Why This REIT Pays 12% Dividends When Banks Pay 0.5%

A 12% dividend yield from a real estate investment trust (REIT) can seem too good to be true compared with a 0.5% savings account, but the difference comes down to structure, risk, and regulation. REITs are legally required to pay out at least 90% of taxable income as dividends, making them attractive for income-seeking investors. In contrast, bank deposits trade higher returns for safety and FDIC insurance. The tradeoff: REITs carry market, interest rate, and sector risks, while savings accounts prioritize security and liquidity. For most investors, REITs should complement, not replace, cash reserves.

- Dividend rule: REITs must distribute 90% of taxable income, boosting yields but limiting retained earnings.

- Risk tradeoff: Savings accounts are FDIC-insured up to $250,000, while REITs can lose value in downturns.

- Yield contrast: Typical REITs pay 3%–5%, sometimes over 10%; savings rates average 0.3%–0.6% as of 2025.

- Liquidity factor: Bank funds are instantly available; REIT shares trade daily but can be volatile.

- Taxation: REIT dividends are taxed as ordinary income, similar to bank interest.

When a real estate investment trust (REIT) advertises a 12% dividend yield while a bank savings account pays just 0.5% interest, the difference can feel dramatic, and even suspicious at first glance. The key lies in understanding the structural differences between the two, the risks they carry, and the rules that govern them.

What Is a REIT?

A real estate investment trust (REIT) is a company that owns, operates, or finances income-generating real estate. Their portfolios can include diverse assets such as apartment buildings, shopping malls, warehouses, data centers, hospitals, and even mortgage-backed securities. Congress established REITs in 1960 to open the door for everyday investors to participate in large-scale real estate projects without having to directly purchase property. This is a significant point – given that one of the dominant narratives in the crypto “real world assets” hype-cycle is that RWAs give small investors the chance to own a share in large assets – with real estate being the most frequent case in point. The reality? This scenario has existed for over 60 years with REITs.

Source: Investopedia

In return for significant tax benefits, most notably avoiding corporate-level taxation, REITs must comply with strict rules. One of the most defining requirements is the distribution mandate: they must return the bulk of their taxable income to shareholders each year – another plus for income focused investors.

Why REIT Dividends Are So High

The 90% Payout Rule

Unlike most companies that retain earnings for reinvestment or expansion, REITs are legally obligated to distribute at least 90% of taxable income as dividends. This guarantees that shareholders receive consistent cash flow, but it also means REITs rely heavily on debt or issuing new shares to fund growth.

Income-Heavy Business Model

REITs derive revenue from rent, long-term leases, or mortgage interest. This creates a steady stream of cash, especially for equity REITs holding physical properties with stable tenants. For mortgage REITs (mREITs), which profit from lending spreads between borrowing and lending rates, dividend yields can surge into double digits when interest rate conditions are favorable. However, those yields can swing sharply when credit markets tighten.

Why Bank Accounts Pay So Little

Safety and Insurance

Bank savings accounts, unlike REITs, offer principal protection. Deposits are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor per bank. This guarantee means savers accept lower returns in exchange for security.

Federal Reserve’s Role

Savings rates closely mirror the Federal Reserve’s monetary policy. When the Fed sets rates low to stimulate the economy, banks adjust deposit rates downward. Even in higher-rate environments, banks often lag inflation, choosing instead to preserve margins rather than passing along higher yields to depositors.

Comparing REITs and Bank Deposits

REITs and bank savings accounts are not interchangeable, they serve entirely different purposes.

-

Yield: REIT dividends typically average 3%–5%, though some high-yield REITs and portfolios can reach 12% or more, while standard savings accounts generally pay around 0.3%–0.6%.

-

Risk: Bank accounts carry negligible risk due to FDIC insurance. REITs, by contrast, face market risks, interest rate fluctuations, and sector-specific vulnerabilities.

-

Liquidity: While REIT shares are publicly traded and can be sold on exchanges, prices fluctuate with market sentiment. Bank accounts provide instant, predictable access to funds.

-

Taxation: REIT dividends are taxed as ordinary income, sometimes at higher rates than qualified stock dividends. Bank interest income is similarly taxed as regular income.

Understanding Risk vs. Reward

A double-digit dividend yield can be enticing but often signals elevated risk. REITs are vulnerable to downturns in the property market or credit cycles. If a REIT pays out more than it sustainably earns, dividend cuts may follow, sometimes sharply impacting share prices.

Mortgage REITs are particularly exposed to changes in interest rates and borrower defaults. Equity REITs, while generally steadier, face risks from vacancies, falling rental rates, or declining property values.

Liquidity and Investor Considerations

Bank accounts are ideal for liquidity, emergencies, or near-term financial goals since funds are available immediately. REITs, though tradable, may be volatile and ill-suited for short-term needs. Investors must be willing to hold through cycles of economic expansion and contraction.

What Investors Should Watch For

-

Dividend Sustainability: High yields above 10% can be red flags. Examining payout ratios relative to earnings and cash flow is critical.

-

Debt Levels: Heavily leveraged REITs may struggle in rising interest rate environments.

-

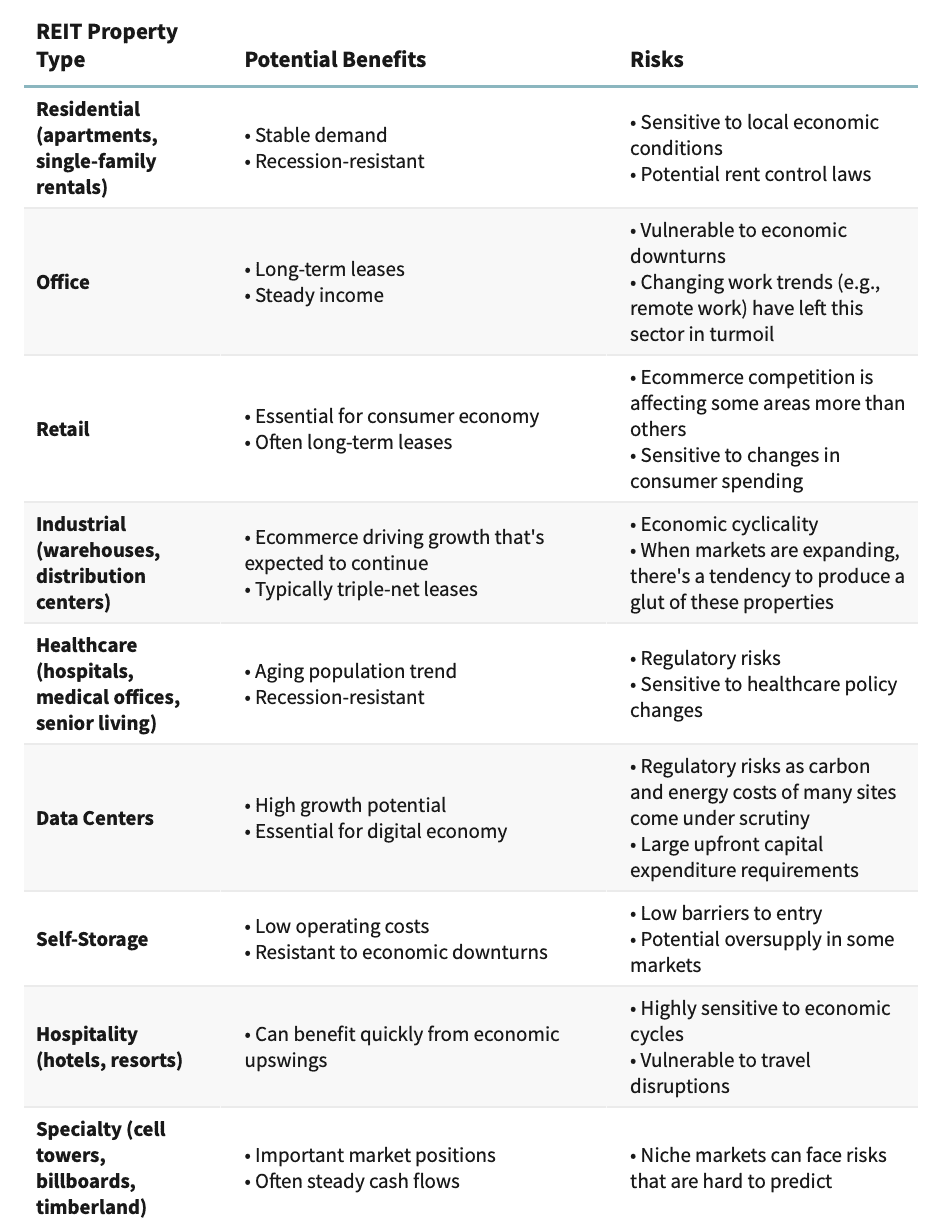

Sector Risks: Office REITs, for instance, have been under pressure from remote work trends, while industrial and data center REITs are benefiting from e-commerce and cloud adoption.

Bottom Line

Banks and REITs fulfill different roles in a financial strategy. Savings accounts provide safety, insurance, and guaranteed access but offer minimal growth. REITs deliver attractive income potential and portfolio diversification, but their higher yields come with meaningful risks. For most investors, REITs should complement, not replace, low-risk cash reserves. The key is balance: use bank accounts for security and liquidity, while carefully selected REITs can enhance long-term income and diversification.