Dividend ETFs: Income Investing Made Simple

Dividend ETFs combine the income potential of dividend-paying stocks with the diversification and simplicity of an index fund. They provide steady cash flow, professional management, and tax efficiency, making them ideal for both income-focused and long-term investors in 2025’s higher-yield environment.

- Purpose: Dividend ETFs hold baskets of dividend-paying stocks, offering regular income and diversification without the need to pick or rebalance individual holdings. Funds trade like stocks on major exchanges for liquidity and transparency.

- ETF Types: Investors can choose from High-Yield ETFs (e.g., VYM, SDY), Dividend Growth ETFs (VIG, SCHD), Low-Volatility ETFs (SPHD), and International ETFs (SCHY).

- Selection Criteria: Compare yield vs. growth, expense ratios (ideally <0.20%), diversification (50–500 holdings), and dividend sustainability (payout ratios <80%) before investing. Long-term consistency often outperforms the highest yields.

- Tax Efficiency: Qualified dividends are taxed at long-term capital gains rates (0%, 15%, 20%) per IRS guidelines. Holding ETFs in IRAs or 401(k)s avoids annual dividend taxes, maximizing compound growth.

- 2025 Outlook: With yields on quality dividend ETFs ranging between 2.5%–4.5%, funds like SCHD and VIG remain top choices for balancing income, stability, and long-term appreciation, especially in retirement or passive-income portfolios.

A dividend ETF (exchange-traded fund) is a professionally managed portfolio of dividend-paying stocks designed to generate steady income for investors while offering diversification and ease of trading. Unlike buying individual dividend stocks, which requires extensive research, monitoring, and portfolio rebalancing, a dividend ETF gives you access to a pre-assembled, diversified collection of companies known for paying regular dividends. These funds trade on major stock exchanges just like individual stocks, combining the liquidity of stock trading with the diversification benefits of a mutual fund.

Think of a dividend ETF as an all-in-one income-generating investment vehicle. Fund managers carefully select dividend-paying companies based on their yield history, financial stability, and growth potential. They continuously monitor and adjust the holdings to maintain the fund’s objective, whether that’s maximizing income, balancing growth and stability, or focusing on companies that consistently raise their dividends.

Do ETF Investors Actually Receive Dividends?

Dividend ETFs vary widely in their goals and methodologies. Some prioritize high income, others emphasize steady growth, and some focus on low volatility or global exposure. Understanding each type can help match your investment strategy with your financial goals.

High-Yield Dividend ETFs

Strategy: Target companies offering above-average current dividend yields, typically ranging between 2.5% and 5%, depending on market conditions.

Who it’s for: Investors seeking maximum income, particularly retirees or those wanting steady cash flow.

Risk profile: Moderate to high. Elevated yields can sometimes signal financial instability, payout stress, or limited growth prospects, especially in sectors such as energy, utilities, and financials. Diversification and quality screening are key to managing these risks.

Examples:

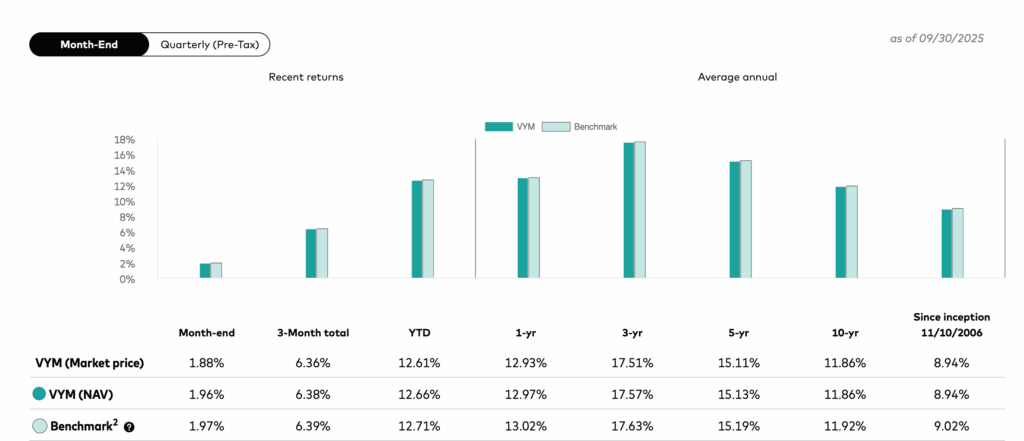

Vanguard High Dividend Yield ETF (VYM), focuses on large U.S. companies with higher-than-average dividend yields. It tracks the FTSE High Dividend Yield Index, which screens for sustainable payers rather than the very highest yields.

Source: Vanguard

SPDR S&P Dividend ETF (SDY) , invests in U.S. companies within the S&P Composite 1500 Index that have increased dividends for at least 20 consecutive years, emphasizing dividend reliability and consistency.

Source: SSGA

Dividend Growth ETFs

Strategy: Invest in companies with a proven record of consistently increasing dividends over time, even if current yields are modest (typically around 1.5%–3%).

Who it’s for: Long-term investors who value compounding returns, financial strength, and dividend reliability over maximizing short-term yield.

Risk profile: Moderate. These ETFs generally hold high-quality, financially sound companies that can maintain or grow payouts through different market cycles, though they still carry normal equity market risks.

-

Examples:

-

Vanguard Dividend Appreciation ETF (VIG), holds firms with 10+ years of consecutive dividend increases.

-

Schwab U.S. Dividend Equity ETF (SCHD), tracks the Dow Jones U.S. Dividend 100 Index, focusing on quality and sustainability.

-

ProShares S&P 500 Dividend Aristocrats ETF (NOBL), invests in S&P 500 companies with 25+ years of growing dividends.

-

Low-Volatility High-Dividend ETFs

Strategy: Combine high-yield stocks with low-volatility screening to create a more stable income stream.

Who it’s for: Conservative investors or those nearing retirement who seek steady income without sharp market swings.

Examples:

Invesco S&P 500 High Dividend Low Volatility ETF (SPHD), selects 50 stocks from the S&P 500 with both high yields and low volatility.

Source: Invesco

Franklin U.S. Low Volatility High Dividend ETF (LVHD), focuses on stable, income-producing companies with strong fundamentals.

International Dividend ETFs

Strategy: Invest in dividend-paying companies outside the U.S., providing global diversification.

Who it’s for: Investors seeking exposure to international markets and foreign income streams.

Examples:

Schwab International Dividend Equity ETF (SCHY), targets high-quality international dividend payers.

How to Choose a Good Dividend ETF

Selecting the right dividend ETF involves looking beyond just the yield. Consider these key factors:

1. Dividend Yield vs. Dividend Growth: A high yield offers immediate income, while dividend growth signals sustainability and compounding potential. For long-term wealth building, ETFs that grow their payouts often outperform high-yield funds over decades.

2. Expense Ratio: This is the annual fee expressed as a percentage of assets. Lower expense ratios, typically below 0.20%, help maximize returns. Over 30 years, even a small difference (0.06% vs. 0.50%) can mean tens of thousands in lost growth.

3. Holdings and Diversification: Look for ETFs with 50–500 holdings to avoid concentration risk. Examine sector exposure, dividend ETFs often lean toward financials, energy, or consumer staples.

4. Dividend Sustainability: Review payout ratios of underlying holdings; ratios above 80% can signal risk of future cuts. Funds with consistent dividend histories and moderate payout ratios are safer choices.

5. Performance and Volatility: Compare the ETF’s total return (price growth + dividends) to benchmarks like the S&P 500. Also check how it performs during bear markets, resilience is key for long-term investors.

6. Tax Efficiency: Dividend ETFs held in taxable accounts may face higher taxes on non-qualified dividends. Holding them in tax-advantaged accounts like IRAs or 401(k)s can reduce this burden.

Tax Treatment of Dividend ETFs

Understanding how dividend ETFs are taxed is essential for maximizing your after-tax returns. Qualified dividends receive favorable tax treatment, taxed at long-term capital gains rates: 0% for lower income levels, 15% for middle income ranges, and 20% for high earners. To be qualified, both the ETF must hold the underlying stock for more than 60 days during the 121-day period beginning 60 days before the ex-dividend date, and you must hold your ETF shares for more than 60 days during that same period.

Ordinary (non-qualified) dividends are taxed at your regular income tax rate, which can be as high as 37%. These include dividends from REITs (Real Estate Investment Trusts), some dividends from foreign companies, and dividends from stocks held less than 61 days. High earners: If your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly), you’ll also pay the 3.8% Net Investment Income Tax on dividend income.

In retirement accounts (IRA, 401(k), Roth IRA), dividends aren’t taxed when received. In traditional accounts, you’ll pay taxes when you withdraw. In Roth accounts, qualified withdrawals are completely tax-free. This makes dividend ETFs particularly powerful in retirement accounts since there’s no annual tax drag.

In taxable brokerage accounts, you’ll pay taxes on dividends in the year received, even if you reinvest them. This creates “tax drag” that reduces your compound growth compared to holding the same investments in a retirement account. Most states tax dividend income, though a few (like Texas, Florida, and Washington) have no state income tax, giving residents an advantage with dividend investing.

When you sell your ETF shares, those held over one year are taxed at long-term capital gains rates (0%, 15%, or 20%). Shares held one year or less face short-term capital gains taxed as ordinary income. ETFs are generally more tax-efficient than mutual funds because of their unique “in-kind” creation and redemption process, which minimizes capital gains distributions to shareholders.

Best ETF Providers for Dividend Investing

| Provider | Flagship ETFs | Typical Expense Ratio | Key Strengths |

|---|---|---|---|

| Vanguard | VYM, VIG | ~0.06% | Ultra-low cost, broad diversification |

| Schwab | SCHD | ~0.06% | Strong yield-quality balance |

| ProShares | NOBL | 0.35% | Access to S&P Dividend Aristocrats |

| iShares (BlackRock) | DVY | 0.38% | Global and sector-specific options |

| SPDR (State Street) | SDY | 0.35% | 20+ years of dividend history focus |

Common Misconceptions About Dividend ETFs

One of the biggest misconceptions about dividend ETFs is that higher yield always means better returns. In reality, extremely high yields, typically above 7%, often signal financial distress within the underlying companies. Consistent, moderate yields supported by sustainable dividend growth usually deliver superior long-term total returns.

Another common myth is that dividend ETFs are risk-free. While they tend to be less volatile than growth-oriented stocks, they can still experience sharp declines during market downturns because they are fundamentally equities, not bonds. Some investors also believe that holding dividend ETFs doesn’t make them real shareholders, leading to different tax treatment.

That’s false, ETF investors receive dividends just as they would from directly owning the individual stocks, and the tax treatment remains identical. Finally, not all dividend ETFs are created equal. They differ significantly in strategy, risk exposure, yield targets, and sector allocations. For instance, the Schwab U.S. Dividend Equity ETF (SCHD) focuses on high-quality, consistent dividend payers, while the Invesco S&P 500 High Dividend Low Volatility ETF (SPHD) emphasizes higher yields with greater risk exposure, two very different approaches despite both being dividend ETFs.

Getting Started with Dividend ETFs

For beginners, start with broad, diversified, low-cost dividend growth ETFs like SCHD or VIG. These balance current income with growth potential and quality screening. For income-focused investors, consider splitting between dividend growth ETFs (60–70%) and higher-yield options (30–40%) to balance current income with sustainability. For risk-averse investors, explore low-volatility dividend ETFs like SPHD that screen for stability alongside income. For global diversification, add a 10–20% allocation to international dividend ETFs like SCHY.

The beauty of dividend ETFs is that they make sophisticated dividend investing accessible to everyone. You get professional management, instant diversification, and regular income, all wrapped into a single investment you can buy and sell as easily as a stock. Whether you’re building long-term wealth or generating retirement income, dividend ETFs offer a powerful tool for achieving your financial goals.