The Rise of Equity Crowdfunding: How Main Street Can Now Invest in Startups

Since 2016, U.S. equity crowdfunding has transformed from a niche experiment into a $300M+ annual market, letting non-accredited investors buy startup shares under the Regulation Crowdfunding (Reg CF) and Regulation A+ frameworks created by the 2012 JOBS Act. Everyday Americans can now invest small amounts in private companies once reserved for venture capitalists, though risks remain high, exits rare, and liquidity limited.

- Access Expanded: The JOBS Act (Titles II, III, and IV) legalized online startup investing via platforms like Wefunder, StartEngine, and Republic, enabling both accredited and non-accredited participation since May 2016.

- Investor Limits: Non-accredited investors can contribute 5–10% of annual income or net worth (up to $124K/year), per Investor.gov guidelines. Reg CF caps company raises at $5M annually.

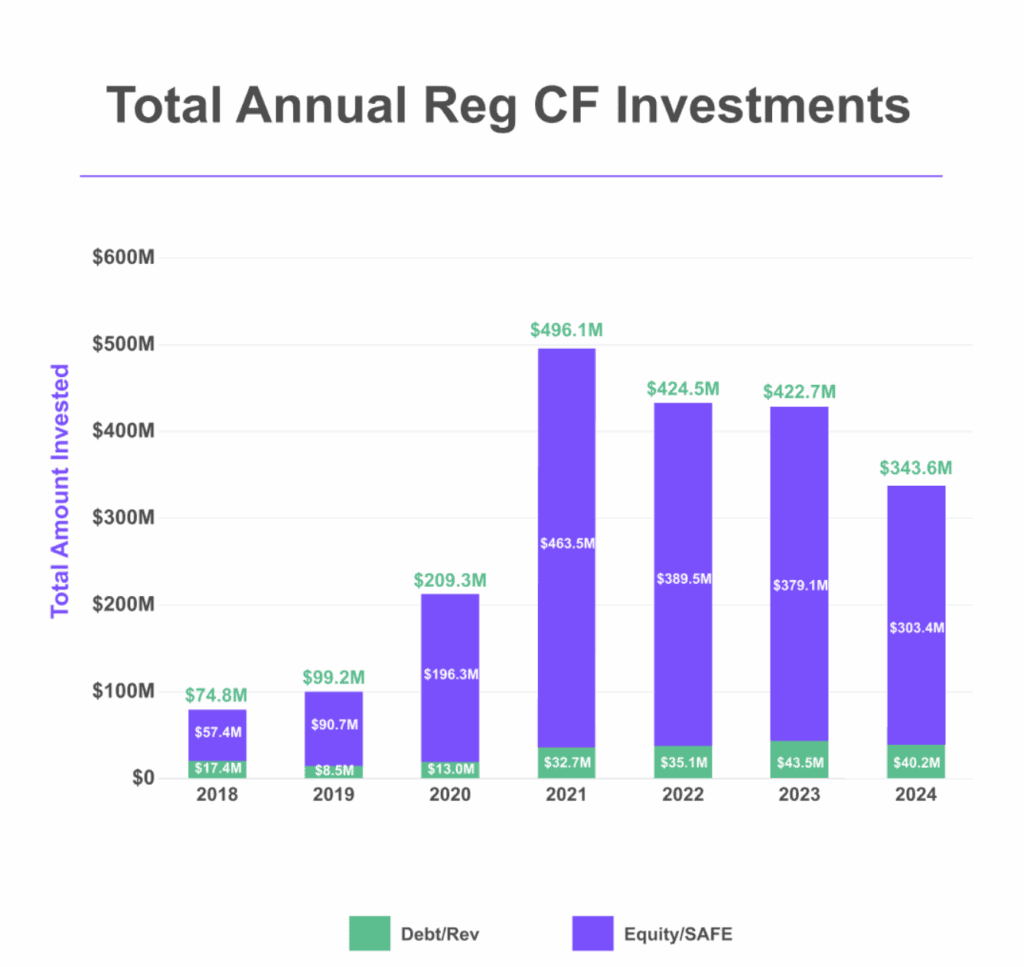

- Market Snapshot (2024): U.S. crowdfunding volume reached $343.6M (- 18% YoY), with average investments rising to $1.5K-$2.3K per deal (KingsCrowd, 2024).

- Key Risks: High failure rates (60–70%), multi-year illiquidity, and inflated valuations compared with venture capital averages (PitchBook, Q3 2024).

- Outlook: Tokenization and secondary markets like StartEngine Secondary aim to boost liquidity, while SEC and global regulators refine crowdfunding protections for 2025 and beyond.

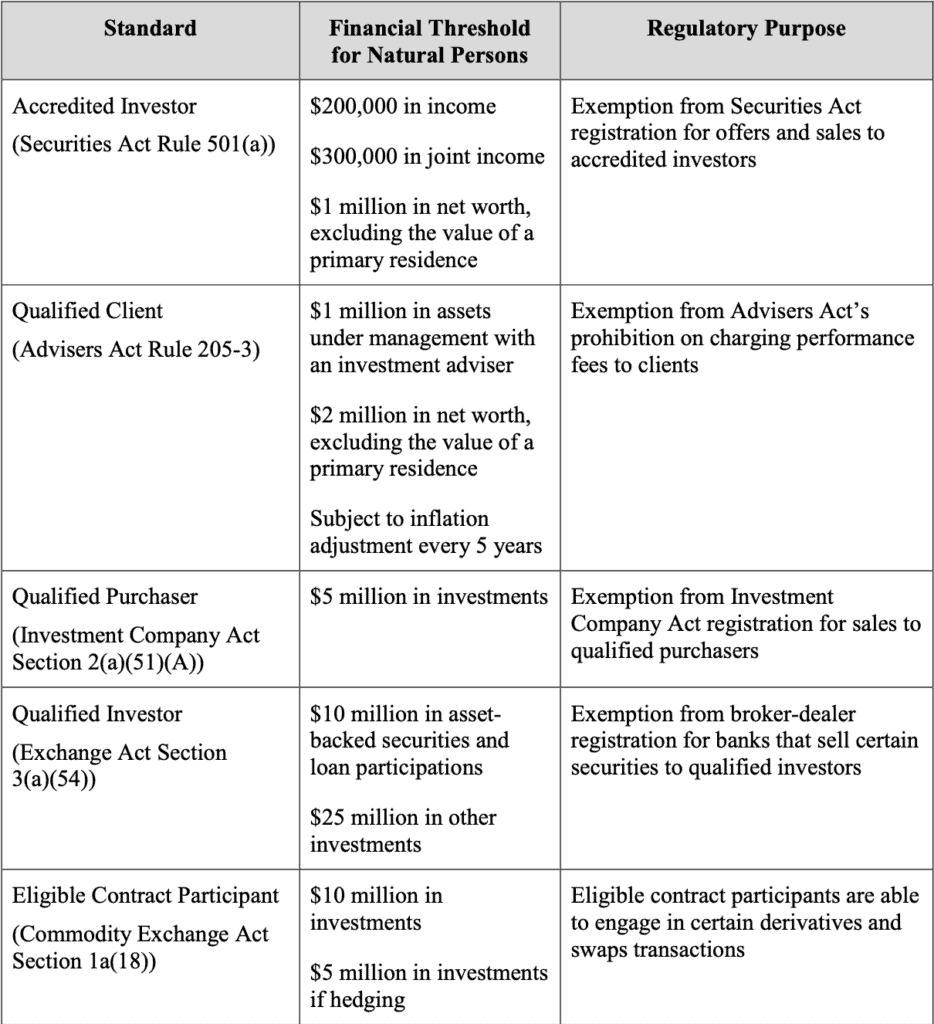

For decades, startup investing remained largely off-limits to everyday Americans. From the early 1980s until 2016, U.S. securities regulations restricted participation in private offerings to accredited investors, individuals earning over $200,000 annually ($300,000 jointly) or holding $1 million in net worth excluding their home.

Source: SEC

The Regulatory Framework: Understanding the JOBS Act

The JOBS Act consists of seven titles, but three in particular, Titles II, III, and IV, transformed the landscape of equity crowdfunding and startup finance.

Title II: Opening the Door for Accredited Investors (2013)

Implemented on September 23, 2013, Title II lifted a nearly century-old ban on “general solicitation”, the public advertising of private investment opportunities. Before this reform, entrepreneurs could only approach investors with whom they had pre-existing relationships. Under Rule 506(c) of Regulation D, startups could publicly promote fundraising campaigns, provided they accepted funds only from accredited investors and verified their accreditation status.

This change ignited a new era of online private fundraising. Platforms like AngelList, SeedInvest (now part of StartEngine), and Crowdfunder flourished by connecting startups directly to accredited investors. For the first time, investment opportunities could be marketed through digital channels, social media, email, and dedicated investment portals, creating unprecedented visibility for early-stage deals.

Title III: The Crowdfunding Exemption (2016)

The most groundbreaking reform arrived with Title III, also known as the CROWDFUND Act, which legalized Regulation Crowdfunding (Reg CF). After several years of deliberation, the SEC adopted final rules in October 2015, effective May 16, 2016, officially allowing non-accredited investors to participate in startup investing for the first time.

Reg CF empowered everyday Americans to invest modest amounts in early-stage ventures. Initially, companies could raise up to $1.07 million annually, but in March 2021, the SEC increased the cap to $5 million, significantly expanding the fundraising potential of small businesses.

Investment limits were designed to protect investors while ensuring fair access:

-

If annual income or net worth is below $124,000, individuals can invest up to the greater of $2,500 or 5% of their income or net worth.

-

If both exceed $124,000, they may invest up to 10% of the greater figure, capped at $124,000 per 12 months.

-

Accredited investors face no statutory investment caps.

These limits apply cumulatively across all Reg CF investments within a 12-month period to prevent overexposure to high-risk assets while still enabling meaningful participation in startup financing.

Title IV: Regulation A+ for Larger Raises

Title IV modernized Regulation A, creating Regulation A+, a framework that bridges the gap between crowdfunding and a traditional IPO. Companies can now raise up to $75 million per year, an increase from the previous $50 million limit,without the full compliance burden of going public, though they remain subject to SEC oversight.

Reg A+ offers two tiers of offerings:

-

Tier 1: Up to $20 million annually, with lighter reporting requirements and state-level review.

-

Tier 2: Up to $75 million annually, requiring audited financials and ongoing disclosures but allowing nationwide fundraising without separate state registration.

This structure appeals to more mature startups seeking to scale without going fully public, effectively bridging the gap between early crowdfunding rounds and institutional investment. The SEC’s 2021 amendments further strengthened this pathway by expanding capital limits and harmonizing exempt offering rules.

The Market Today: Growth, Challenges, and Reality Checks

Despite broader economic turbulence, equity crowdfunding has evolved into a critical pillar of the U.S. startup ecosystem. According to KingsCrowd, total capital raised under Regulation Crowdfunding (Reg CF) reached $423 million in 2023, before dipping to $343.6 million in 2024, an 18% decline driven by tighter liquidity and investor caution. Yet even amid this slowdown, the number of campaigns continued to grow, with hundreds of issuers successfully meeting their minimum targets, underscoring the model’s resilience.

Source: Kingscrowd

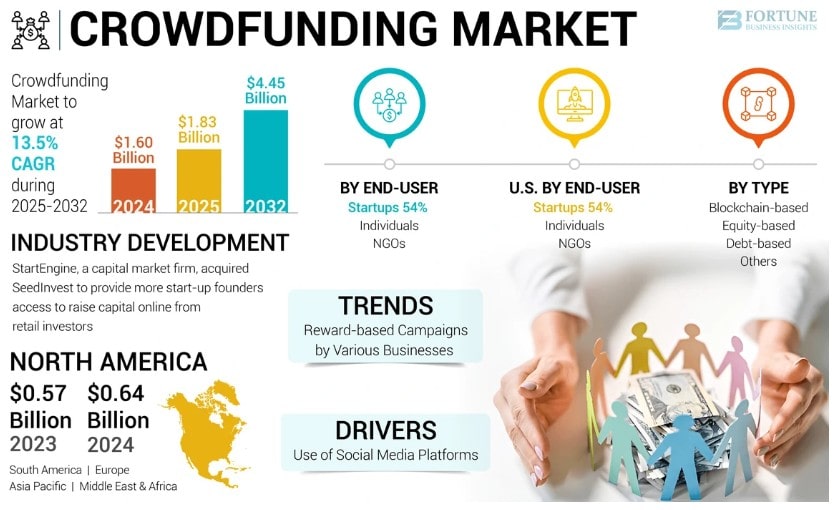

Globally, the crowdfunding market was valued at $1.60 billion in 2024, with forecasts projecting a compound annual growth rate (CAGR) of 13.5% through 2032, according to Fortune Business Insights.

Source: Fortune

The U.S. landscape remains dominated by the “Big Three” platforms, Wefunder, StartEngine, and Republic. These firms collectively account for the majority of Regulation CF and Regulation A+ deal flow, shaping much of the innovation in retail startup investing. Wefunder and StartEngine led 2024 by total capital raised, while Republic expanded its footprint into real estate and digital asset offerings, reflecting the diversification of investor appetite.

Investment behavior has also matured. The average check size increased to $1,500 for Reg CF offerings and $2,300 for Reg A+ campaigns, marking a 26% year-over-year rise. This trend suggests that while the number of retail investors has stabilized, those participating are contributing larger sums, signaling growing conviction in the equity crowdfunding model.

Valuations and Market Concerns

A clear divergence has emerged between venture capital (VC) and crowdfunding valuations. While VC-backed startup valuations dropped from their 2021 highs, those on crowdfunding platforms have remained elevated. The Q3 2024 PitchBook Venture Monitor placed the median VC seed valuation at $13 million, yet many crowdfunding campaigns list valuations at or above that level.

This gap raises concerns about overvaluation in the retail market. As KingsCrowd notes, crowdfunding valuations often rely more on narrative appeal than institutional due diligence, creating a mix of genuine opportunity and speculative pricing.

Investor Protections and Risks: What You Need to Know

Equity crowdfunding platforms and regulators have built key safeguards to protect investors and ensure transparency.

Platform Due Diligence: Top platforms screen applicants rigorously. SeedInvest accepts only 1% of startups, while Seedrs rejects 90% after initial checks, reducing fraud and low-quality listings.

Mandatory Disclosures: Companies must file Form C with the SEC, sharing financials, risk factors, and business plans so investors can verify details before funding.

Holding Period: Crowdfunded securities can’t be sold for one year, preventing quick flips and pump-and-dump schemes but limiting liquidity.

Investor Education: Platforms like Crowdcube provide training on risk, valuation, and due diligence, helping users invest responsibly.

Key Risks in Equity Crowdfunding

| Risk | Details |

|---|---|

| High Failure Rate | 2018–2024 data show ~2.9% failures so far; real rate expected closer to 60–70%. |

| Illiquidity | Most holdings locked for years; average exit window 8–12 years. Limited resale options even via StartEngine Secondary. |

| Dilution | Future funding rounds reduce ownership—e.g., 0.5% → 0.3%. One-third of crowdlending ventures fail to meet targets. |

| Limited Control | Small investors (< $25K) lack voting rights or board seats. |

| Information Gaps | Founders know more than investors despite disclosure rules. |

| Long Return Timeline | Returns may take 5–12 years, if achieved at all. |

Equity crowdfunding offers early-stage access but carries high risk, low liquidity, and long timelines. Only invest what you can afford to lose.

Success Stories: When It Works

Despite the risks, equity crowdfunding has produced notable winners.

Mercury

In July 2021, Mercury, a banking platform for startups, raised $4.9 million from 2,453 investors on Wefunder as part of its $120 million Series B round at a $1.62 billion valuation. Following the March 2023 Silicon Valley Bank collapse, Mercury reportedly gained thousands of new accounts and billions in deposits, highlighting how crowdfunding can effectively complement institutional funding.

Meow Wolf

The immersive art collective Meow Wolf raised $1.32 million from 621 investors on Wefunder in July 2017. Its first Santa Fe location generated roughly $8.8 million in annual revenue, and the company has since expanded to Las Vegas and Denver with additional locations planned. It remains one of the few non-tech ventures to scale nationally through crowdfunding.

Substack

As of April 2023, Substack reported around 35 million active subscriptions, more than 2 million paid subscriptions, and over $300 million paid out to writers. Despite its strong community growth, the company has faced scrutiny for raising capital at valuations considered high relative to its revenue and competitors, showing that even successful startups face pricing challenges.

The IPO Path

According to KingsCrowd, just 21 crowdfunded companies, about 0.3% of all issuers, have reached IPO status. Few have performed well post-IPO, particularly amid the rising interest-rate environment from 2022 to 2024.

Exits vs. Failures: The Scorecard

KingsCrowd’s 2018–2024 data shows:

| Outcome | Count | Definition |

|---|---|---|

| Positive Exits | 77 | IPOs, M&A, buybacks, or capital returns |

| Failures | 186 | Shutdowns or distressed sales |

Failures outnumber successes so far – but equity crowdfunding remains young. Many promising startups are still maturing, and typical angel investments take 8-12 years to exit.

How to Evaluate Equity Crowdfunding Deals

If you’re considering investing, follow these best practices. Diversification is non-negotiable, never put all your eggs in one basket. Experts recommend investing in at least 10-20 different companies to build a diversified portfolio and reduce the risk that one failure wipes out your returns.

Invest only what you can afford to lose. Treat equity crowdfunding money as “play money”, if losing it would cause financial hardship, don’t invest.

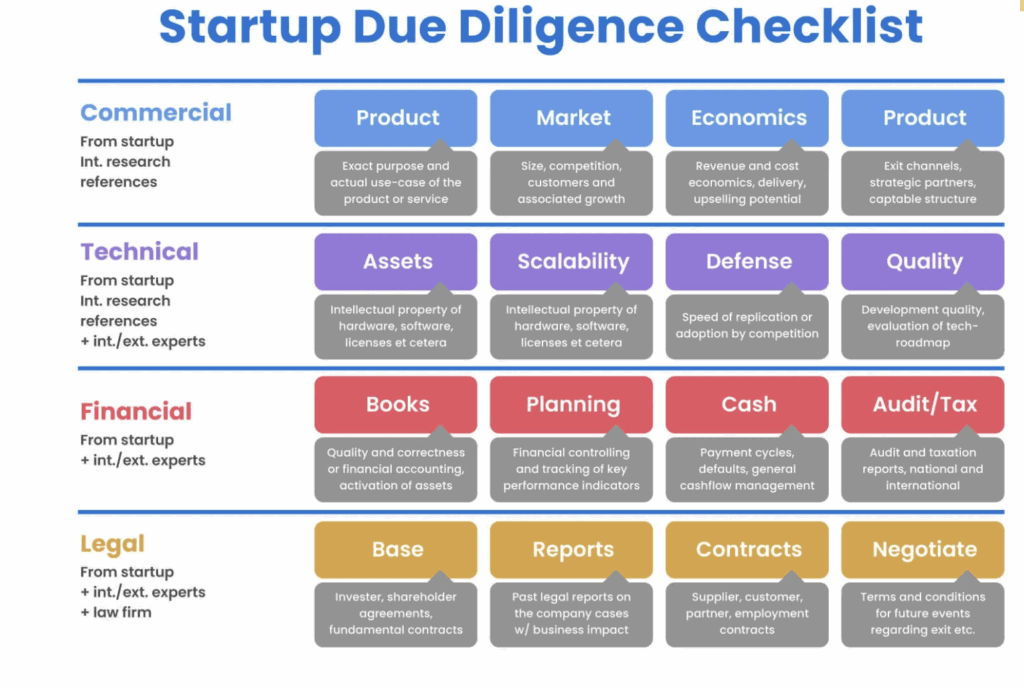

Do your due diligence. Read the full offering document, examine financials like revenue, burn rate, and cash runway, and research the founders’ experience. Understand the market demand and look for red flags such as unrealistic projections or vague business plans that often signal weak execution.

Source: Medium

Understand the deal terms. Know what type of security you’re buying, common stock, preferred stock, convertible note, or SAFE. Review your rights, the company’s valuation, and how the funds will be used. Look for traction; companies with revenue, customer validation, or milestones are generally safer than idea-stage startups.

Consider the platform. Those with strict vetting, like SeedInvest’s 1% acceptance rate, offer an added layer of quality control, though even vetted startups can fail.

Finally, beware of FOMO. A popular campaign isn’t always a good investment; crowd enthusiasm can inflate valuations. Think independently, focus on fundamentals, and invest with discipline.

The Future of Equity Crowdfunding

The industry is poised for continued evolution through regulatory modernization, technology, and global expansion. Authorities such as the U.S. Securities and Exchange Commission (SEC), Financial Conduct Authority (FCA, U.K.), and Monetary Authority of Singapore (MAS) are refining frameworks to enhance investor protection.

Blockchain-based tokenization is emerging as a tool for transparent ownership tracking, while secondary trading platforms like StartEngine Secondary aim to bring liquidity to early investors. Although trading volumes remain limited, these marketplaces represent an important step toward solving illiquidity in private markets.

Institutional participation is also rising, with private deal rooms and tokenized investment platforms granting investors exposure, direct or synthetic, to high-profile startups such as SpaceX and Stripe. While access is still largely restricted to accredited or institutional investors, tokenized vehicles are beginning to open new pathways for broader participation.

In Europe, equity crowdfunding represented about 10% of early-stage investments in 2023, totaling roughly €240 million, according to the EBAN Statistics Compendium 2023. The sector continues to expand, especially across technology and proptech ventures, highlighting the growing integration of alternative finance into Europe’s innovation ecosystem.

The Verdict: Is Equity Crowdfunding Right for You?

Equity crowdfunding represents a genuine democratization of startup investing. For the first time in generations, everyday Americans can participate in the growth of early-stage companies that were once reserved for wealthy venture capitalists. This shift has opened the door for a new class of investors eager to back innovation, support entrepreneurship, and share in the potential upside of startup success.

Equity crowdfunding can be a strong fit if you have capital you can afford to lose and understand the high-risk, high-reward nature of startups. It appeals to investors who are willing to hold their investments for 8–12 years, build diversified portfolios across multiple ventures, and enjoy exploring new technologies and business ideas. Those motivated by innovation and eager to support founders will find this model especially rewarding.

However, equity crowdfunding isn’t for everyone. If you need liquidity or quick access to your funds, can’t afford potential losses, or lack the time for proper due diligence, this type of investing may not suit your goals. Those seeking fast returns or unwilling to tolerate high risk should proceed with caution.

The JOBS Act created unprecedented access to startup investing. Whether this shift becomes a lasting democratization of wealth or a warning for unprepared investors will depend on education, regulation, and individual discipline.

As the market evolves, we’ll see more exits, failures, and real data on performance. For now, equity crowdfunding remains a high-risk yet potentially high-reward path that demands patience, diversification, and realistic expectations. Main Street can now invest in startups, but the question is, should you?