Best Car Insurance Rates: State-by-State Comparison and Money-Saving Strategies

Auto insurance costs in the U.S. differ dramatically by location, with drivers in the most expensive states paying nearly three times more than those in the cheapest for similar coverage. As of late 2025, the national average cost of full-coverage auto insurance is about $2,894 per year, but where you live can add or subtract thousands annually. State regulations, weather risks, traffic density, uninsured motorist rates, and local claims costs all play major roles in pricing, making comparison shopping one of the most effective ways for drivers to save.

- Most expensive states: Nevada leads the nation at roughly $286 per month for full coverage, followed by Florida (~$270) and Michigan (~$260).

- Most affordable states: Vermont has the lowest average full-coverage cost at about $996 per year (~$83/month), with Maine and New Hampshire close behind.

- Why location matters: High uninsured motorist rates, severe weather exposure, dense traffic, and no-fault insurance systems all push premiums higher in certain states.

- Premium trends: U.S. auto insurance rates rose about 10%–12% in 2025 versus 2024, slower than prior years, with some states seeing decreases after prolonged increases.

- How to save: Comparing quotes from three to five insurers, bundling policies, adjusting deductibles, and using available discounts can save hundreds, or more, per year.

The cost of auto insurance varies significantly by location, with drivers in some states paying nearly three times morethan those in others for comparable coverage. Understanding these regional differences, and applying smart comparison-shopping strategies, can help drivers save hundreds or even thousands of dollars annually on premiums.

The National Landscape: Where Rates Stand

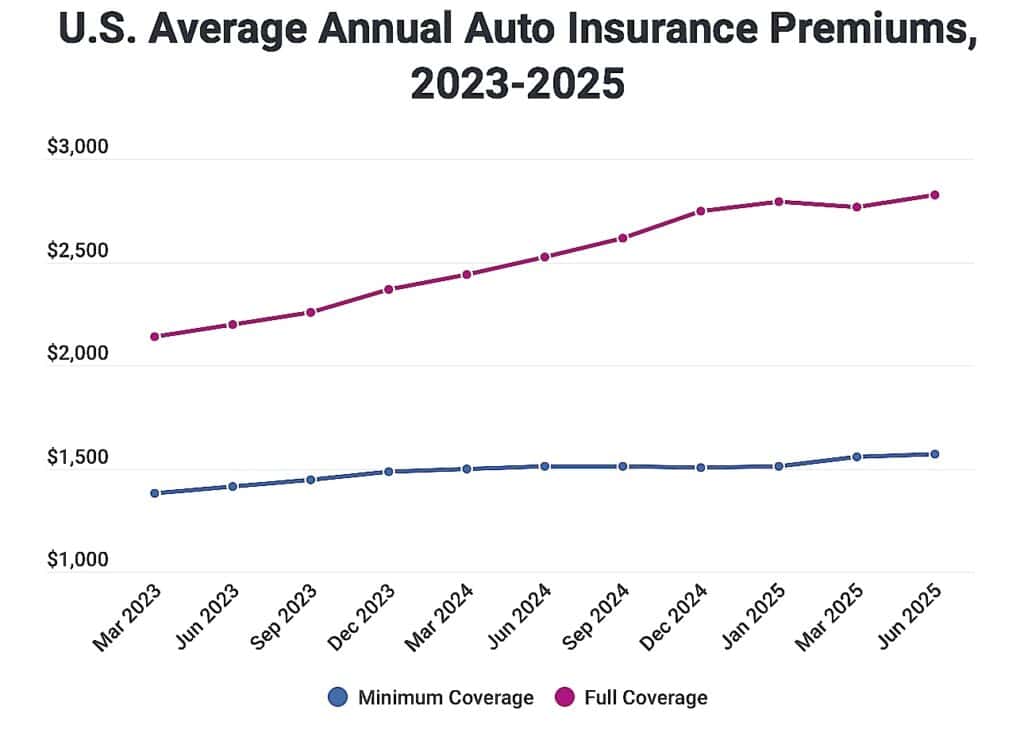

According to Experian data, the national average cost of full-coverage car insurance stands at about $2,894 per year, or roughly $241 per month, as of late 2025. For drivers carrying only state-minimum liability coverage, average annual premiums are lower, at approximately $1,548. These costs represent a meaningful expense for many households, especially as auto insurance premiums have risen steadily over the past several years.

Source: Experian

Insurance pricing also varies widely by location, making where you live nearly as important as how you drive. Differences at the state and ZIP-code level reflect a mix of regulatory requirements, weather-related risks, traffic density, claims frequency, legal environments, and the share of uninsured motorists, all of which influence how insurers set rates.

Most Expensive States for Auto Insurance

Nevada currently holds the distinction of having the nation’s highest car insurance costs. According to ValuePenguin’s 2025 state-by-state analysis, drivers in Nevada pay an average of about $286 per month for full-coverage auto insurance, placing it well above the national average. Florida ranks close behind, with average monthly premiums around $270, while Michigan remains among the most expensive states at roughly $260 per month for full coverage.

Several factors contribute to Nevada’s elevated insurance rates. The state has a high share of uninsured motorists, increasing costs for insured drivers. Heavy traffic congestion in the Las Vegas metro area, higher vehicle theft rates, and costly accident claims all add to insurer risk and push premiums higher.

Florida’s auto insurance costs have risen sharply in recent years. The state’s frequent exposure to hurricanes and severe weather leads to higher claim volumes and repair costs. Florida also has one of the highest uninsured motorist rates in the country, well above the national average, which forces insurers to spread additional risk across policyholders. A challenging legal and litigation environment further contributes to elevated premiums statewide.

Other states with consistently high auto insurance costs include New York, Louisiana, and California, where dense populations, higher repair expenses, elevated claim severity, and regulatory pressures combine to keep premiums above the national norm.

Most Affordable States for Coverage

On the opposite end of the cost spectrum, Vermont offers the lowest auto insurance rates in the nation. According to ValuePenguin’s 2025 data, drivers in Vermont pay an average of about $996 per year for full-coverage auto insurance, or roughly $83 per month. Maine ranks second, with average monthly premiums near $110, followed closely by New Hampshire at approximately $112 per month for full coverage.

Several factors help keep insurance costs low in these states. Lower population density results in fewer accidents and reduced claim frequency. Rural road networks experience far less congestion than major urban corridors, lowering collision risk. These states also face fewer costly natural disasters than hurricane- or tornado-prone regions and maintain comparatively lower rates of uninsured motorists, reducing insurer exposure.

Other states that consistently rank among the most affordable for auto insurance include Idaho, Ohio, and North Dakota, where average full-coverage premiums remain well below the national average. The contrast is substantial: the difference between insuring a vehicle in Vermont versus Nevada exceeds $2,000 per year, underscoring how strongly location influences auto insurance costs.

Understanding Recent Premium Trends

Auto insurance rates have risen sharply in recent years, though the pace of increases has begun to moderate. National industry data shows that average U.S. auto insurance premiums increased by roughly 10%–12% in 2025 compared with 2024, marking a slowdown from the steeper double-digit jumps recorded throughout 2023 and much of 2024.

Rate changes have varied widely by state. Several states experienced increases exceeding 20% over certain periods, driven by local loss trends and regulatory timing rather than uniform national pressure. These increases reflect a combination of factors, including higher vehicle repair costs due to advanced electronics, rising medical expenses following accidents, more frequent and severe weather events, and insurers adjusting rates after years of underwriting losses.

Not all trends have moved higher. Louisiana, long among the most expensive states for auto insurance, has seen a notable shift in 2025. State regulators report more than 20 auto insurance rate decrease filings since January, reflecting improving claims trends and changing market conditions. This divergence highlights how regional factors and regulatory environments can significantly influence insurance pricing outcomes.

Proven Money-Saving Strategies

Regardless of location, several evidence-based strategies can significantly reduce auto insurance costs. The most effective is comparison shopping. Consumer research from NerdWallet shows that annual premiums for identical coverage can differ by thousands of dollars between insurers, largely due to differences in pricing models and risk assessment.

Because insurers evaluate drivers differently, the cheapest company for one policy type may not be the cheapest for another. Studies indicate that insurers offering the lowest full-coverage rates frequently do not offer the lowest minimum-coverage rates in the same ZIP codes, making it essential to compare quotes for the exact coverage you need.

Shopping activity has increased in recent years. Data shows that about 14% of U.S. drivers shopped for auto insurance in early 2025, near historical highs. However, switching rates remained much lower, just over 4%, suggesting many drivers compare prices but do not ultimately change insurers, potentially missing savings.

Industry guidance generally recommends obtaining quotes from three to five insurers. Online comparison tools simplify the process, while independent agents can also help by quoting multiple carriers at once.

Additional cost-saving strategies include bundling auto insurance with homeowners or renters coverage, which commonly produces average discounts in the 7% to 10% range. Raising deductibles, such as increasing from $500 to $1,000, typically lowers premiums but requires sufficient savings to cover higher out-of-pocket costs after a claim.

Credit-based insurance scores influence pricing in most states. Insurers are permitted to use credit information in the majority of U.S. states, while California, Hawaii, Massachusetts, and Michigan restrict or prohibit this practice.

Finally, many insurers offer defensive driving discounts, often up to 10%, for completing approved courses. These programs can reduce premiums and help drivers avoid violations that lead to higher future rates.

Coverage Considerations

While pursuing lower rates makes financial sense, drivers must balance affordability with adequate protection. State minimum coverage requirements vary widely and are generally designed to meet legal standards rather than fully protect drivers in serious accidents. Most states require bodily injury and property damage liability insurance, with common minimums expressed as 25/50/25, meaning $25,000 per person for injuries, $50,000 per accident, and $25,000 for property damage.

These minimum limits often fall short in real-world scenarios. Industry claims data shows that average bodily injury claim severity rose by roughly 40% between 2018 and 2022, while property damage claim severity increased by nearly 50% over the same period. As medical costs, vehicle repair expenses, and labor rates continue to rise, a single serious accident can easily exceed state-mandated limits, leaving the at-fault driver personally responsible for uncovered costs.

Full coverage policies, which typically include comprehensive and collision coverage in addition to liability, cost more but provide broader financial protection. The choice between minimum and full coverage depends largely on vehicle value and personal financial risk tolerance. For older vehicles with low market value, maintaining comprehensive and collision coverage may not be cost-effective, since payouts are limited to the vehicle’s actual cash value.

The Impact of State Regulations

State insurance regulations play a major role in how auto insurance is priced. Some states, including California, impose strict rules on underwriting. These rules limit or prohibit the use of factors such as credit history, employment status, or prior insurance coverage when setting rates. Other states allow insurers broader discretion, leading to wider pricing variation across drivers.

No-fault insurance systems also affect costs. In no-fault states, drivers generally file injury claims with their own insurers regardless of fault, which requires Personal Injury Protection (PIP) coverage. PIP adds to baseline premiums and helps explain why many no-fault states tend to have higher average insurance costs. States operating under full or modified no-fault frameworks include Michigan, Florida, and New Jersey, consistently among the more expensive markets for coverage.

Regulatory oversight of rate increases varies by state as well. Insurers must file rate change requests with state insurance regulators, who can approve, reject, or modify proposed adjustments. This review process influences how quickly rising repair costs, medical expenses, and claims trends are reflected in premiums. In 2025, some states experienced modest rate relief as insurers sought decreases after several years of sharp increases, while others continued to see upward pricing pressure due to persistent claims severity and loss trends.

Looking Ahead

Auto insurance pricing is expected to remain uneven through 2026. While the pace of premium increases has slowed compared with the sharp spikes seen in 2023 and early 2024, pricing pressure has not disappeared. Rate trends will continue to vary significantly by state and insurer based on local claims experience, regulation, and cost dynamics.

Higher vehicle repair costs remain a key risk. Ongoing increases in labor rates, parts prices, and potential trade-related pressures on imported components could contribute to renewed upward pressure on premiums in some markets. At the same time, improving underwriting results and stronger insurer profitability have allowed certain carriers to file for rate reductions or compete more aggressively on price in select states.

For consumers, the most effective strategy remains active monitoring of local market conditions and regular comparison shopping, ideally at every policy renewal. While geographic differences in insurance costs are substantial and largely outside a driver’s control, maintaining a clean driving record, managing credit responsibly where permitted, and choosing coverage levels that balance protection and affordability can meaningfully reduce overall costs. In a market where location sets the baseline, focusing on controllable factors is essential to securing the best available rate.