The IRS has released its official 2026 inflation adjustments (Revenue Procedure 2025-32), affecting returns filed in 2027. While modest, these updates raise standard deductions and expand tax brackets, allowing taxpayers to earn and deduct more before facing higher marginal rates. The changes aim to prevent “bracket creep” and deliver mild inflation relief for most U.S. households.

Higher Standard Deductions: For 2026, married couples can deduct $32,200; single filers $16,100; heads of household $24,150 — all slightly higher than 2025 amounts.

Expanded Brackets: The seven federal tax rates (10%–37%) remain unchanged, but income thresholds rise, for singles, the 22% rate now begins at $50,401; for joint filers, at $100,801.

AMT & Estate Adjustments: AMT exemption increases to $90,100 (single) and $140,200 (joint); federal estate tax exclusion jumps to $15 million per person.

Credit & Benefit Updates: EITC max rises to $8,046; Adoption Credit to $17,280; Health FSA limit to $3,400; foreign income exclusion to $132,900.

Planning Ahead: Review Form W-4, optimize withholdings, and update tax strategies early. For full details, see IRS Revenue Procedure 2025-32 and consult a tax professional.

The Internal Revenue Service (IRS) has officially released its inflation-adjusted tax brackets, standard deductions, and more than 60 related provisions for the 2026 tax year, the one that will affect returns filed in 2027. These annual updates are crucial because they help ensure that inflation doesn’t push taxpayers into higher tax brackets without an actual increase in real income. Even though the changes for 2026 are relatively modest, they provide mild relief by allowing Americans to earn more before reaching higher marginal tax rates.

Most taxpayers will benefit from higher standard deductions and expanded income thresholds across all brackets. In essence, you’ll be able to earn slightly more before moving into the next tax rate, while also deducting more income if you take the standard deduction. Although these changes may seem incremental, they add up over time, especially for households near the boundaries of tax brackets.

2026 Standard Deduction Amounts

The standard deduction, the amount you can subtract from your income before paying taxes, has increased for every filing category. This adjustment provides immediate relief to most households that don’t itemize their deductions.

Married filing jointly: $32,200 (up from $31,500 in 2025)

Single filers: $16,100 (up from $15,750 in 2025)

Head of household: $24,150 (up from $23,625 in 2025)

Married filing separately: $16,100 (up from $15,750 in 2025)

This means that more of your income will be shielded from taxation even if you don’t itemize deductions, effectively lowering your taxable income.

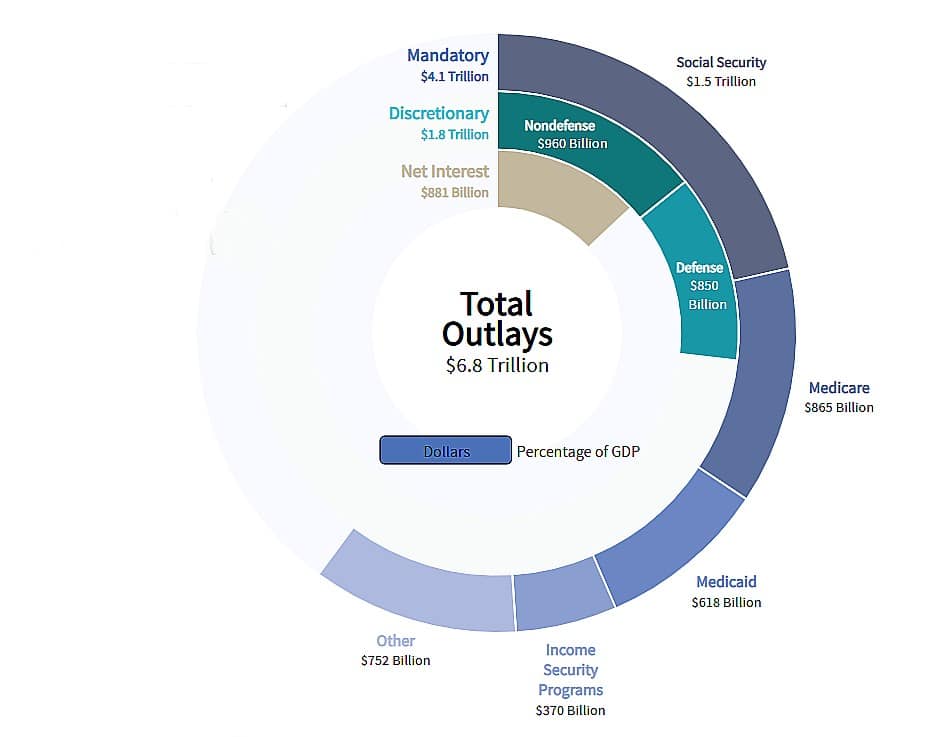

WHERE DOES THE MONEY GO?

Mandatory spending on Social Security and other support services account for the majority of the US government’s annual spending. Source: Congressional Budget Office.

2026 Federal Income Tax Brackets

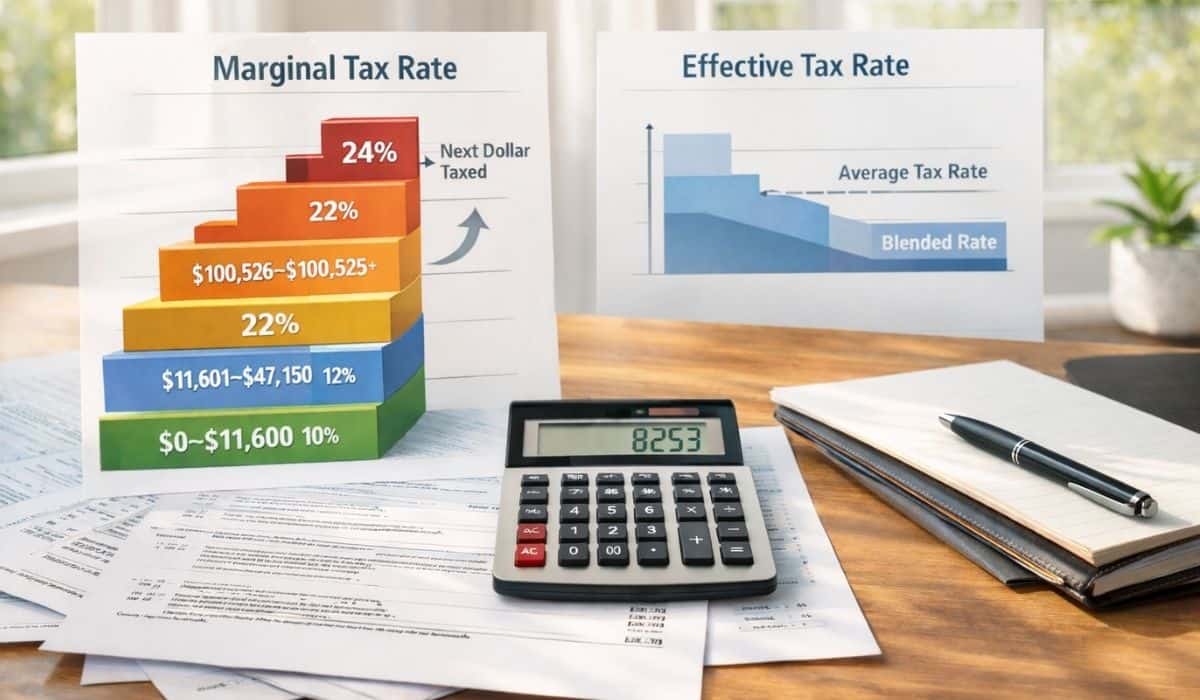

The seven federal tax rates, 10%, 12%, 22%, 24%, 32%, 35%, and 37%, remain unchanged. However, the income thresholds defining each bracket have been adjusted upward to account for inflation. This is one of the most significant components of the annual update since it prevents “bracket creep,” where inflationary income gains lead to higher tax rates without a real increase in purchasing power.

For single filers, the 2026 income ranges are as follows:

10%: $0 to $12,400

12%: $12,401 to $50,400

22%: $50,401 to $105,700

24%: $105,701 to $201,775

32%: $201,776 to $256,225

35%: $256,226 to $640,600

37%: Over $640,600

For married couples filing jointly, the brackets are:

10%: $0 to $24,800

12%: $24,801 to $100,800

22%: $100,801 to $211,400

24%: $211,401 to $403,550

32%: $403,551 to $512,450

35%: $512,451 to $768,700

37%: Over $768,700

For example, if a single taxpayer earns $51,000 in 2026, they’ll pay 12% on income up to $50,400 and only 22% on the remaining $600, not on the full amount. This progressive structure ensures that your effective tax rate, the average rate you pay, is always lower than your marginal rate, the rate applied to your last dollar of income.

Other Key 2026 Tax Adjustments

The IRS has also raised several important thresholds and credit limits that affect specific categories of taxpayers.

The Alternative Minimum Tax (AMT) exemption for 2026 rises to $90,100 for single filers (phaseout begins at $500,000) and $140,200 for married couples filing jointly (phaseout begins at $1,000,000), according to IRS Revenue Procedure 2025-32. These updates, detailed on the IRS website, adjust for inflation to prevent middle-income taxpayers from being pulled into the AMT.

In terms of estate taxes, the federal estate tax exclusion jumps significantly to $15,000,000 per person, up from $13,990,000 in 2025. This means estates below that amount owe no federal estate tax. For married couples using portability provisions, the combined exclusion can reach $30,000,000.

The Earned Income Tax Credit (EITC) will also rise, offering crucial relief to lower-income families. The maximum EITC for families with three or more qualifying children increases to $8,046 for the 2025 tax year, up from $7,830 in 2024, according to official IRS EITC guidelines.

For adoptive parents, the Adoption Tax Credit increases to $17,280 for qualified adoption expenses, up from $16,810 in 2024. Under recent tax-law changes, up to $5,000 of this credit may be refundable, providing additional support for families finalizing adoptions.

Americans working abroad can now exclude up to $132,900 in foreign-earned income from U.S. taxation, a slight increase from $130,000 in 2025. The Gift Tax Annual Exclusion remains at $19,000 per person in 2026, while the exclusion for gifts to non-citizen spouses rises to $194,000.

Employees will also benefit from increased transportation and parking benefits, with the monthly tax-free limit for employer-provided transit passes and parking increasing to $340, up from $325.

The Health FSA contribution limit increases to $3,400 for 2026, up from $3,300 in 2025, while the carryover amount rises to $680. The Employer-Provided Childcare Credit also expands in 2026, allowing employers to claim up to $500,000 (up from $150,000), with eligible small businesses qualifying for up to $600,000.

Provisions That Remain Unchanged

Certain aspects of the tax code will stay the same in 2026. Personal exemptions remain eliminated, continuing the policy established under the Tax Cuts and Jobs Act of 2017. Likewise, most taxpayers will still not face itemized deduction limits, though those in the top bracket will encounter some restrictions. The Lifetime Learning Credit phase-out ranges also stay consistent at $80,000–$90,000 for single filers and $160,000–$180,000 for joint filers.

These stable provisions maintain the simplified structure introduced under TCJA, emphasizing the broader standard deduction as the default option for most taxpayers.

Planning Ahead: How to Prepare for 2026

Now is the ideal time to review your tax strategy in light of the new adjustments. Start by revisiting your Form W-4 and checking whether your withholding matches your expected 2026 income. If you received a large refund or owed a substantial balance this year, fine-tuning your withholding could prevent either outcome in the future.

You should also take advantage of available deductions and credits that align with your financial situation. For example, the increased EITC and adoption credit could provide significant savings to eligible families. Meanwhile, maximizing retirement contributions, such as 401(k)s or IRAs, can lower your taxable income and keep you within a lower bracket.

For those planning major financial moves, like selling investments or exercising stock options, understanding the 2026 brackets will help you forecast your tax burden and time transactions strategically. High-net-worth individuals should also revisit their estate and gift plans, as the elevated exclusion thresholds create opportunities for tax-efficient wealth transfers before potential future policy changes.

The Bottom Line

The IRS’s 2026 inflation adjustments offer steady but meaningful relief to most taxpayers. Expanded brackets and higher deductions mean that households can retain a little more of their income, which helps offset inflation’s impact on living costs. Although these changes are incremental, they play a vital role in maintaining fairness and stability in the tax system.

Effective tax planning begins with understanding how these adjustments affect your unique financial situation. Review your current income, withholding, and potential deductions well before the year begins. For a full list of all 60-plus adjustments, consult the official IRS Revenue Procedure 2025-32, and consider speaking with a certified tax professional to tailor your strategy for the year ahead.

Related: This article is part of Mooloo’s Tax Strategy Hub, covering tax planning, investment taxes, retirement strategies, and after-tax wealth decisions: