Dividend Investing: Turn Your Portfolio Into a Paycheck

Dividend investing remains one of the most reliable long-term wealth-building strategies for U.S. investors in 2025. By owning shares in companies that pay regular dividends, investors can generate consistent income while benefiting from capital appreciation and compounding returns. The key is focusing on quality firms with sustainable payout ratios, moderate yields, and a track record of growing dividends over time.

- Dual Benefit: Dividends provide quarterly income while reinvested payouts accelerate compounding, mirroring the “rent plus appreciation” effect of real estate investing.

- Best Fit: Ideal for retirees, conservative investors, and long-term savers seeking predictable cash flow and reduced volatility. Dividend ETFs like VIG and SCHD offer diversified exposure.

- Smart Yields: Sustainable yields range from 2%–4% for blue-chip companies; yields above 7% may signal financial stress.

- Tax Edge: Qualified dividends are taxed at 0%, 15%, or 20%, while holding stocks in IRAs or 401(k)s can defer or eliminate taxes.

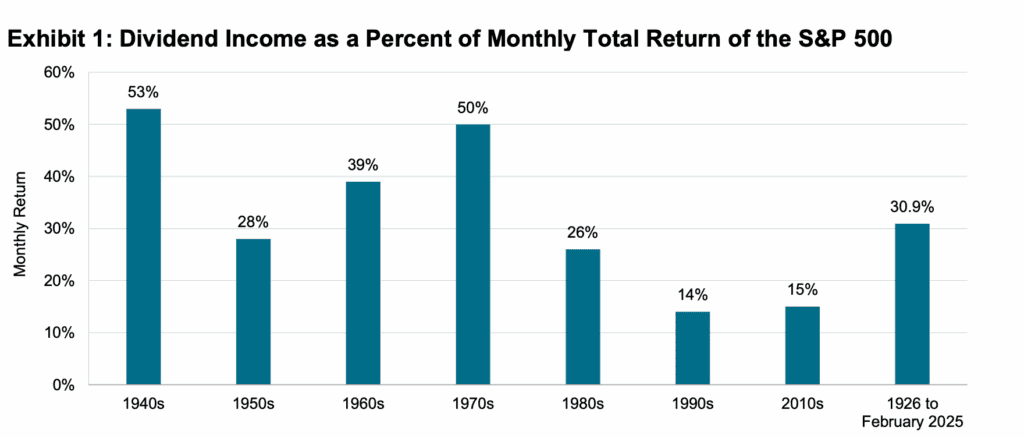

- Compounding Power: Reinvesting dividends through DRIPs amplifies total return, historically, dividends have accounted for roughly 31% of S&P 500 total returns (1926–2025).

Dividend investing is a long-term strategy focused on building wealth through steady income and compounding growth. It involves owning shares in companies that regularly distribute a portion of their profits to shareholders in the form of dividends. These payments, typically made quarterly, provide investors with a consistent income stream in addition to any potential capital appreciation from the stock’s price growth.

How Dividends Work

Dividends are typically paid by established companies with stable earnings. When a company declares a dividend, it announces a specific payout per share. For example, owning 100 shares in a company that pays $1 annually per share results in $100 of income, often distributed in four quarterly payments of $25 each.

Investors can either take dividends as cash or reinvest them through a Dividend Reinvestment Plan (DRIP), which automatically buys more shares. Reinvesting accelerates compounding, each new share earned generates additional future dividends, creating exponential growth.

Companies may increase, reduce, or suspend dividends based on earnings or financial conditions. Sectors like utilities, telecommunications, and consumer staples often pay stable dividends, while growth-oriented sectors like technology may reinvest profits instead of distributing them.

Who is Dividend Investing Best Suited For?

Dividend investing appeals to several types of investors:

Retirees and near-retirees often favor dividend stocks because they provide regular income without needing to sell shares. This creates a sustainable cash flow to cover living expenses while preserving the principal investment.

Conservative investors appreciate the stability that dividend-paying companies typically offer. These tend to be established, profitable businesses with predictable earnings, which generally experience less dramatic price swings than growth stocks.

Long-term wealth builders use dividend reinvestment to accelerate portfolio growth. By automatically using dividend payments to purchase additional shares, investors benefit from compound growth over decades.

Income-focused investors of any age who want to supplement their salary or create passive income streams find dividends attractive as an alternative or complement to bonds and other fixed-income investments.

Dividend investing may be less suitable for younger investors with long time horizons who can tolerate higher volatility in exchange for potentially greater capital appreciation from growth stocks, or for those in high tax brackets who want to minimize current taxable income.

Pros and Cons of Dividend Investing

| Pros | Description |

|---|---|

| Steady income | Provides regular cash flow even during market downturns. |

| Lower volatility | Dividend stocks are typically more stable and mature. |

| Compounding | Reinvested dividends generate additional returns over time. |

| Inflation hedge | Growing dividends help maintain purchasing power. |

| Real returns | Delivers tangible income while waiting for price growth. |

| Quality signal | Consistent payers often indicate strong, reliable companies. |

| Cons | Description |

|---|---|

| Slower growth | Less reinvestment may limit long-term expansion. |

| Taxable income | Dividends are taxed annually, even if reinvested. |

| Cuts hurt | Dividend reductions can lower income and share value. |

| Yield traps | Very high yields may signal financial trouble. |

| Sector bias | Concentration in a few industries reduces diversification. |

| Missed upside | May underperform growth stocks over long periods. |

Returns: Growth Potential vs. Dividend Yield

Understanding the balance between dividend yield and stock price growth is crucial. The dividend yield spectrum typically ranges from 2% to 6% for most blue-chip stocks. Yields above 7% often signal risk. Yield is calculated by dividing the annual dividend by the stock price, meaning it fluctuates as prices move.

There is an inverse relationship between dividend yield and growth potential. High-yield companies like utilities or mature consumer firms often have limited growth prospects. In contrast, firms with moderate yields but strong dividend growth tend to outperform long-term by combining income with price appreciation.

Focusing on total return, dividends plus price appreciation, is essential. A stock yielding 2% with 10% annual dividend growth and 8% price gains provides a total return near 10%, outperforming a 6% static-yield stock with no growth.

Research from S&P Global shows dividends have historically contributed about 31% of the S&P 500’s total return between 1926 and 2025. This underscores their importance in compounding wealth over time.

Source: S&P Global

As of 2025, the S&P 500 Dividend Aristocrats Index includes 69 companies that have raised dividends for at least 25 consecutive years. The elite Dividend Kings have increased dividends for over 50 years. These firms typically offer sustainable yields between 2% and 4%.

Sustainability is measured through the payout ratio, the percentage of earnings paid as dividends. A healthy range is 40–70%. Ratios above 80% suggest limited flexibility, making dividends vulnerable to cuts during downturns.

Tax Considerations

Taxes significantly influence dividend returns. Qualified dividends, those from U.S. corporations held for more than 60 days during the 121-day period surrounding the ex-dividend date, are taxed at long-term capital gains rates: 0%, 15%, or 20%, depending on taxable income. Non-qualified dividends are taxed as ordinary income, with rates from 10% to 37%.

High earners face an additional 3.8% Net Investment Income Tax on dividend income if their modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). State and local taxes can further reduce returns depending on where investors live.

Holding dividend stocks in tax-advantaged accounts like IRAs or 401(k)s eliminates annual tax drag. Dividends grow tax-deferred or tax-free, depending on the account type, enhancing long-term compounding. In contrast, dividends in taxable accounts reduce reinvestment power each year due to immediate taxation.

For traditional IRA holders, dividends contribute to required minimum distributions (RMDs) starting at age 73, which may increase taxable income in retirement.

Estate planning also plays a role. Dividend-paying stocks in taxable accounts receive a step-up in cost basis at death, eliminating capital gains taxes for heirs. However, dividends earned during the investor’s lifetime remain taxable.

Getting Started

For new investors, diversified dividend ETFs offer an easy entry point. Funds like the Vanguard Dividend Appreciation ETF (VIG), Schwab U.S. Dividend Equity ETF (SCHD), and ProShares S&P 500 Dividend Aristocrats ETF (NOBL) provide instant diversification and exposure to financially sound, income-generating companies.

Successful dividend investing requires focusing on total return, not just high yields. The best results come from combining consistent dividend growth with solid capital appreciation potential. Over time, this strategy builds both wealth and financial stability.

Dividend investing rewards patience, discipline, and reinvestment. By focusing on quality companies, sustainable yields, and long-term compounding, investors can create a resilient portfolio that delivers dependable income and steady growth for decades.