Cruise Lines vs. Casinos: Which Is The WORST Investment?

For investors choosing between cruise lines and casinos, both sectors promise excitement, but deliver volatility, debt, and disappointing returns. Cruise lines emerge as the weaker bet, narrowly, due to their extreme capital costs, pandemic exposure, and fragile operating model. Casinos fare slightly better thanks to diversified revenue and real estate value, but remain vulnerable to digital disruption and labor costs.

- Cruise lines’ debt burden: Major operators like Carnival and Royal Caribbean took on tens of billions in debt post-2020, leaving long-term solvency concerns.

- High capital intensity: New ships cost $800M–$1.5B each, with massive fixed expenses even when revenue collapses.

- Casinos’ structural edge: Casino assets retain real estate value and can adapt via online betting, unlike immobile cruise fleets.

- Digital disruption risk: Physical casinos face competition from online gambling and mobile betting platforms.

- Better alternatives: Consider gaming tech firms like Light & Wonder or travel giants Hilton and Marriott for diversified exposure.

For investors seeking thrills, both cruise lines and casinos promise excitement and the lure of big returns. The reality, however, is far less glamorous. Both industries are riddled with bankruptcies, mounting debt, and crushed investor hopes. From failed cruise operators to bankrupt casino empires, the track record is filled with spectacular financial collapses. If you’re deciding between these two gambling-adjacent sectors, you’re essentially choosing whether to risk your money on water or on land. But which one truly deserves the crown as the worse investment?

The Case Against Cruise Lines: Floating Money Pits

Cruise lines can produce impressive profits during boom times, but beneath the surface lies a deeply fragile business model. The industry’s capital intensity is immense, modern cruise ships cost between $800 million and $1.5 billion each to build, with operators constantly ordering new vessels to remain competitive. These floating resorts require continuous maintenance, crew staffing, and fuel, creating fixed costs that persist even when revenue collapses.

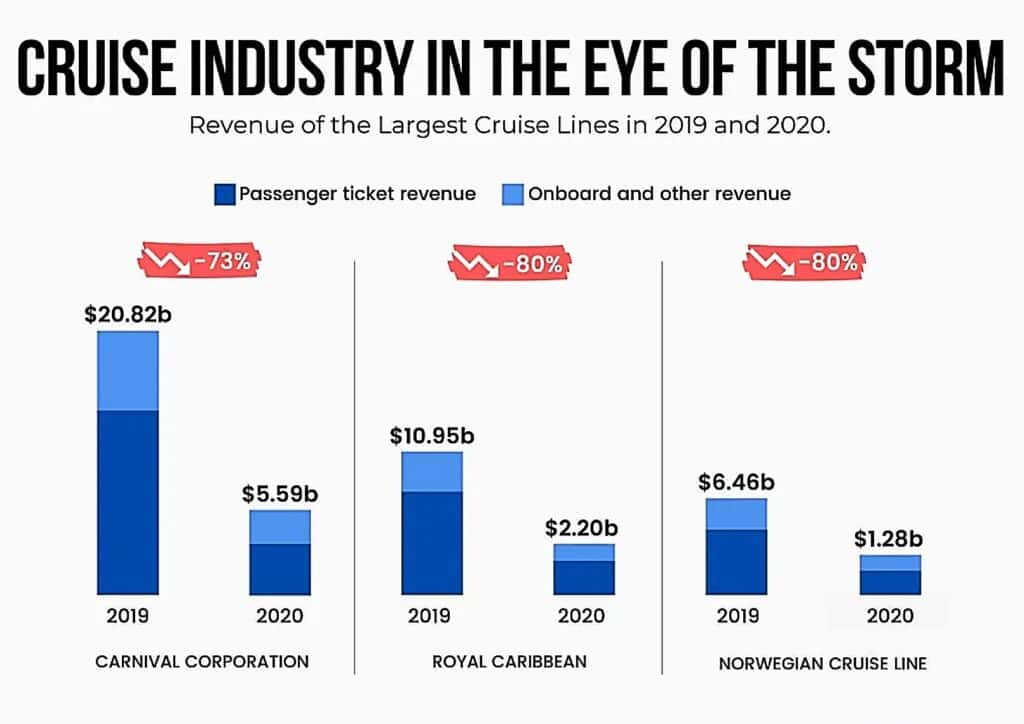

The COVID-19 pandemic exposed these vulnerabilities. Revenue for major operators plunged by 70–90%, forcing companies to take on billions in new debt just to survive. Several smaller lines, including Crystal Cruises and Cruise & Maritime Voyages, went bankrupt as global operations shut down for more than a year. Even giants like Carnival and Royal Caribbean narrowly avoided insolvency through massive capital raises and emergency liquidity measures.

Source: CompanyDebt

Operationally, cruise lines face endless risks, disease outbreaks, fuel price swings, hurricanes, geopolitical tensions, and shifting travel preferences. A single negative incident can devastate bookings for months. Despite strong demand, the industry suffers from limited pricing power, especially in the mass-market segment where travelers shop primarily on price. Discounting wars erode margins, leaving even record revenues struggling to offset enormous operating costs and debt loads.

In short, cruise lines may offer glamour and scale, but beneath the luxury veneer they remain among the most capital-intensive and vulnerable businesses in global travel, profitable in good years, perilously exposed in bad ones.

The Case Against Casinos: House Always Wins (Except When It Doesn’t)

On paper, casinos appear to be money-printing machines. The industry operates on the mathematical certainty of the house edge, every game is designed so that, over time, probability favors the casino. Yet history shows how fragile this business can be.

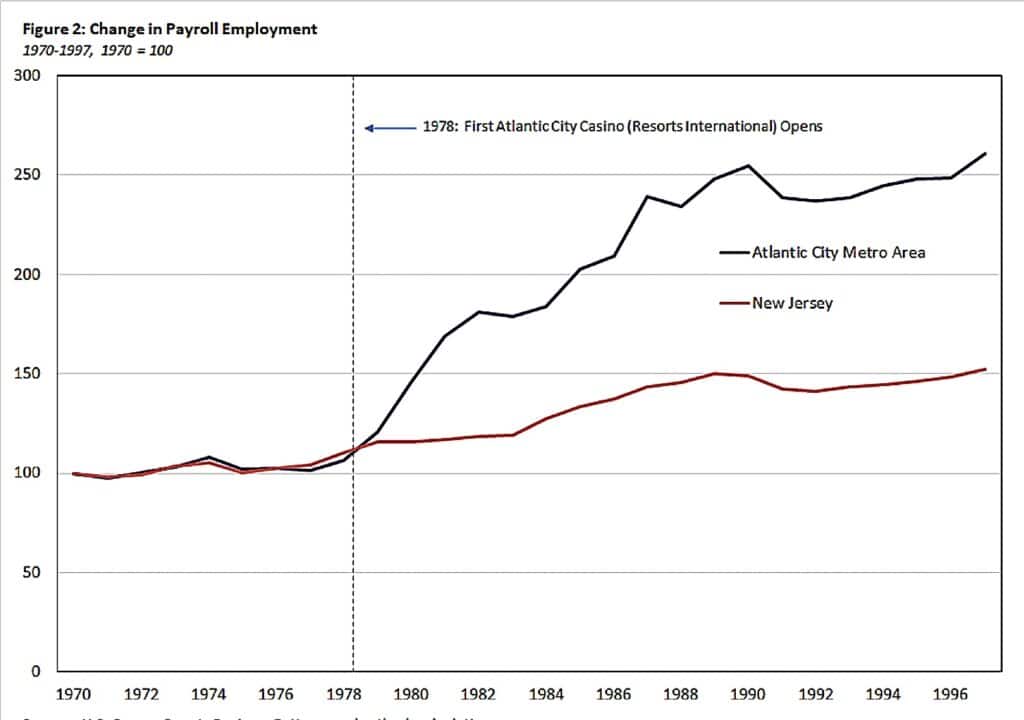

Atlantic City remains a cautionary tale. Once a booming gambling hub, it suffered a steep decline as neighboring states legalized casinos, eroding its customer base. Revenue peaked in 2006 and fell by nearly half within a decade, forcing multiple casino closures and leaving several properties vacant. Overexpansion, competition, and weak financial management crippled the market.

The downfall of Trump Entertainment Resorts exemplifies the dangers of excessive leverage. The company, which ran several Atlantic City casinos, filed for bankruptcy multiple times, in 2004, 2009, and 2014, after taking on high-interest debt to finance growth. Bondholders and contractors absorbed heavy losses while the properties struggled to stay afloat.

Today, regional casinos face similar pressures. As more states expand gaming markets, older venues lose their monopoly advantage. Meanwhile, online gambling and mobile sports betting have disrupted the traditional model, attracting younger gamblers who prefer the convenience of digital platforms. Physical casinos, burdened by high overhead, must now justify their existence against leaner, tech-driven competitors.

Source: Federal Reserve Bank Of Richmond

Labor challenges add further strain. Casinos require massive staffing to operate 24/7, and powerful unions in markets like Las Vegas and Atlantic City continue to drive up wages. Labor disputes and strikes have repeatedly halted operations, compounding financial losses.

Despite their built-in edge, casinos remain risky investments, capital-intensive, highly regulated, and increasingly vulnerable to digital disruption. The house may win the odds, but not always the market.

Critical Differences: Business Model Vulnerabilities

Both industries operate with high fixed costs and cyclical demand, but their weaknesses differ sharply. Cruise lines can redeploy ships to stronger regions if one market underperforms, while casinos are tied to immovable real estate assetsthat lose value when local economies falter.

Casinos have largely recovered post-pandemic, with many operators improving profit margins through cost efficiency and strong demand in entertainment and hospitality. Cruise lines, meanwhile, continue to rebuild from COVID-19’s shutdowns, burdened by heavy debt and lingering operational challenges despite rising bookings.

Casinos also enjoy diversified revenue streams beyond gambling, hotels, restaurants, events, and conventions now contribute significantly to income. Cruise lines, though offering onboard shopping and dining, remain dependent on consumer willingness to travel.

Source: Mordor Intelligence

However, casinos face a rising existential threat from online gambling, which erodes foot traffic and profits. Cruise lines don’t share this risk, you can gamble online from your couch, but you can’t replicate the cruise experience at home.

The Verdict: Cruise Lines Are Worse (By a Narrow Margin)

If forced to choose the weaker investment, cruise lines narrowly edge out casinos, but the margin is thin. The COVID-19 pandemic exposed just how vulnerable cruise operations can be. Global cruising came to a complete standstill for over a year, resulting in billions in losses and near-total revenue collapse. Casinos, while affected, largely remained operational, often shifting to limited-capacity or online formats rather than total shutdowns.

Cruise lines also face higher operational and reputational risk. A single ship outbreak or accident can dominate headlines worldwide, damaging the entire sector’s image. The industry remains vulnerable to disease transmission, mechanical failures, and environmental scrutiny, all of which add to costs and uncertainty.

The capital intensity of the cruise industry is another major weakness. Modern vessels often exceed $1 billion per ship, and maintaining a fleet creates massive fixed expenses. During the pandemic, the three largest cruise lines, Carnival Corporation, Royal Caribbean, and Norwegian Cruise Line Holdings, took on tens of billions in new debt to survive, leaving long-term solvency concerns.

Casinos, meanwhile, are not without risk. Regional markets such as Atlantic City have suffered waves of bankruptcies and closures due to market saturation and competition from neighboring states. Companies like Trump Entertainment Resorts filed for bankruptcy multiple times, erasing shareholder value. However, unlike cruise lines, casino assets, real estate, hotels, and resorts, retain some salvageable value even in downturns.

The Better Alternative: Avoid Both

Here’s the uncomfortable truth: both cruise lines and casinos are speculative investments unsuitable for most portfolios. Both have repeatedly destroyed shareholder value through poor management, excessive leverage, and extreme sensitivity to external shocks.

If you’re drawn to gaming and entertainment, consider companies that profit from gambling without running casinos. Light & Wonder and Evolution AB provide gaming technology and capture steady revenue without bearing operational risk.

Likewise, investors interested in travel and leisure should look to diversified hospitality firms like Marriott or Hilton, which spread risk across hotels, resorts, and attractions instead of relying on cruise demand.

For those seeking direct exposure, proceed cautiously. These are not long-term wealth builders but tactical trades for experienced investors who understand cycles and can endure volatility. Between the two, cruise lines remain slightly riskier due to their total shutdown during COVID and heavy debt. The smartest move is avoiding both.