How to Rebuild Your Finances After Bankruptcy or a Criminal Record

ADVERTISEMENT

Advertise with Us

- Start with a budget: Use zero-based budgeting to track essentials, cut unnecessary spending, and redirect even small amounts (e.g., $50/month) toward debt repayment.

- Rebuild credit carefully: Secured credit cards, credit-builder loans, and regular error checks at AnnualCreditReport.com help restore scores – timely payments remain the biggest factor.

- Secure income: Explore fair-chance hiring with employers like Amazon or JPMorgan, pursue short-term training in trades or healthcare, and leverage gig work for immediate cash flow.

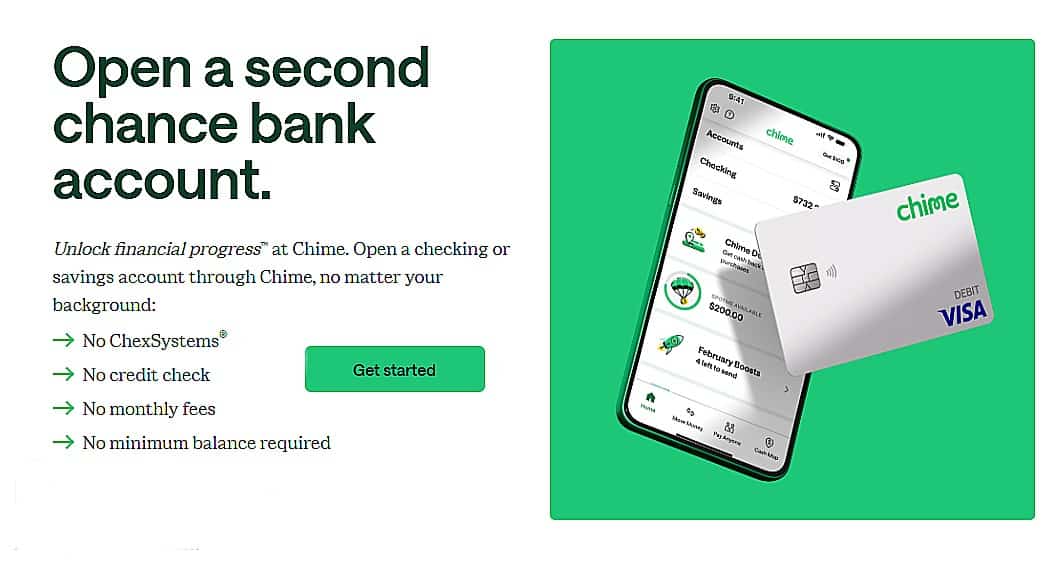

- Reenter the banking system: Second-chance checking accounts and credit unions provide alternatives to costly payday lenders and rebuild trust with mainstream banks (FDIC).

- Protect progress: Build a starter emergency fund, automate payments, and avoid predatory lenders to create lasting financial resilience.

ADVERTISEMENT

Advertise with Us

Related Posts

Related Insights

ADVERTISEMENT

Advertise with Us

Tags

Business & Entrepreneurship (82)

Crypto & Digital Assets (29)

Crypto As An Asset (3)

Custody & Security (1)

Custody Models (9)

Infrastructure and Access (11)

Investing (95)

Law & Control (49)

Loans & Credit (63)

Market Structure (18)

Personal Finance (138)

Press Releases (4)

Regulation & RIsk (1)

Retirement (39)

Self Custody (12)

Tax Strategy (24)

Third Party Custody (72)

Why Custody Fails (27)