The US Coffee Shop Landscape: Saturation or Strategic Opportunity?

The September 2025 Starbucks decision to close roughly 1% of its North American company-operated stores is not evidence of collapsing demand, it’s part of a US$1 billion restructuring plan that removes underperformers, retires weak formats, and redirects capital into more than 1,000 planned remodels in the next year. Starbucks will still end the fiscal year with nearly 18,300 stores and expects net new growth to resume in 2026, signaling that the broader U.S. coffee market remains healthy. For prospective café owners, the closures highlight lessons around location quality, operational discipline, and shifting consumer preferences rather than any downturn in long-term opportunity.

- Starbucks’ targeted closures, especially ~90 underperforming pickup-only stores, reflect strategic pruning, not reduced nationwide demand; the company still generated $36.2B in FY2024 revenue.

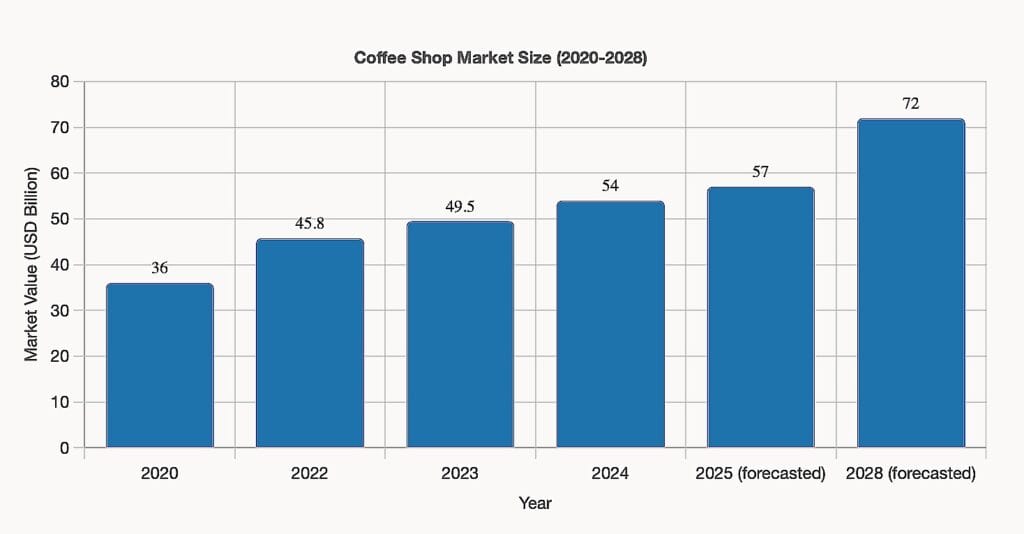

- The U.S. branded coffee shop market is valued around $49.5B–$54B and is forecast to reach $62B–$72B by 2028, supported by daily coffee consumption from roughly 66–67% of adults.

- Independent café profitability typically ranges 10%–20% net margins, with beverage gross margins around 75%–80%; achieving this depends heavily on labor control, rent discipline, and location fit.

- Generational demand, especially Gen Z and Millennials, favors specialty drinks, cold formats, ethical sourcing, plant-based options, and digital ordering, aligning with the fastest-growing segments of the market.

- Failure rates remain high (30%–80%), mostly tied to undercapitalization, weak operational planning, or poor site selection; operators should plan for $100K–$200K startup costs and 18–36 months to break even.

When Starbucks announced in September 2025 that it would close about 1% of its North American company-operated stores, a reduction amounting to roughly 400 or more locations based on the company’s filings and media reports, the news immediately drew industry attention. Many headlines framed it as a sign of weakening demand or an oversaturated market. But the facts tell a more complex story.

Starbucks described the closures as part of a broader restructuring plan that includes US$1 billion in related costs, selective removal of underperforming locations, and a reinvestment strategy to redesign and upgrade more than 1,000 stores over the following year. Understanding this context is essential for anyone evaluating the café opportunity in 2025.

Decoding the Starbucks Closures

The Starbucks closures deserve careful examination because they reveal important dynamics about the current coffee shop landscape. CEO Brian Niccol, who took over in September 2024, initiated these closures as part of his Back to Starbucks restructuring plan. The company explained that it would close stores “unable to create the physical environment our customers and partners expect, or where we don’t see a path to financial performance.”

This was not a broad retreat from the market. Starbucks said it would finish the fiscal year with nearly 18,300 North American stores, still one of the largest footprints in the industry. The company also made clear that net store growth will resume in fiscal 2026, alongside a plan to remodel more than 1,000 stores over the next year.

What drove specific closures varies by location. Starbucks confirmed it was shutting down about 90 mobile-order and pickup-only stores across 23 states, an experimental format that underperformed expectations. Other closures occurred in areas where pandemic-era migration permanently reduced foot traffic, especially in dense urban markets. These factors reflect operational and location-specific challenges rather than a demand collapse.

Starbucks also faced internal performance issues. North American comparable-store sales fell 2% in fiscal 2024, and leadership acknowledged the brand had drifted away from its core coffeehouse experience. The company noted that execution, customer experience, and operational consistency needed improvement.

Financially, Starbucks remains strong. The company generated $36.2 billion in revenue in fiscal 2024, maintaining its position as the world’s most profitable large coffee chain, even amid temporary restructuring. These metrics indicate a strategic correction, not an industry downturn.

The lesson for prospective café owners is nuanced. Starbucks’ closures reflect targeted adjustments, format missteps, and a strategic reset, not a weakening coffee market. At the same time, they highlight how crucial location quality, consistent operations, and evolving customer expectations are in today’s café environment.

The Market Reality: Growth Amid Evolution

While Starbucks has trimmed underperforming locations, the broader U.S. coffee shop market is still a growth story. Industry research from World Coffee Portal values the U.S. branded coffee shop market at about $49.5 billion with just over 40,000 outlets as of 2023–2024, roughly 4–7% above pre-pandemic levels, depending on the dataset. Estimates that include a wider mix of coffee shops peg 2024 revenue closer to $54 billion, with forecasts suggesting the market could reach roughly $62–72 billion by 2028, highlighting continued expansion rather than contraction.

Source: CoffeeDasher

As of late 2024, U.S. coffee chain sales grew about 8% year over year, led by large brands. Starbucks added nearly 500 net new U.S. stores in 2023, while Dunkin’ has continued to expand and Dutch Bros remains a smaller but fast-growing chain, underscoring that new and emerging brands can still scale in this environment.

Consumer demand is the engine behind this growth. The National Coffee Association’s 2024–2025 data show that roughly two-thirds of American adults (about 66–67%) drink coffee daily, and the average coffee drinker consumes around three cups per day. The market spans far beyond cafés to include at-home brewing, workplace coffee service, and ready-to-drink beverages, while the global coffee market overall is estimated at more than $260 billion annually.

The specialty segment is particularly strong. The U.S. specialty coffee market generated roughly $46–48 billion in revenue in 2024 and is projected to grow at about a 9.5–9.6% compound annual growth rate through 2030, driven by consumer interest in higher-quality, ethically sourced coffee and willingness to pay for differentiated experiences.

Behavior at the café level reinforces this momentum but also reveals limits. Survey data indicate that about 51% of people purchase coffee from a coffee shop at least once a week, and a majority of U.S. consumers keep their monthly café coffee spend relatively modest, often around $20 or less, signaling regular engagement with coffee shops alongside meaningful price sensitivity.

Profitability: The Make-or-Break Numbers

Understanding realistic profit expectations is essential before entering the coffee shop business. Industry data shows that most independent coffee shops operate with 10% to 20% net profit margins, with higher margins (15% to 25%) achievable only for well-run or high-volume locations.

For a small independent cafe generating $500,000 annually, a 15% margin equals $75,000 in profit before any owner salary. If the owner works in the business, their total compensation includes both profit and whatever wage they would otherwise pay a manager.

Profitability begins with strong gross margins. Multiple industry guides report 70% to 85% gross margins on beverage sales, placing the typical 75% to 80% range well within standard benchmarks. The profit per cup is also consistent with industry estimates: brewed coffee usually generates $1.50 to $2.50 in gross profit per cup, while specialty espresso drinks average $2.50 to $4.00.

The difference between high beverage gross margins and modest net profit margins reflects the real challenge. Labor, rent, utilities, insurance, and equipment quickly absorb the gap. Many operators use common benchmarks, labor at roughly 30% of revenue and rent below 15%, to maintain healthy margins, though actual percentages vary by market.

Location strongly affects these ratios. Prime areas may support higher revenue but come with higher rent, while neighborhood locations offer lower occupancy costs but may require stronger marketing and community engagement. Profitability ultimately depends on balancing foot traffic, pricing, and operating efficiency.

Startup costs also shape financial outcomes. Opening a coffee shop generally requires $100,000 to $200,000 for build-out, equipment, permits, inventory, and working capital, though some concepts cost more. Many shops reach break-even within 18 to 36 months, assuming solid management and a viable location.

Franchises offer different economics. According to Franchise Business Review, the average annual income for a coffee franchise owner after two years is about $116,000. Franchises benefit from brand systems and purchasing power, but operators pay royalties and fees that independents avoid. Beans & Brews Coffeehouse owners, for example, can achieve six-figure earnings when operating within the franchisor’s established model.

Consumer Trends Reshaping the Market

Several powerful trends are reshaping what successful coffee shops look like in 2025. One of the most significant is generational preference shifts. Generation Z (ages 18–24) and Millennials (ages 25–39) remain the primary growth engines of the specialty coffee sector. The 18–24 group held a 31.9% revenue share in 2024, while the 25–39 group is projected to grow fastest at 10.3% CAGR through 2030, according to Grand View Research’s specialty coffee market analysis.

These demographics favor independent cafes over chains, seek unique and Instagram-worthy experiences, prioritize sustainability and ethical sourcing, embrace plant-based options, and are heavy adopters of digital ordering and loyalty programs. Coffee shops that cater to these preferences can capture disproportionate share of this valuable segment.

The beverage mix is also evolving. While about 60% of adults 55 and older prefer hot coffee, younger drinkers lean toward cold formats; multiple surveys confirm that a majority of Gen Z coffee consumers prefer iced coffee. Cold brew, nitro coffee, and creative iced beverages are now essential menu items. The ready-to-drink coffee market reached tens of billions in 2024 and is expected to grow steadily through 2028.

Plant-based milk alternatives have shifted from accommodation to expectation. Almond, oat, and soy milk are standard choices, and around 50% of quick-service restaurants now offer plant-based options.

The “third place” concept, positioning the cafe as a community gathering spot between home and work, is also regaining importance. Starbucks’ renewed focus on this model reflects customer demand for comfortable seating, strong Wi-Fi, power access, and an environment suited for working or socializing.

Digital Integration: Essential Infrastructure

Technology has become non-negotiable infrastructure for coffee shop success. Digital ordering, through proprietary apps, in-store mobile ordering, or third-party platforms, can represent 30% to 40% of sales at leading operations. Loyalty programs drive repeat business, with engaged customers contributing a disproportionately high share of transactions.

However, digital integration comes with costs and trade-offs. Third-party delivery platforms typically charge 15% to 30% commissions, reducing profit margins on those orders. Building proprietary digital ordering systems requires technical expertise and ongoing maintenance, while cloud-based point-of-sale systems add monthly subscription fees.

The advantage of digital systems is significant for operators who implement them effectively. They enable detailed tracking of sales patterns, inventory management, labor optimization, and customer behavior analysis, allowing more informed decisions than traditional methods.

For smaller independent cafes, the challenge is accessing these technologies at reasonable cost. Some franchise systems provide digital infrastructure as part of their package, giving them an advantage over independent cafes that must build or buy these capabilities separately.

Competitive Dynamics and Market Concentration

Market concentration in coffee shops is significant but not overwhelming. Starbucks commands about 40% market share in US coffee shops, followed by Dunkin’ at roughly 25–26%, Dutch Bros at around 3%, and other chains and independents capturing the remaining 31% collectively. Starbucks operates over 16,000 US stores, while Dunkin’ has more than 9,000 locations and Dutch Bros has approximately 850–900 outlets.

Source: CoffeeDasher

This concentration means that the largest chains dominate prime locations, command significant marketing budgets, and achieve economies of scale that independents cannot match. However, the 31% share held by smaller chains and independents represents billions in revenue and demonstrates that alternatives to the giants can succeed.

Independent cafes succeed by differentiating on quality, experience, community connection, and specialty offerings that chains cannot easily replicate. The artisanal coffee movement, emphasizing craft roasting, ethical sourcing, distinctive flavor profiles, and barista expertise, has created space for independents to command premium prices and build loyal followings.

Geographic considerations matter enormously. The West region dominated the US specialty coffee market with approximately 25.8% revenue share in 2024, driven by cities like Seattle, Portland, and San Francisco that lead in coffee culture innovation. Meanwhile, the Southeast is projected to grow at the fastest rate of about 10% CAGR through 2030, suggesting opportunity in markets with developing coffee cultures.

The Failure Rate Reality

Coffee shop failure rates are sobering, estimates range from 30% to 80% depending on the source, timeframe, and whether the data refers to independent cafes or restaurants broadly. Most failures stem from three primary causes: overspending during startup, overestimating demand and underestimating competition, or lacking a solid business plan and operational expertise.

Overspending is particularly common because building an attractive cafe can quickly consume capital. Custom equipment, quality furnishings, sophisticated build-outs, and extensive inventory can push costs well beyond initial projections. Operators who reach break-even with insufficient capital to sustain operations until profitability arrives face serious financial pressure and a high risk of closure.

Overestimating demand reflects inadequate market research. A location that seems perfect may be surrounded by competitors, serve a demographic that doesn’t match the concept, or lack the foot traffic patterns assumed during planning. Thorough market analysis, including traffic counts, demographic studies, and competitive mapping, is essential but often skipped or done superficially.

Weak operational planning kills many cafes. Making great coffee is only one component of success. Managing inventory, scheduling labor, controlling costs, maintaining equipment, marketing effectively, and delivering consistent service require business skills that not all coffee enthusiasts possess.

Strategic Entry Points for 2025

For prospective cafe owners evaluating this market, several strategic considerations emerge from this analysis. First, saturation is market-specific rather than universal. Dense urban areas with multiple Starbucks locations per square mile present different dynamics than suburban neighborhoods or smaller cities where independent cafes can establish strong positions.

Second, differentiation is crucial. Simply opening another cafe serving standard espresso drinks in a competitive market is unlikely to succeed. Successful new entrants typically offer something distinctive: exceptional coffee quality, unique food pairings, compelling atmosphere, strong community connection, or specialized offerings like high-end pour-overs or coffee education.

Third, operational excellence from day one has become essential. Thin margins mean that cafes cannot afford extended learning curves. Operators without prior cafe management experience should seriously consider franchise options that provide training and systems, despite the additional costs.

Fourth, capital adequacy matters enormously. Plans should account for 18–36 months to profitability and include reserves for unexpected expenses. Undercapitalization is one of the most common failure causes and one of the most preventable.

Fifth, location selection requires sophisticated analysis. High-rent, high-traffic locations versus lower-rent neighborhood spots involve fundamentally different business models and risk profiles. The decision should be based on realistic revenue projections, not hope or intuition.

The Verdict: Opportunity Exists, But Standards Are High

The U.S. coffee shop market is not saturated to the point that opportunities have disappeared. The sector continues to grow, consumer demand remains strong, and new successful entrants are still emerging. At the same time, the bar for success has risen sharply. Competition is intense, operational requirements are demanding, margins are thin, and customers are more discerning than ever about quality, experience, and value.

The Starbucks closures in 2024–2025 illustrate this reality. They reflect targeted restructuring at underperforming locations within an otherwise healthy global brand, not a collapse in market demand. Starbucks’ shift toward improving in-store experience and scaling back formats that underperformed actually creates openings for independent cafés that prioritize atmosphere, service, and community connection.

For aspiring operators, the core question is not whether the market can support another coffee shop, but whether you can execute at a level that earns customer loyalty in a crowded field. That requires honest self-assessment, sufficient capital, rigorous market analysis, and realistic expectations about the operational complexity of running a café.

The coffee shop opportunity in 2025 is real, but only for those who approach it with preparation, discipline, and strategic clarity. Passion for coffee is not enough. Success requires business acumen, operational consistency, and a commitment to delivering an experience that stands out from the competition. Those who meet these standards can build profitable, enduring businesses. Those who do not will likely join the industry’s sobering failure statistics.

The decision, ultimately, is whether you have what it takes to be among the winners.