Yes, You Can Borrow Money From Your 401(k): Here’s How It Works

Borrowing from your 401(k) can offer fast, low-rate relief during a financial emergency, but it carries long-term costs. While you’re technically paying yourself back with interest, a 401(k) loan can shrink your retirement growth, create tax liabilities if you leave your job, and lead to missed employer matches. It’s best viewed as a last resort, not a first-line option, after exploring emergency savings, personal loans, or 0% APR credit cards.

- Loan limits: The IRS caps 401(k) loans at the lesser of 50% of your vested balance or $50,000, typically repaid over five years via payroll deductions.

- Interest rate (2025): Around 9–10%, based on prime +1–2%, but repaid interest goes back into your account, not to a bank.

- Key risk: Job loss triggers repayment within 60–90 days; failure to repay means taxes and a 10% early-withdrawal penalty if under age 59½.

- Hidden costs: Lost investment growth, double taxation (repaying with after-tax dollars), and missing out on employer match contributions.

- When it makes sense: To prevent foreclosure or bankruptcy, or consolidate high-interest debt, with strong job security and disciplined repayment.

When your HVAC system dies in the middle of summer or an unexpected medical bill hits, the expense can feel overwhelming. If your emergency fund falls short and personal loan rates hover around 12%, you might start eyeing an alternative you’ve only heard coworkers mention, borrowing from your 401(k). It sounds simple: tapping your own savings for quick relief. But before treating your retirement account as a financial safety net, it’s worth asking, is a 401(k) loan really a smart move?

What Is a 401(k) Loan?

A 401(k) loan lets you borrow money directly from your own retirement savings and pay it back, with interest, into your account. In simple terms, it’s like becoming your own lender, using your retirement balance as collateral.

Not every employer offers this option, but it’s widely available. According to the latest data from the Investment Company Institute (ICI) 84% of employer-sponsored 401(k) plans include a loan provision. You’ll need to check with your plan administrator to confirm if your plan allows loans and what limits apply. The application process is typically fast, often completed within a few business days depending on your provider.

A 401(k) loan differs significantly from a hardship withdrawal. With a hardship withdrawal, you permanently remove money from your account, owe income taxes on the withdrawn amount, and may face a 10% early-withdrawal penaltyif you’re under age 59½. With a loan, the funds stay within your plan ecosystem, you repay the borrowed amount over time, and the interest goes back into your own account.

However, if you fail to repay as required or leave your job before the loan is repaid, the outstanding balance may be treated as a taxable distribution, potentially triggering penalties.

The Rules

The IRS sets clear limits on 401(k) loans. You can borrow the lesser of $50,000 or 50% of your vested account balance. If you have $80,000 vested, you can access $40,000; if your balance is $120,000, your limit is $50,000.

Repayment rules are equally strict. Most loans must be repaid within five years using substantially level paymentsmade at least quarterly, typically through automatic payroll deductions. If the money is used to purchase your primary residence, your plan may allow a longer repayment term, though the IRS doesn’t set a specific maximum period.

Interest rates must be “reasonable,” often based on the prime rate plus 1–2 percentage points. As of late 2024, that means roughly 9–10%, depending on your plan’s terms. The upside is that you pay the interest back to your own 401(k), not to a lender, so the money continues benefiting your retirement savings.

The application process is simple. Log into your plan’s online portal, choose the loan option, enter the amount and reason, review the terms, and e-sign the agreement. Funds usually arrive in a few business days, though processing times vary by provider.

Most employers limit the number of loans you can have open, often one or two at a time. However, not all 401(k) plans permit loans, so confirm eligibility with your plan administrator before applying.

Why People Do It

The appeal of a 401(k) loan is undeniable when you’re facing a financial emergency. There’s no credit check required because you’re borrowing your own money, not applying with a lender. That makes it attractive for people with limited or damaged credit who might otherwise face high-interest rates.

The interest rate advantage is another key factor. Most plans charge the prime rate plus 1–2%, typically around 8–10% in late 2024. By comparison, personal loans average about 11–12%, and credit cards often exceed 20%. Since the interest goes back into your own account, it feels like a better deal than paying a bank.

Speed also matters. Unlike traditional loans that take weeks to process, 401(k) loans are often approved online and funded within a few business days. Many people use them for debt consolidation, medical bills, home repairs, or other urgent needs. In these situations, tapping a 401(k) can feel like a quick financial lifeline, though it’s important to remember it also comes with long-term trade-offs.

The Risks

But here’s where things get treacherous, and why financial advisors typically cringe when this topic arises.

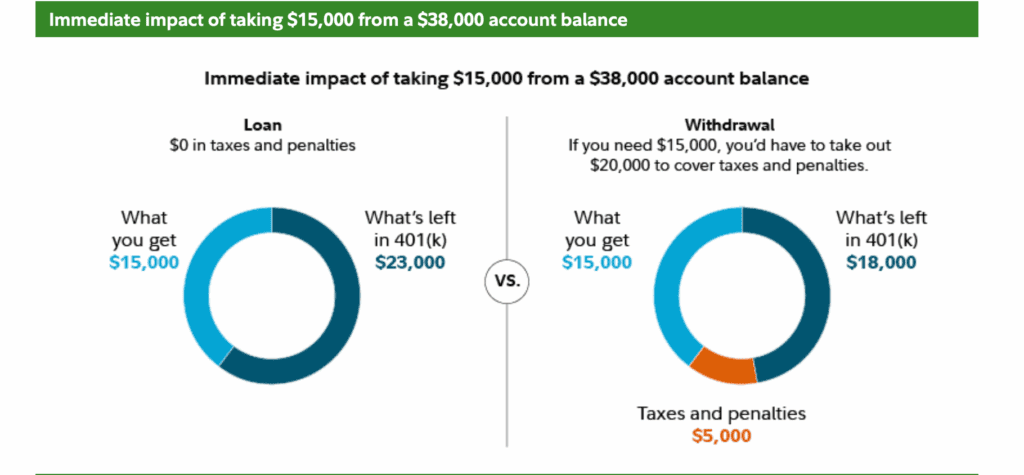

The job loss trap is the biggest danger. If you leave your employer, whether voluntarily or not, most plans require full repayment within 60 to 90 days. Miss that deadline, and the outstanding balance becomes a taxable distribution. You’ll owe income tax on the entire amount, plus a 10% early withdrawal penalty if you’re under 59½. A $30,000 loan could suddenly trigger a $10,000+ tax bill when you can least afford it. Under current rules, some plans allow repayment until your tax-filing deadline, but this varies by employer according to IRS 401(k) loan guidelines.

Source: Fidelity

Opportunity cost compounds quietly. Every dollar you borrow stops growing. If you borrow $20,000 and take five years to repay it, you could miss out on $8,000 to $12,000 in potential gains, assuming a 7% annual return. While you’re paying yourself interest, typically around 8–10%, the market historically delivers higher returns, making it a trade-off that reduces long-term growth.

Double taxation adds another hidden cost. You repay your 401(k) loan with after-tax dollars from your paycheck, and when you withdraw that money in retirement, it’s taxed again as ordinary income. Those same dollars end up being taxed twice, cutting deeper into your savings due to 401(k) loan taxation rules.

Lost employer match can quietly drain your balance. Many people reduce or pause 401(k) contributions while repaying a loan, thinking they can’t afford both. But if your employer matches contributions, you’re giving up free money. A 50% match on 6% of your salary means losing about $3,000 a year, often more than the loan’s total interest cost, as noted in Fidelity’s guidance on 401(k) loan repayment.

When It Makes Sense

Despite the risks, certain situations can justify taking a 401(k) loan.

Preventing bankruptcy or foreclosure. If you’re facing financial catastrophe and have exhausted all other options, a 401(k) loan may be the least-bad choice. Bankruptcy can damage your credit for up to ten years, while foreclosure costs you your home. In such cases, tapping your retirement savings might be preferable to losing everything.

Consolidating high-interest debt, with discipline. If you’re carrying $15,000 in credit card debt at 24% interest and can’t qualify for a balance transfer card or personal loan, borrowing from your 401(k) at around 9% could save you hundreds each month. The key is strict discipline, close or stop using your cards. Otherwise, you’ll add new debt while draining your retirement.

Emergency expenses with job stability. When you need funds for a medical procedure or urgent repair, have strong job security, and can repay the loan within a few years while continuing regular contributions, the math may work in your favor.

Decision framework checklist:

- Have you used your emergency fund?

- Explored 0% credit cards, personal loans, or home-equity options?

- Is your job secure?

- Can you repay the loan in three to five years?

- Can you keep contributing to your 401(k) during repayment?

- Is the alternative more harmful or costly?

If you answered “yes” to all, a 401(k) loan may be appropriate. Always review your plan’s terms and IRS loan rules before borrowing.

Better Alternatives to Try First

Before tapping your 401(k), explore safer and more cost-effective options. Start by building a small emergency fund, even $1,000 can help you handle minor expenses without touching retirement savings. Many medical providers and contractors offer payment plans with zero interest, making large bills easier to manage. A 0% introductory APR credit card can provide 12–18 months of interest-free payments if you qualify and repay on time.

Personal loans from credit unions often feature lower rates and better terms than most banks. If you’re a homeowner, a home equity line of credit (HELOC) can offer lower borrowing costs and potential tax benefits when used for home improvements. Explore community assistance programs that help with medical bills, utilities, or rent, and don’t hesitate to negotiate with creditors, many will reduce balances or create payment plans to prevent defaults.

Conclusion

Borrowing from your 401(k) isn’t inherently good or bad, it’s a financial tool with very specific use cases and real consequences. It can provide quick relief in a true emergency or help you avoid bankruptcy, but it also puts your long-term retirement growth at risk. If your job security is uncertain or your repayment plan isn’t solid, the short-term fix can become a lasting setback.

Your 401(k) is meant to fund your future, not patch today’s problems. Exhaust safer alternatives first, emergency savings, low-interest loans, or payment plans, before dipping into your retirement. And if you do borrow, commit to repaying on time and continuing regular contributions. The best outcome is one where you solve today’s problem without shortchanging tomorrow.