, and (selectively) software. Battery producers remain tier-one suppliers tied to OEM order cycles with limited pricing discretion. Advantage: EV makers.

Profit margins: Battery manufacturers face ongoing price compression from capacity expansion and chemistry shifts, with profitability concentrated among a few leaders. Automakers’ pure-EV margins are thinner than ICE today, but portfolio profits are supported by scale, mix, and aftersales, while software/subscription upside is emerging, not guaranteed. Advantage: EV makers.

Capital intensity: Gigafactories require multibillion-dollar outlays with long ramps and yield risk. Car production is also capex-heavy, but legacy OEMs can reuse plants, platforms, and distribution, spreading costs across multiple nameplates and regions. Advantage: EV makers.

Competitive dynamics: The global battery market is concentrated in a handful of players led by CATL and BYD (with LG Energy Solution and Panasonic among the top), while many newer non-Chinese projects are still ramping and profitability is uneven. Leading automakers like Toyota, Tesla, and Hyundai maintain profitable product lines at the corporate level and wield scale and purchasing power. Advantage: EV makers.

Strategic risk: Battery firms are more exposed to trade barriers, input volatility (lithium, nickel, graphite), and fast-moving chemistry transitions (LFP, NMC, sodium-ion, solid-state). Car companies face brand and market-cycle risk but retain greater control over pricing, product mix, and supplier choice. Advantage: EV makers.

Why battery producers are the worse investment

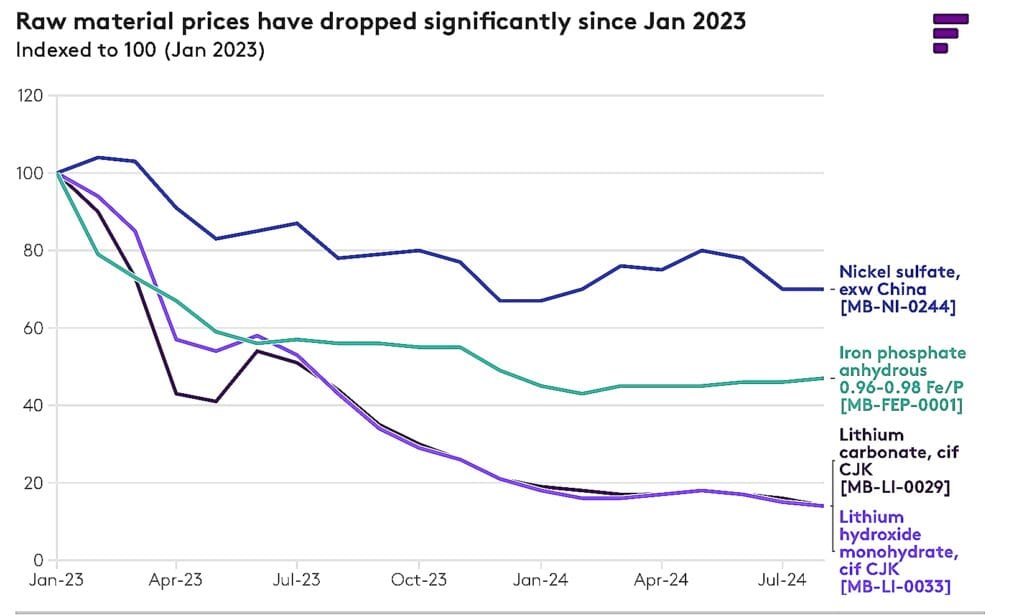

The core problem for battery producers is that competition has outpaced innovation. Prices for lithium and other key materials have dropped sharply from their 2022 peaks, but those savings have mostly been passed to automakers rather than boosting margins. Oversupply has become a structural issue, leaving even efficient manufacturers struggling to stay profitable as Chinese capacity now exceeds global demand.

Source: Fastmarkets

The industry is also highly exposed to rapid technological shifts. A company that commits billions to one battery chemistry risks having its assets rendered outdated within just a few years. Gigafactories demand huge upfront capital and are difficult to repurpose, while automakers can diversify, integrate production in-house, or switch suppliers as technologies evolve.

By contrast, EV manufacturers retain brand strength, control customer relationships, and enjoy greater flexibility in design and vertical integration. For investors, that degree of strategic control gives carmakers a far better cushion against the volatility and margin pressure crushing the battery sector.

But EV makers aren’t invincible

EV makers still face risks from soft consumer demand, rising financing costs, and policy uncertainty over incentives. The European Union’s new tariffs on Chinese EVs could invite retaliation, while the upcoming U.S. election may reshape subsidies under the Inflation Reduction Act. Global adoption also hinges on charging infrastructure, battery affordability, and grid readiness, factors largely beyond automakers’ control.

Even so, automakers have more defined paths to profitability than most battery specialists. Firms that can combine cost efficiency, brand strength, and production scale, such as Tesla, BYD, and Hyundai, are positioned to outperform as the market matures.

Implications for investors

Investors seeking EV exposure need to be selective. Among automakers, the strongest prospects are vertically integrated companies that control their battery supply chains and software ecosystems, giving them more stability and pricing power. For battery producers, firms with proprietary chemistry, cost efficiency, or diversified operations across regions are better positioned for long-term profitability.

Battery-focused ETFs and suppliers without strong intellectual property or scale could struggle if market oversupply continues. In contrast, EV-themed ETFs that include diversified automakers and software-integrated manufacturers may offer a more balanced and resilient risk profile for investors.

Final word

The EV transition is undeniably one of the century’s defining industrial shifts, but not all parts of the value chain will thrive equally.

Battery manufacturing, once seen as the heart of the electric revolution, is now weighed down by oversupply, thin margins, and geopolitical risk.

Automakers, though far from risk-free, hold the strategic advantage: they own the brands, control pricing, and can pivot as technologies evolve. For long-term investors, the smarter bet in the electric age lies with the companies selling cars, not just the ones selling the cells that power them.