How Does The Age That A Person Starts Saving Impact The Amount They Can Earn In Compound Interest?

Time in the market beats timing the market. Compound interest rewards early savers because returns generate additional returns over decades. Starting at 25 with modest contributions often outperforms starting later with larger amounts. The cost of waiting is steep, and every year delayed means saving more just to catch up. Even small amounts invested early, through a Roth IRA, 401(k), or brokerage account, grow into substantial wealth thanks to compounding.

- Starting at 25 with $200/month for just 10 years ($24,000) can grow to over $280,000 by age 65, beating someone who contributes $200/month from 35–65 ($72,000) but ends with only ~$245,000.

- The final decade of compounding often produces as much growth as all prior decades combined, showing why age matters more than contribution size.

- Waiting 10 years means you must save significantly more monthly (e.g., $300 instead of $200) just to reach the same balance.

- Consistency and automation are critical, steady contributions, even $25–$50 in your 20s, can snowball into tens of thousands at retirement.

- It’s never too late: in your 50s and 60s, IRS catch-up contributions provide ways to maximize late-stage savings.

When people think about building wealth, they often focus on income levels or picking the right investments. While both matter, there’s another factor that has an even greater impact: time.

The earlier you start saving, the longer your money benefits from compound interest. This effect occurs when your savings not only earn returns, but those returns also begin to generate additional returns. Over decades, this snowballing growth can create results that seem extraordinary. But it isn’t magic, it’s math. And understanding how age affects compounding can guide smarter financial decisions.

Source: Investor.gov

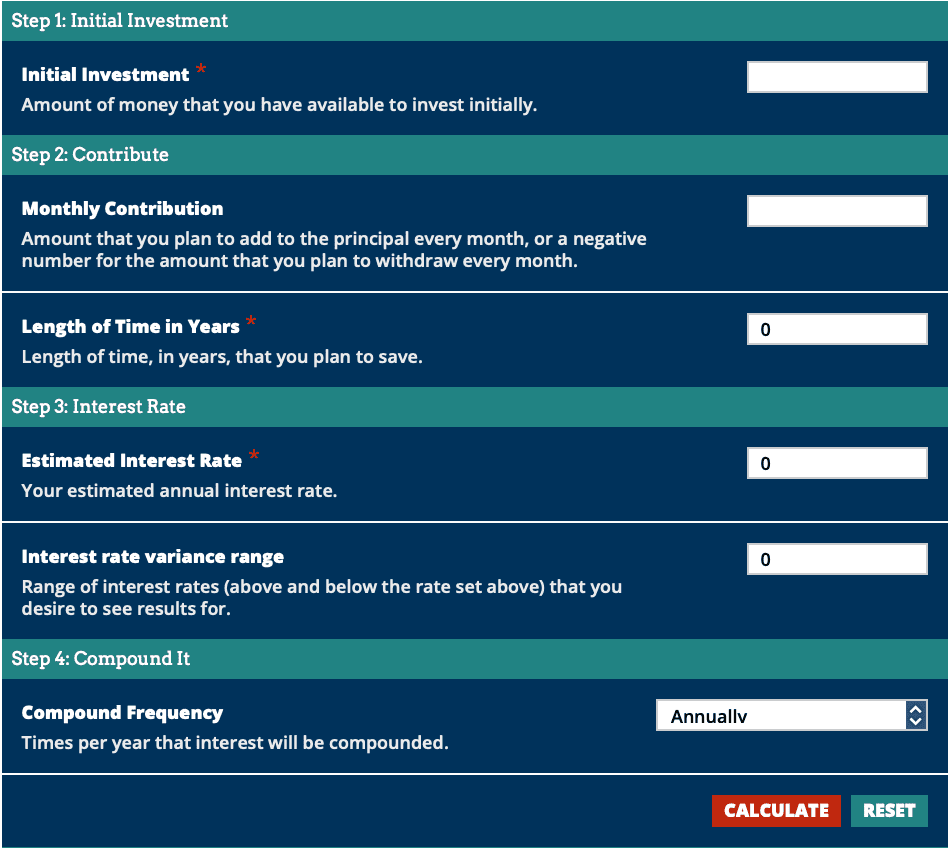

How Compound Interest Works

Compound interest operates on two levels:

-

Your contributions: the money you put in.

-

Your earnings on earnings: growth from prior years (interest, dividends, or reinvested returns).

Over time, the second element begins to dominate. This is why financial experts often emphasize that time in the market beats timing the market.

Breaking Down the Math

Imagine saving $200 each month in an account growing at an average of 7% per year:

| Years Saving | Total Contributed | Ending Balance |

|---|---|---|

| 10 years | $24,000 | $34,400 |

| 20 years | $48,000 | $103,000 |

| 30 years | $72,000 | $245,000 |

| 40 years | $96,000 | $525,000 |

Notice how the final decade produces nearly as much growth as all the previous decades combined. That’s the curve of compound interest in action, the longer the money stays invested, the steeper the growth.

A Tale of Two Savers: Early vs. Late Start

| Saver | Contribution Window | Total Contributed | Ending Balance at 65 (7% annual, monthly comp.) |

|---|---|---|---|

| Alex (Early Starter) | $200/mo from 25–35, then stops | $24,000 | $282,607 |

| Jordan (Late Starter) | $200/mo from 35–65 | $72,000 | $245,417 |

Why this matters: Even though Jordan contributes three times more, Alex still finishes with the larger balance because those early dollars compound for an extra decade.

This example highlights a critical truth: the cost of waiting is greater than most people realize.

Why Waiting Is So Expensive

Delaying savings by a decade forces you into tough trade-offs. To match Alex’s outcome, Jordan would need to contribute over $300 each month instead of $200. That extra $100 doesn’t sound huge, but across decades it means tens of thousands more in contributions just to catch up.

The reality is that time does the heavy lifting. Money saved early grows for longer, and no amount of later hustle can fully replace those lost years. Even modest early contributions, $25 or $50 per month in your twenties, can grow into tens of thousands by retirement.

A helpful metaphor is planting trees. A tree planted at 25 has 40 years to grow tall, strong, and fruitful. A tree planted at 35 has only 30 years. Both grow, but the earlier one always produces more.

Strategies for Every Age

While early starters have the biggest edge, it’s never too late to benefit from compound interest. Different stages of life call for different approaches:

-

In your 20s: Start small, even if it’s just a few dollars each month. The habit is more important than the amount. Retirement accounts like a Roth IRA or employer 401(k) are excellent vehicles.

-

In your 30s and 40s: As income rises, increase contributions. Automating transfers ensures consistency without effort.

-

In your 50s and 60s: Take advantage of IRS catch-up contributions in retirement accounts. The focus here is on maximizing savings during peak earning years while maintaining steady growth.

The key lesson is not to wait for the “perfect time.” Markets go up and down, expenses fluctuate, but delaying savings only makes the climb steeper later.

Key Lessons About Wealth and Time

-

Starting age matters more than contribution size, especially early on. Ten years of early compounding can outweigh 30 years of later saving.

-

Waiting has a steep price. To catch up, late savers must contribute significantly more.

-

Consistency is king. Small, steady contributions add up, and automation ensures discipline.

-

It’s never too late. While starting young is ideal, beginning at any age improves your future.

Final Thoughts

The age at which you begin saving is one of the most decisive factors in your financial future. Starting in your twenties offers the largest advantage, but even beginning in your thirties, forties, or later can yield meaningful results. Compound interest is a patient partner, it rewards time and discipline far more than luck or timing.

Wealth-building is less about heroic investing choices and more about letting time do its work. The earlier you begin, the less you’ll need to save, and the more your money will grow on its own. But the most important truth is this: the best time to start is now. Every year you wait, the cost rises, but every dollar saved today is a seed that compounds into tomorrow’s financial security.

About Portfolio Strategy

Portfolio construction sits at the core of long-term investing. It determines how risk is balanced, how returns are captured, and how portfolios survive periods of volatility, drawdowns, and changing market conditions.

Explore the full framework in our Portfolio Strategy guide.