The AI Investment Paradox: Why Companies Spending $400 Billion Still Can’t Turn a Profit

The Numbers That Don’t Add Up

The spending is historic by any measure. Tech giants are projected to spend around $400 billion in 2025 on infrastructure to train and operate AI models, more than the inflation-adjusted cost of putting America on the moon. Except the Apollo program was a decade-long effort; the AI buildout is happening every year, not once a decade.

Source: IEEE

Global AI spending is expected to reach $375 billion in 2025 and $500 billion by 2026, according to UBS estimates. The scale is staggering, and it’s already shaping macro trends: Goldman Sachs analysts estimate AI-related capital expenditures added roughly 1 percentage point to U.S. GDP growth in the first half of 2025, placing it alongside consumer spending as a top economic driver.

But here’s the problem, revenue isn’t keeping up with investment. OpenAI reported $4.3 billion in revenue in the first half of 2025, but also posted an estimated $7–8 billion loss for the same period. Internal projections reviewed by The Information suggest cumulative losses of about $44 billion through 2028, with profitability not expected until 2029.

Industry-wide, a Fortune analysis shows that to justify current AI investments, companies would need to generate roughly $40 billion in annual revenue, yet currently produce only $15–20 billion. That’s not a small gap, it’s a chasm.

Five Fault Lines

1. The Circular Money Dance

Perhaps nothing better illustrates bubble dynamics than the tangled web of investments propping up the AI ecosystem. OpenAI’s recent deal with AMD grants it warrants to acquire up to 160 million AMD shares, nearly a 10 percent potential stake, as part of a multi-year chip-supply partnership expected to scale to six gigawatts by 2026. Meanwhile, Nvidia and OpenAI announced a $100 billion strategic partnership to deploy 10 gigawatts of Nvidia systems. Add to that Microsoft’s dual role as OpenAI’s largest investor and cloud partner, plus Nvidia’s equity stake in CoreWeave, itself a key supplier of Microsoft’s AI compute, and the money starts to loop in circles. Investment analysts are flagging these “round-trip” flows as early warning signs of bubble-like behavior.

2. The Profitability Desert

Inside Big Tech, cost pressures are mounting. Firms are spending billions on compute and model training without clear revenue paths. A Massachusetts Institute of Technology study found that 95 percent of enterprise generative-AI pilots fail to deliver measurable profit impact. Gartner projects that roughly 30 percent of GenAI projects will be abandoned after proof-of-concept by 2025 due to poor ROI and unclear business value. The result: entire divisions burning cash with no sustainable model in sight.

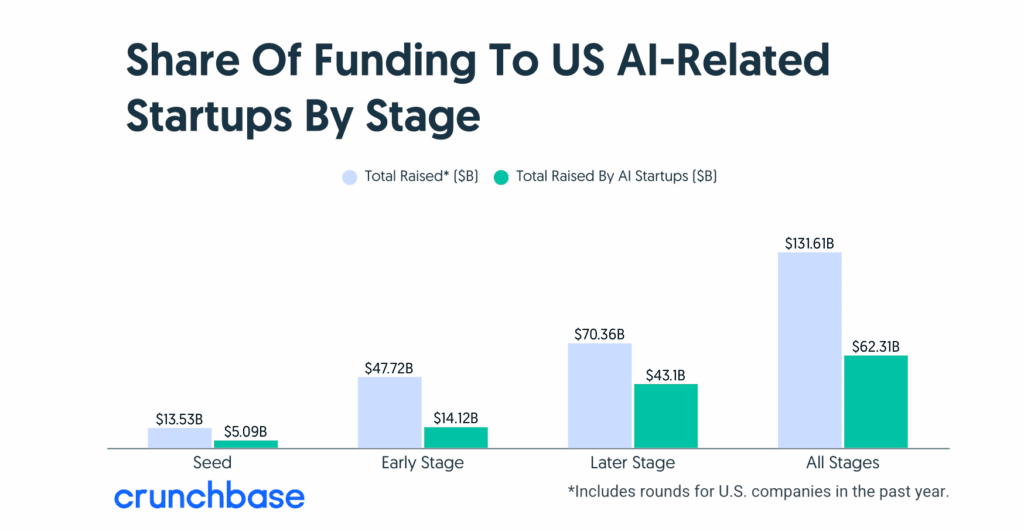

3. The Capital Concentration

AI startups continue to swallow venture capital at record pace. In the first half of 2025, they captured about 53 percent of global VC funding and roughly 64 percent of U.S. venture dollars. Yet the number of active venture funds keeps shrinking, with fewer firms writing bigger checks to fewer companies. According to Crunchbase, late-stage AI giants like Anthropic, OpenAI, and Databricks are capturing a disproportionate share of new money. This isn’t diversification. It’s groupthink at scale.

Source: Crunchbase

4. The Giant’s Shadow

Unlike the dot-com boom, when small startups blindsided incumbents, today’s tech giants are playing offense. Meta, Google, and Microsoft can bankroll AI losses indefinitely using profits from search, advertising, and cloud services. Smaller AI-first firms like OpenAI or Anthropic must monetize immediately or run out of runway. The giants’ ability to subsidize R&D gives them an enduring structural edge others simply can’t match.

5. The Valuation Fantasia

AI valuations have entered speculative territory. Across markets, share prices are increasingly driven by momentum rather than fundamentals. The rumored $2 billion raise for a stealth startup led by former OpenAI executives remains unverified, but it captures the sentiment: investors are funding promise over proof. Even long-term optimists like Jeff Bezos have cautioned that the sector shows signs of an “industrial-scale bubble”, with valuations increasingly detached from real earnings.

Why The Believers Might Be Right

Yet dismissing the current AI surge as pure speculation misses something crucial, the technology actually works. As Jeff Bezos put it, “AI is real, and it is going to change every industry.” Analysts at Forrester note that regardless of financial dynamics, adoption is rising fast, with consumers and enterprises actively using AI tools and integrating them into daily workflows.

This distinguishes AI from cryptocurrency’s empty promises or the metaverse’s corporate hype. ChatGPT now has around 700 million weekly users, and GitHub Copilot is writing code that developers rely on daily. AI systems are accelerating drug discovery, generating creative content, and automating critical business operations across industries from finance to healthcare.

Unlike the 1990s dot-com bubble driven by unprofitable startups, this year’s rally rests on robust earnings from mega-cap firms such as Microsoft, Google, and Meta, all profitable companies making calculated AI investments rather than speculative bets.

As Howard Marks of Oaktree Capital observes, “The main ingredient in bubbles is psychological excess, there’s no such thing as a price too high. And I don’t detect that level of mania at this time.” Meanwhile, former Intel CEO Pat Gelsinger agrees the market shows bubble traits but predicts it will last “several years” as transformative technologies mature through the decade.

The Correction Has Begun

The question isn’t whether there will be a reckoning, it’s already underway.

Meta’s 600 layoffs mark just one data point. Early indicators show that many AI startups are collapsing under unsustainable costs and weak product-market fit. Industry studies estimate that nearly 90% of AI startups fail, a rate on par or higher than general tech ventures due to high compute expenses and unclear paths to profitability. Venture capital has entered a selective phase, backing firms with proven traction rather than every startup with “AI” in its name.

Perhaps most tellingly, a PYMNTS Intelligence survey found that only 26.7% of CFOs plan to increase generative AI budgets in 2026, down sharply from 53.3% a year earlier. Enterprise checkbooks are tightening, signaling a cooling cycle after two years of exuberant spending.

Even OpenAI CEO Sam Altman admits the market is in a bubble, warning that “some AI startups and investors will get burned.” Yet he remains confident OpenAI can weather the storm, proof that even true believers now recognize the correction is already in motion.

What Comes Next

History offers a clear template. The railroad boom of the 1800s, the dot-com surge of the 1990s, and the broadband build-out of the early 2000s all followed the same arc, massive overinvestment, spectacular crashes, and eventual transformation. The question was never whether the technology mattered. It was who would survive to capture the lasting value.

As experts note, just like the 19th-century railroads and the 20th-century Internet build-out, artificial intelligence will rise first, crash second, and ultimately reshape the world.

Meta’s contradiction, cutting 600 jobs while pouring billions into AI infrastructure, isn’t confusion; it’s adaptation. The company is acknowledging that the current AI gold rush was poorly organized while doubling down on its belief that controlling the infrastructure means controlling the future.

For investors, the era of indiscriminate AI funding is over. For startups, survival now depends on actual revenue and clear differentiation, not pitch decks and hype. For Big Tech, the advantage compounds as capital requirements soar, only the giants can afford to keep playing.

And for the broader economy, when AI-related spending accounts for a meaningful share of GDP growth, a correction could have significant ripple effects. The AI bubble isn’t a hypothesis, it’s already here. The only question is how hard it deflates, and who’s still standing when it does.