How One Auto Accident Can Derail Your Wealth-Building Goals

Even one car accident can derail years of financial progress. Between medical bills, lost income, vehicle costs, and higher insurance premiums, a single crash can drain emergency funds and set back long-term wealth goals by five to ten years. With more than 15% of U.S. drivers uninsured, protecting yourself through stronger coverage and an emergency reserve is essential to preserving financial stability.

- Medical costs climb fast: Crash-related hospitalizations average $56,700 per patient, with serious injuries often exceeding $100,000.

- Hidden losses multiply: Lost wages, vehicle replacement, and rising premiums can add tens of thousands beyond medical expenses.

- Settlements fall short: Typical payouts range from $10,000–$50,000, often leaving victims responsible for major uncovered costs.

- Uninsured drivers increase risk: Over one in seven motorists lack insurance, exposing others to uncovered losses when accidents occur.

- Protect your wealth: Raise liability to at least $250K/$500K, add uninsured/underinsured motorist and umbrella coverage, and maintain an emergency fund for deductibles and gaps.

Most people know that auto accidents are expensive. What many may not realize is how deeply they can affect their financial future, especially for those focused on building and preserving wealth. A single crash can erase years of savings, create lasting debt, and delay important financial goals.

The True Cost of an Auto Accident

When people think about car accident costs, they typically imagine repair bills and maybe some medical expenses. The reality is far more complex and expensive.

According to the Centers for Disease Control and Prevention (CDC), the average medical cost for a crash-related injury treated in an emergency department is about $3,300, while hospitalization averages roughly $56,700 per patient. These expenses vary widely depending on the type and severity of the crash.

For serious injuries such as fractures, traumatic brain injuries, or spinal cord damage, total medical and rehabilitation costs can easily exceed $100,000, especially when intensive care, surgery, or long-term treatment is required, according to research from the National Library of Medicine.

These medical expenses represent only one part of the financial equation, as lost income, property damage, and long-term disabilities add substantial financial strain after a severe accident.

Beyond Medical Bills: The Hidden Costs

Lost Wages: When injuries keep you from working, the financial fallout can be immediate. Even moderate injuries can lead to weeks or months of missed income, draining emergency savings and disrupting long-term financial plans. The National Safety Council notes that lost productivity remains one of the largest economic impacts of crash-related injuries each year.

Vehicle Replacement: If your vehicle is totaled or requires major repairs, the costs can be devastating, especially if you’re underinsured or the at-fault driver lacks coverage. You may still owe on your auto loan while covering thousands in out-of-pocket expenses to replace or repair your car.

Increased Insurance Premiums: After an at-fault accident, car insurance rates often rise 20% to 50%, and the increase can last three to five years, according to the Insurance Information Institute (III). These higher premiums compound over time, adding thousands in additional costs.

Long-Term Care: Some crash injuries require years of physical therapy, medication, or assistive devices. The Centers for Disease Control and Prevention (CDC) reports that each hospitalization from a crash-related injury costs about $57,000 over a person’s lifetime, reflecting medical and ongoing rehabilitation expenses.

Diminished Earning Capacity: Severe injuries can permanently affect your ability to work or perform in your previous role. Many victims must change careers or accept reduced wages, leading to a lasting decline in lifetime income potential.

The Settlement Reality

Many people assume that if the accident wasn’t their fault, insurance will cover everything. Unfortunately, that’s rarely the case.

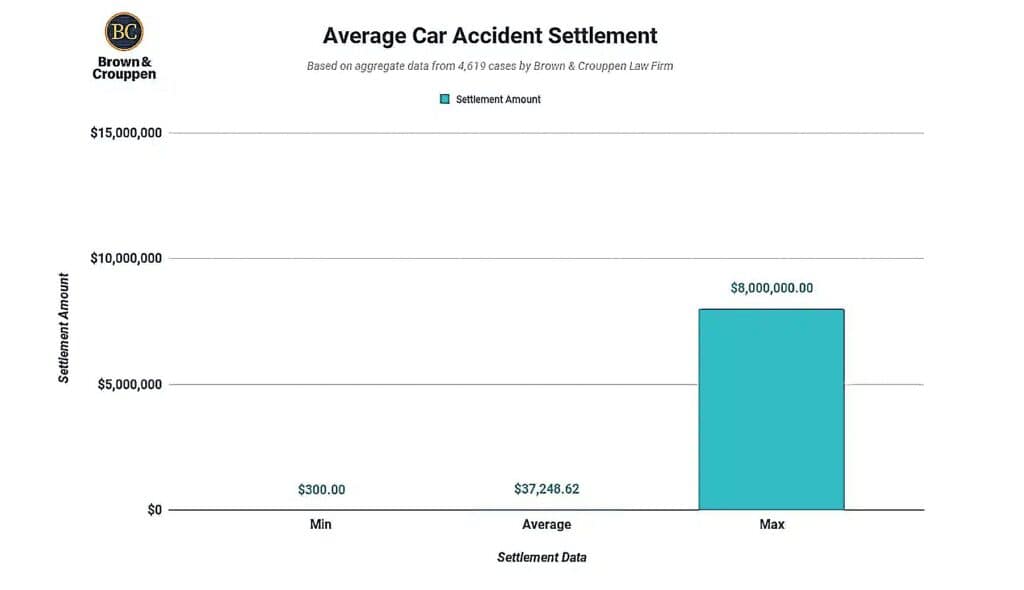

The average car accident settlement is around $37,000, according to nationwide data from over 4,500 cases compiled by Brown & Crouppen, though outcomes vary widely based on injury type and circumstances.

Source: Brown & Crouppen

For minor injuries, such as soft-tissue damage requiring a few medical visits, settlements typically range from $10,000 to $15,000, based on analysis by TorHoerman Law. Cases involving moderate injuries like fractures or mild head trauma generally fall between $20,000 and $50,000.

However, these settlements must cover all expenses, medical bills, lost wages, property damage, and pain and suffering. If total damages exceed the payout, the injured party is responsible for the remainder. This gap often leaves victims financially strained despite receiving a settlement.

The Uninsured and Underinsured Driver Problem

Perhaps the biggest financial threat on the road comes from drivers who lack adequate insurance. In 2023, an estimated 15.4% of U.S. motorists, more than one in seven, were uninsured, according to the Insurance Research Council (IRC). Even more concerning, roughly 33.4% of drivers were either uninsured or underinsured, marking a 10-percentage-point increase since 2017 for the combined rate, as noted by the Insurance Information Institute.

What does this mean practically? If you’re hit by an uninsured driver and face $50,000 in medical bills and lost wages, that money has to come from somewhere. Without sufficient uninsured/underinsured motorist coverage on your own policy, you could be forced to pay out-of-pocket, drain savings, or go into debt.

Many drivers carry only state-minimum liability limits, which remain shockingly low in most states, often just $25,000 to $50,000 per accident. These outdated limits haven’t kept pace with rising medical and repair costs, leaving victims exposed to massive financial shortfalls after serious crashes.

How Accidents Derail Wealth-Building

Sarah, 35, has been diligently saving for retirement. She has $40,000 in her emergency fund and contributes $500 per month to her retirement account. She’s on track to retire comfortably.

Then she’s rear-ended by an underinsured driver. She suffers a herniated disc requiring surgery. Her medical bills total $85,000. She misses four months of work, losing $20,000 in income. The at-fault driver carries only $25,000 in liability coverage.

Her health insurance covers part of the costs after she meets a $5,000 deductible, but she’s still responsible for $25,000 in out-of-pocket medical expenses and $5,000 in rehabilitation, travel, and uncovered therapy costs. Combined with her $20,000 lost income, Sarah faces a $50,000 total financial hit.

She’s forced to:

-

Drain her entire emergency fund ($40,000)

-

Borrow $10,000 from family

-

Stop retirement contributions for two years while rebuilding her savings

-

Deal with higher insurance premiums for the next five years

The total financial impact adds up quickly:

-

$40,000 savings drained

-

$12,000 in missed retirement contributions ($500 × 24 months)

-

$3,000 in higher premiums over five years

-

And lingering debt until the family loan is repaid

In total, she’s lost or delayed over $55,000 in net worth, not counting lost investment growth. Her wealth-building timeline is set back seven to ten years, assuming she eventually recovers and returns to her previous income level, which isn’t always guaranteed.

Protecting Your Wealth from Accident Devastation

The good news is that you can protect yourself with proper insurance coverage:

Increase Liability Limits: Don’t settle for state minimums. Carry at least $250,000/$500,000 in liability coverage to protect your assets if you cause an accident.

Add Uninsured/Underinsured Motorist Coverage: This is arguably the most important coverage for protecting your wealth. It covers your medical bills and lost wages when the at-fault driver lacks adequate insurance. In 21 states and Washington D.C., this coverage is mandatory, but it’s optional in others.

Consider Umbrella Insurance: For an additional $150 to $300 annually, an umbrella policy provides $1 million or more in liability coverage above your auto and home insurance limits. This protects your assets from lawsuits following a serious accident.

Maintain Adequate Medical Payments or PIP Coverage: These coverages pay your medical bills regardless of fault, providing immediate financial relief after an accident.

Build and Maintain an Emergency Fund: Even with good insurance, you may face deductibles and coverage gaps. An emergency fund of three to six months of expenses provides a buffer.

The Bottom Line

A single car accident can erase years of financial progress. Medical bills, lost income, vehicle replacement costs, and higher premiums can quickly drain savings and disrupt long-term goals. Even one serious crash can set back wealth-building by several years.

The financial risk is heightened by the large number of uninsured and underinsured drivers, leaving many people to cover major losses on their own. With medical costs and settlements reaching tens of thousands of dollars, being underinsured can have devastating consequences.

For a modest increase in annual premiums, you can significantly strengthen your protection. Review your policy to ensure you have sufficient liability limits, uninsured and underinsured motorist coverage, and consider adding an umbrella policy. Safeguarding your wealth today is far less costly than rebuilding it after a single accident.