AI Startups vs Cloud Giants — Which Is the WORST Investment?

Artificial intelligence may define this decade’s economy, but its profits increasingly flow to the cloud providers, Amazon, Microsoft, and Google, not the startups building on top of them. Venture-backed AI firms raised roughly US$34 billion in early 2025, yet many remain unprofitable and depend on renting compute from the very incumbents they seek to disrupt. Cloud giants, by contrast, monetize AI through established enterprise services and steady margins exceeding 30%. Regulation and high GPU costs amplify the gap: scale and infrastructure ownership now define the winners.

- Funding concentration: AI startup valuations surged, but deal counts fell, signaling a bubble-like shift toward fewer, bigger bets.

- Cloud dominance: Amazon, Microsoft, and Google control about two-thirds of global cloud infrastructure, generating stable recurring revenue.

- Cost asymmetry: Startups rent expensive GPUs like NVIDIA’s H100s, while cloud firms spread costs across vast customer bases.

- Regulatory advantage: Large platforms can absorb new EU AI Act and U.S. compliance costs, turning oversight into a competitive moat.

- Investor takeaway: Startups promise speed; clouds deliver durable profits. Ownership of infrastructure, not hype, defines long-term returns.

Artificial intelligence has become the defining economic story of the decade, reshaping industries, capital flows, and corporate strategy. The race to dominate it has split into two powerful camps. On one side are the AI startups, agile, experimental, and driven by venture capital. On the other are the cloud giants, Amazon, Microsoft, and Google, which own the infrastructure powering nearly every large-scale AI model.

Both are competing for investor capital, but the dynamics could not be more different. Startups sell a story of speed and disruption, while cloud providers monetize the underlying compute, data, and services that make AI possible. As 2025 unfolds, each faces rising costs, regulatory pressure, and fierce competition for talent and energy resources. Yet the balance of risk is uneven. Based on current funding and efficiency data, AI startups remain the riskier bet, with valuations often outpacing sustainable growth compared with the diversified revenue engines of the cloud giants.

The funding surge and the hype gap

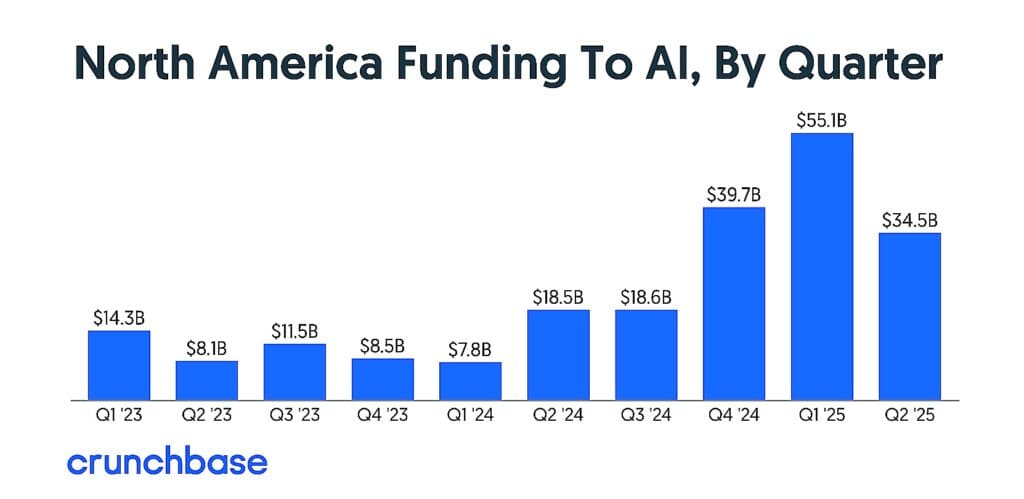

AI startups have dominated global venture investment over the past year. In the first half of 2025, AI-related companies raised around US$34 billion, according to Crunchbase. While funding volume surged, the number of deals declined, signaling a shift toward fewer but larger rounds concentrated among top players. Valuations have climbed sharply, driven by investor enthusiasm and a handful of mega-deals, creating a funding landscape reminiscent of late-cycle tech booms, where profitability often remains distant.

Source: Crunchbase

In contrast, the global cloud computing market is valued at roughly US$913 billion in 2025, based on Precedence Research, and continues to expand at an annual rate exceeding 20%. While cloud providers lack the hype surrounding AI startups, they benefit from stable recurring revenues, entrenched enterprise contracts, and proven profitability. Their growth may be steadier, but their earnings are real.

Source: Precedence

Profit versus promise

The financial gap between the two groups is stark. The three largest cloud providers, Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, control roughly two-thirds of global cloud infrastructure, according to CloudZero. In 2025, AWS generated about US$30.9 billion in quarterly revenue with an operating margin of around 33 %. Microsoft’s Intelligent Cloud division, which includes Azure, earned roughly US$28 billion for the same period, growing more than 20 % year-on-year. These are profitable, scaled businesses built on long-term customer relationships.

AI startups, meanwhile, are still searching for economic footing. Training a large language model (LLM) can cost tens of millions of dollars in computing power and specialized chips, according to the Stanford AI Index 2025. Every time users query those models, additional inference costs are incurred, often paid to the same cloud providers that host the infrastructure. The result is a structural dependency: many AI startups rely financially on the very companies they aim to disrupt.

Source: Stanford AI Index

The infrastructure trap

The biggest irony of the AI boom is that its most ambitious startups rely on renting their most expensive inputs. Access to high-performance GPUs such as NVIDIA’s H100 chips remains costly and supply-constrained, and few startups can afford to build large compute clusters from scratch. This dependence forces them to lease capacity from the major cloud providers, Amazon Web Services, Microsoft Azure, and Google Cloud, locking them into cost structures that often rise in step with user growth.

Cloud giants also face enormous capital expenditure, but they spread those costs across a vast portfolio of services. Microsoft and Google are embedding AI capabilities directly into Office 365, Ads, and Search, monetizing their infrastructure through existing customer bases without overhauling their core business models. For every dollar spent on data centers and chips, these firms generate multiple revenue streams. Startups centered on a single model or service cannot replicate that scale advantage, and risk being trapped by the very infrastructure that powers their innovation.

The profitability paradox

AI’s economics favor scale over speed. Once the enormous fixed costs of infrastructure and model training are absorbed, each additional user or query becomes relatively inexpensive. Cloud providers, especially Amazon, Microsoft, and Google, are built for this model, leveraging global infrastructure and enterprise clients to spread costs efficiently. AI startups, by contrast, often pay premium cloud rates while competing against rapidly improving open-source models that erode their pricing power.

The result is worsening unit economics. According to Gartner, about 29% of large enterprises have deployed generative AI, meaning most remain in the experimental stage. This leaves startups chasing a market where customers are cautious and monetization is uncertain.

Source: Gartner

That tension explains why private AI valuations keep climbing even as public markets grow skeptical. Investors continue to price in long-term dominance that may never materialize. History suggests only a few platform leaders, such as OpenAI or Anthropic, will achieve lasting scale, while many others consolidate or vanish once capital tightens.

Cloud giants: slower, but safer

While cloud growth has moderated, its fundamentals remain robust. Corporate IT spending continues to shift from on-premise systems to cloud-hosted infrastructure, and artificial intelligence has become a powerful new growth driver. The ongoing AI infrastructure boom has led to record capital expenditures by AWS, Microsoft, and Google Cloud, as each races to expand GPU and data-center capacity to meet surging demand. Every new AI workload adds incremental usage, and therefore revenue, to these platforms, reinforcing a self-sustaining cycle where startups and enterprises alike must rent compute from them to train and deploy models.

That dynamic effectively makes the cloud giants the landlords of the AI economy. Their businesses are diversified, regulated, and consistently profitable, supported by recurring enterprise contracts and long-term service agreements. They may not deliver the explosive returns of early-stage AI startups, but their growth is steadier, their margins more durable, and their risk profile far more predictable.

The regulation squeeze

Regulation is emerging as a major headwind for both AI startups and cloud giants, but its impact is uneven. The EU AI Act, the UK AI Safety Summit commitments, and the White House Executive Order on AI all impose tougher standards around model transparency, data governance, and safety.

For small startups, the cost of compliance, audits, legal reviews, and documentation, can consume scarce capital and slow innovation. In contrast, large cloud companies have the compliance teams, infrastructure, and lobbying power to manage these rules efficiently. They may even turn regulation into a competitive moat, shaping standards that smaller rivals must follow. In an increasingly regulated AI market, scale itself becomes protection.

Sentiment and valuation

Public markets have already shown a clear preference. Shares of Microsoft and Amazon have outperformed most major tech peers in 2025, supported by strong AI-driven revenue growth in their cloud divisions. Microsoft’s Azure and Amazon Web Services both reported double-digit gains from AI workloads, helping them stay ahead of broader market indices like the Nasdaq Composite in several quarters.

In contrast, private AI valuations are showing early signs of fatigue. A Goldman Sachs report cautioned that many AI startups remain “years away from sustainable profitability,” with valuations often “front-loading expectations of future dominance.” Investors are increasingly questioning when, if ever, these companies will deliver consistent earnings.

Ultimately, AI startups are trading on potential, while cloud giants are trading on performance. That distinction matters in a market where interest rates remain elevated and capital allocation is becoming more selective.

The verdict

AI startups may capture the thrill of innovation, but cloud giants dominate the economics behind it. Startups face steep capital costs, thin margins, growing regulatory scrutiny, and reliance on infrastructure they don’t own. Cloud providers, by contrast, generate consistent cash flow and control the digital “rails” that power AI.

That doesn’t make them risk-free. Growth is slowing, competition is intense, and capital expenditure remains heavy. Yet their risks are measurable, and their business models are proven. The startup ecosystem, meanwhile, resembles a high-stakes experiment where only a few will endure.

By 2025, the verdict is clear: in the debate over AI Startups vs. Cloud Giants, Which Is the Worst Investment?, startups carry the higher risk. They are more expensive, more speculative, and less anchored in sustainable economics. The cloud giants may not deliver explosive gains overnight, but they own the infrastructure, the customers, and increasingly, the profits.

Final word

The future of artificial intelligence will not hinge solely on who builds the most advanced model, it will be defined by who controls the compute, data, and distribution networks that sustain it. The past year has made one thing unmistakably clear: innovation may start at the edges, but value accrues at the core.

AI startups will continue to push boundaries and capture headlines, but their dependence on rented infrastructure, volatile funding, and unproven monetization keeps them vulnerable. Cloud giants, meanwhile, sit atop the digital supply chain. They provide the chips, data centers, and enterprise ecosystems that every ambitious model depends on. Every AI query, training run, or deployment ultimately passes through their gates.

For investors, the contrast is instructive. Startups promise velocity; the cloud incumbents deliver durability. One offers potential, the other scale. In an era where capital is growing more selective and regulation more demanding, ownership of infrastructure, not hype, defines the winners.

The next phase of the AI economy will be remembered not for who moved fastest, but for who built the foundations others had to rent.