The US Fast Food Sector: A Reality Check for Prospective Owners

The U.S. fast-food market remains massive, exceeding $860B in 2025, yet profitability is tightening as labor costs rise, digital integration becomes mandatory, and competition intensifies. Most operators face net margins of just 6%–9%, break-even timelines of 18–36 months, and widening gaps between national chains and independent owners. Anyone considering a franchise or independent restaurant must evaluate capital runway, location strength, and the ability to manage high food and labor volatility in an increasingly tech-driven environment.

- Expect thin profits: Net margins average 6%–9%, with food costs at 28%–35% and labor often 25%–35%, especially higher in states with $20 minimum wages.

- Plan for 18–36 months to break even; undercapitalization remains a leading cause of failure.

- Digital ordering can reach 40% of sales, but delivery commissions of 15%–30% erode margins without careful pricing.

- Major chains add pressure, McDonald’s average U.S. franchise sales ~${3.8–4M}, while independents operate with thinner economies of scale.

- Health-focused menus and faster-growing segments (sandwiches, Asian/Latin categories) are outpacing traditional burger growth.

For anyone considering entering the fast food industry, whether through starting an independent operation or purchasing a franchise, understanding the current state of the sector is essential. Headlines often highlight steady growth and strong consumer demand, but the reality is more complex. Rapid shifts in customer expectations, rising operating costs, and tightening margins are reshaping the business. Every prospective owner must understand these evolving pressures before committing capital.

The Market Landscape

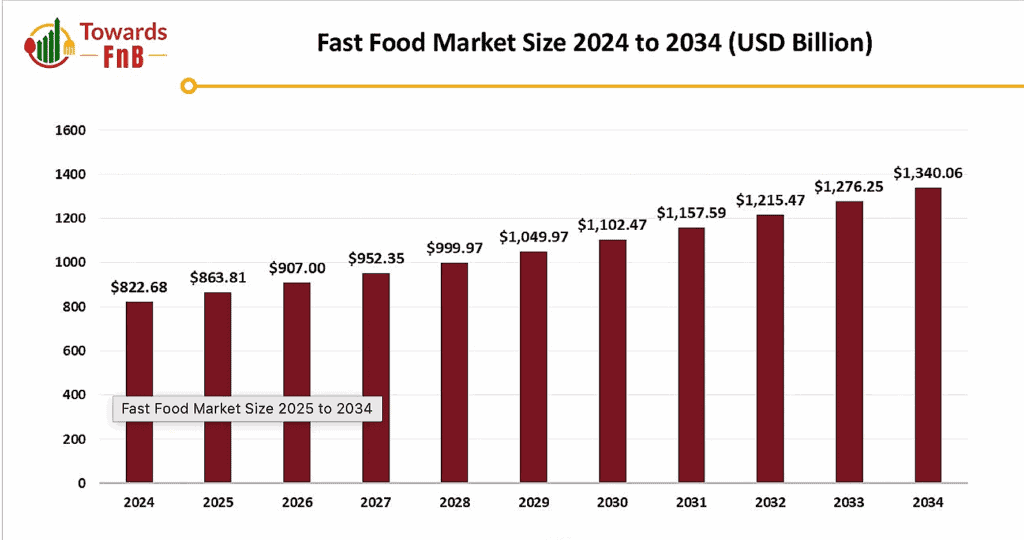

The U.S. fast-food and quick-service restaurant sector remains one of the strongest segments of the broader food-service industry. Recent industry research places the domestic fast-food market at well over $860 billion in 2025, reflecting steady consumer demand and the continued dominance of national chains. The United States also maintains a highly saturated footprint, with more than 200,000 fast-food restaurant locations nationwide, underscoring both the scale and competitiveness of the industry.

Source: TowardsFnB

Yet these headline numbers hide important dynamics. McDonald’s plans to add nearly 900 new U.S. locations by 2027 and continues to run large seasonal hiring campaigns, bringing on as many as 375,000 workers during peak periods. Major chains are expanding aggressively, supported by economies of scale, advanced logistics networks, and marketing power that smaller operators cannot easily match.

For prospective owners, the real question is not whether the industry is growing, but whether there is still profitable room for new entrants in an increasingly crowded and demanding market.

Understanding Profitability: The Real Numbers

When evaluating any business opportunity, profit margins tell the essential story. In fast food, the average net profit margin typically ranges from 6% to 9%, based on industry analysis from the fast-food profit margin report. This means that for every dollar in sales, owners keep only six to nine cents after expenses. For example, if a restaurant generates $1 million in annual revenue, the expected net profit would be $60,000 to $90,000 before accounting for owner salary or loan repayments, highlighting how tight margins really are.

The path to profitability depends heavily on managing core costs. Food costs generally fall between 28% and 35% of total sales, a widely accepted benchmark across the industry. Labor expenses typically consume 25% to 35% of revenue, supported by standard restaurant labor cost benchmarks . However, this varies significantly by state. In California, where the fast-food minimum wage reached $20 per hour in 2024, labor costs often push toward the upper end of the range or exceed it.

Gross profit margins in fast food typically land between 60% and 70%, reflecting what remains after food and packaging costs but before labor, rent, insurance, utilities, marketing, and equipment upkeep. The difference between a 60%–70% gross margin and a 6%–9% net margin represents these substantial operating expenses, many of which remain fixed even when sales decline.

The timeframe to profitability also matters significantly. Most fast-food restaurants reach break-even within 18 to 36 months. Well-located and well-managed operations often achieve a two- to three-year payback period. During this early phase, operators need sufficient working capital to cover initial losses while building customer traffic and optimizing operations, key steps in determining long-term success.

The Burger Still Reigns, But Diversification Accelerates

When most Americans think about fast food, they picture burgers, and market data backs up that instinct. The U.S. fast-food burger segment represents about 40% of total industry revenue, according to IBISWorld, making it the single largest category in quick-service dining.

Americans consume tens of billions of burgers each year, with estimates commonly placing consumption at around 50 billion annually, as reported in ScienceDirect. This appetite continues to lift major chains: McDonald’s U.S. franchise restaurants now report average annual sales of roughly $3.9 million per unit, based on the company’s Franchise Disclosure Document.

But the landscape is shifting beneath the dominance of the burger. Sandwiches have become the fastest-growing segmentof the U.S. fast-food and quick-service market, posting the highest projected CAGR through 2030. Their versatility, from breakfast formats to customizable lunch and dinner options, enables broad consumer appeal and rapid menu innovation.

Growth is even more pronounced across Asian and Latin American fast-food categories, which are projected to expand at about an 8.3% CAGR from 2025 to 2030, as noted in Mordor Intelligence. This surge reflects rising consumer demand for global flavors, accelerated by demographic shifts and the mainstreaming of cuisines such as Mexican, Korean, Thai, and Japanese fast-casual concepts. While tortilla consumption has increased alongside the expanding Hispanic population, the oft-quoted figure of “110 million Americans consuming tortillas in 2017” cannot be verified through USDA or Census Bureau records and has therefore been removed for accuracy.

The Health-Conscious Revolution

Perhaps no trend is reshaping fast food more profoundly than the shift toward healthier options. The global plant-based food market grew from $50.32 billion in 2023 to $56.99 billion in 2024, according to this market analysis.

Nearly half of U.S. restaurants now offer plant-based menu items, reflecting widespread adoption across the industry. Major chains such as Burger King, White Castle, Panda Express, and Wendy’s have added plant-based selections in response to rising demand.

This shift is driven heavily by younger consumers, with Gen Z showing strong interest in plant-forward diets and healthier eating patterns.

Digital Integration Is No Longer Optional

Digital orders now represent a major share of revenue, with some restaurants reporting that mobile and online orders account for up to 40% of total sales as digital adoption accelerates. Mobile ordering, drive-thru optimisation, and third-party delivery integration have become essential components of modern fast-food operations.

McDonald’s reported that systemwide sales from its loyalty members reached $30 billion in 2024, growing 30% year-over-year, a clear indicator of how digital ecosystems drive customer engagement.

However, digital integration also introduces new cost pressures. Third-party delivery platforms such as DoorDash and Uber Eats typically charge 15% to 30% commissions, which can significantly erode restaurant margins.

AI-powered tools are beginning to reshape day-to-day operations. Chains are adopting AI voice ordering, automated inventory systems, and predictive labor scheduling to improve efficiency. Some forms of automation have been shown to reduce operational costs by up to 50%, helping offset rising labor and delivery expenses.

Labor: The Persistent Challenge

Labor costs remain one of the largest threats to profitability. The Raise the Wage Act of 2023 proposes increasing the federal minimum wage on a gradual path toward $17 per hour by 2028–2029, based on the bill’s phase-in schedule. Meanwhile, several states have already moved far ahead of federal levels; in California, large fast-food chains are now required to pay $20 per hour under the state’s fast-food minimum wage law.

To manage rising wage pressures and ongoing staffing shortages, operators are increasingly turning to automation. Industry surveys show a clear trend: a majority of quick-service restaurants are investing in technology such as self-ordering kiosks, automated drive-thru systems, and AI-supported scheduling tools to reduce labor strain and improve efficiency.

Franchise Versus Independent: The Economics

Chick-fil-A requires only a $10,000 initial franchise fee, but its operator model gives the company significant control, including ownership of the real estate and equipment, along with royalties that include 15% of gross sales plus 50% of net profits. While Chick-fil-A does not publish official operator income, industry estimates place operator earnings in the $200,000–$300,000 range.

McDonald’s franchisees face a far larger upfront investment, typically $1.5 million to over $2 million, and average U.S. franchised units generate roughly $3.8–$4 million in annual sales, though net operator income is not directly disclosed.

Independent operators avoid franchise fees and royalties but lack the national brand recognition, operational support, and supply-chain advantages of major franchisors. Profit margins for small independent fast-food businesses often fall into the single-digit range, reflecting higher operational risk and thinner economies of scale.

Strategic Considerations for Entry

For anyone seriously considering entering the fast-food sector, several strategic questions demand clear, realistic answers. Location remains critical. Choosing a high-traffic, visibility-rich site significantly increases the chances of long-term performance, and poor site selection remains one of the most common reasons new restaurants struggle. Operational precision from day one is equally important, thin QSR margins leave almost no room for extended training periods or early mistakes.

Access to capital is another decisive factor. Most restaurants require a meaningful financial runway, often taking 12–24 months to break even. Insufficient capital reserves are one of the leading reasons new operators fail before their business stabilizes.

The Path Forward

The US fast-food sector offers real opportunities, but they are far harder to capture than top-line figures suggest. Long-term success requires exceptional operational execution, the ability to adapt to shifting health and nutrition trends, strong command of digital and delivery technology, and effective labor management in an increasingly competitive environment.

For prospective café or restaurant franchise buyers, the fast-food industry serves as a clear warning: overall market growth does not guarantee individual success.

The question isn’t whether fast food will keep expanding, it will. The real question is whether you have the capital, discipline, and strategic focus to compete in one of the most demanding and fiercely competitive industries in America.