I Make $70,000 A Year How Much House Can I Afford – 2026 Reality Check Inside

Buying a home on a $70,000 salary in 2025 is possible, but affordability depends heavily on down payment size, debt levels, and location. With mortgage rates averaging 6.5% and U.S. median home prices above $420,000 (NAR, July 2025), a single income at this level supports home purchases between $280,000 and $350,000, well below national averages. Buyers will need to apply the 28/36 rule, strengthen credit, and consider lower-cost regions to make ownership realistic.

- Affordability range: $280,000–$350,000 with a 10–20% down payment, based on the 28/36 lending rule.

- Market gap: National median prices ($422,400 existing; $403,800 new per Census Bureau) exceed safe affordability on $70,000 income.

- Regional differences: Midwest and South cities (e.g., Indianapolis, Cleveland, Memphis) still have homes under $300,000; coastal metros often exceed $500,000.

- Key levers: Higher credit scores lower mortgage rates; reducing debt and saving for a larger down payment boosts buying power.

- Next steps: Improve credit, pay down debt, save at least 10% down, and consider relocation or first-time buyer programs for affordability.

Buying a home on a $70,000 salary in 2025 presents both opportunities and significant challenges. Mortgage rates have leveled off around 6.5% for a 30-year fixed loan, which is lower than the peaks of 2023 but still historically high. Meanwhile, U.S. home prices remain elevated, and in many areas, they continue to rise. This combination has created an affordability gap where income growth lags far behind housing costs. For buyers in this income bracket, it is crucial to understand lending standards, calculate realistic budgets, and identify strategies that expand affordability.

The 28/36 Rule and Lending Standards

Lenders use the 28/36 rule as the starting point for determining how much house an individual or household can afford. Under this guideline, no more than 28% of gross monthly income should be dedicated to housing expenses, which include the mortgage payment, property taxes, and homeowners insurance. At the same time, total debt obligations, covering all monthly debts such as student loans, car payments, and credit card balances, should not exceed 36% of gross income.

While these numbers provide a baseline, lending institutions often adjust them based on the borrower’s credit profile, savings, and employment stability. Government-sponsored enterprises such as Fannie Mae and Freddie Mac allow debt-to-income ratios up to 43% in cases where borrowers demonstrate strong compensating factors, such as high credit scores or larger down payments. However, stretching beyond the 36% threshold can make finances fragile, especially when unexpected costs or job disruptions occur.

Breaking Down a $70,000 Salary

A $70,000 annual income equates to about $5,833 in gross monthly income. Following the 28% rule, a safe housing budget is roughly $1,633 per month. At current interest rates, this translates into different affordability ranges depending on the down payment.

-

With a 10% down payment, the affordable loan amount is close to $250,000, which supports a purchase in the range of $278,000 to $300,000.

-

With a 20% down payment, affordability expands to $312,000 to $350,000, while eliminating private mortgage insurance.

The difference highlights the critical role of upfront savings. Even modest increases in down payment size can significantly widen buying options and reduce monthly costs, making long-term ownership more sustainable.

The 2025 Housing Market Reality

Comparing these affordability figures to actual market data reveals the core challenge. The National Association of Realtors reported a median existing home price of $422,400 in July 2025. The U.S. Census Bureau placed the median new home price at $403,800, and Zillow’s home value index for August 2025 was $368,581. All of these figures remain above what a single income of $70,000 can comfortably support under traditional lending standards.

This gap is more pronounced in expensive metros. Entry-level homes in markets such as San Francisco, Los Angeles, New York City, and Boston typically exceed $500,000, which puts them out of reach for many middle-income buyers. By contrast, regions like the Midwest and parts of the South continue to offer more attainable options. Cities such as Indianapolis, Cleveland, and Memphis still feature properties below $300,000, making them realistic choices for buyers earning $70,000 annually.

Factors That Influence Buying Power

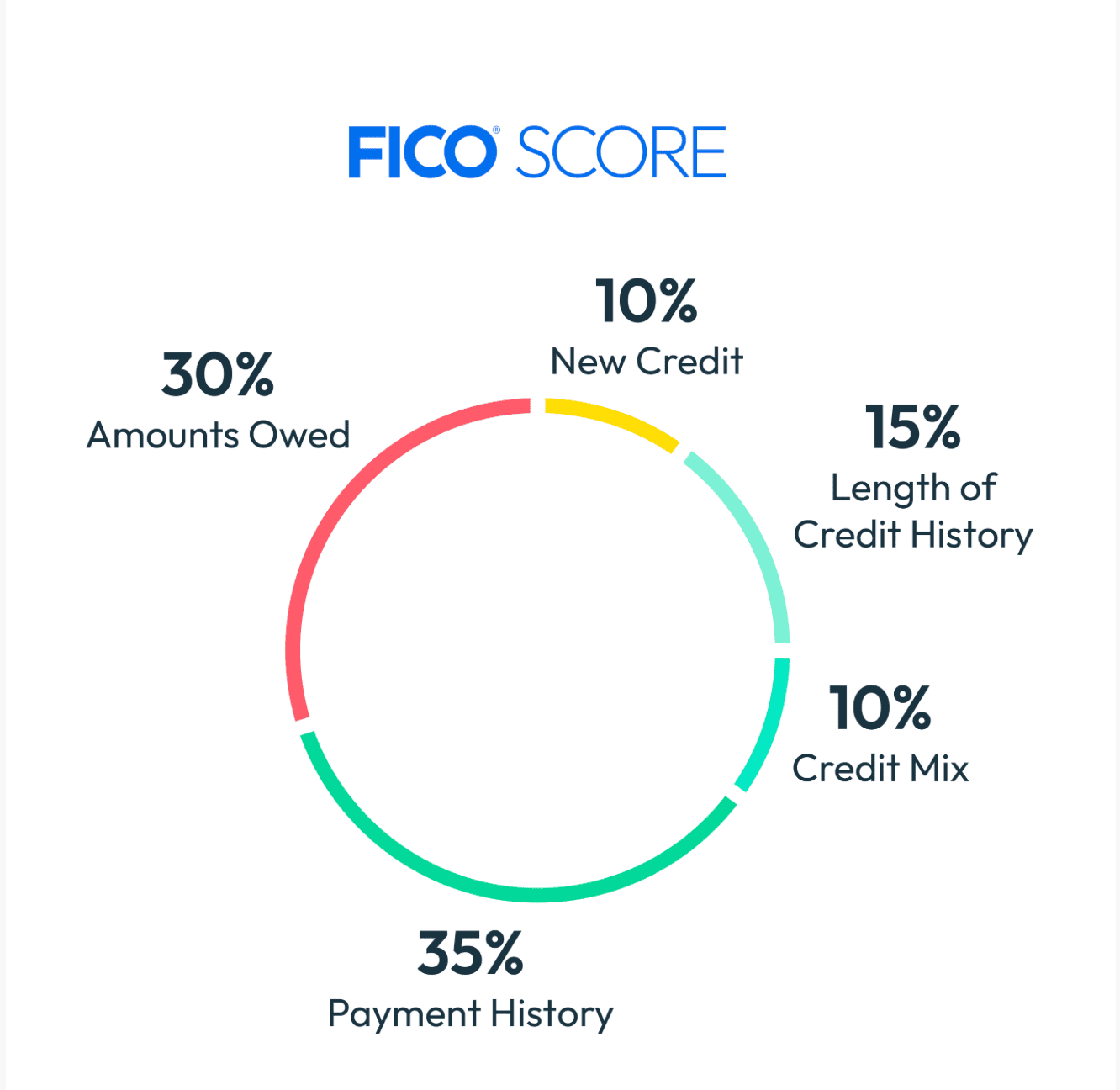

Affordability depends on more than just income. Credit scores can dramatically alter mortgage terms: a borrower with excellent credit may secure a rate of 6% instead of 6.5%, increasing their purchasing power by tens of thousands of dollars. Debt also has a direct impact. For example, a $400 monthly car payment reduces the available housing budget, tightening the price range of affordable homes.

Source: myFICO

Down payment savings remain one of the most powerful levers in improving affordability. A larger down payment not only reduces the size of the mortgage but also lowers monthly expenses and avoids mortgage insurance costs. Even an additional $10,000 in savings can improve affordability by tens of thousands in purchase price.

Regional cost differences further shape buying power. A $70,000 salary goes significantly further in lower-cost housing markets than in high-priced coastal metros. Buyers who are flexible about location may find relocating to more affordable regions the most realistic path to homeownership.

Practical Steps for Buyers

Households considering a home purchase on a $70,000 salary can improve their chances by focusing on preparation.

- Checking and improving credit scores before applying helps secure better rates.

- Paying down existing debt improves the debt-to-income ratio, making it easier to qualify for a larger loan.

- Saving for at least a 10% down payment not only increases affordability but also builds financial resilience.

- Getting pre-approved by a lender provides a clear picture of what is affordable before beginning the home search.

Rent-versus-buy comparisons should also be part of the decision-making process. In some metropolitan areas, renting may still be more financially sound in the short term, even if long-term ownership remains the goal. First-time buyers should also explore state and local assistance programs, which often provide grants or reduced down payment requirements, easing the path to ownership.

Conclusion

In 2025, a $70,000 salary supports a home purchase in the $280,000 to $350,000 range, depending on down payment size and debt obligations. Yet with national median prices above $420,000, affordability remains out of reach in many markets. Buyers must weigh their options carefully, considering not only income but also debt levels, credit health, and regional price differences.

Homeownership is still possible at this income level, but it often requires strategic planning, disciplined savings, and flexibility about where to buy. For many, success will mean targeting affordable markets, delaying purchase until savings grow, or adjusting expectations to fit the realities of today’s housing economy.